Oil continues to recover despite lingering supply concerns and this is pushing the USD/CAD exchange rate lower.

The Canadian dollar's epic period of appreciation appears unstoppable with the currency forcing the USD/CAD exchange rate down a further 0.3% ahead of the weekend.

USD/CAD is quoted at 1.2950 at the time of writing but, “in the light of the rapid fall in USD CAD we may be set to test back towards 1.3095, this comes as CAD looks increasingly overbought.”

The chances of a near-term rebound in the US dollar are growing argues analyst Jeremy Stretch at CIBC.

The post FOMC slide in the USD has benefitted nominal commodity prices.

“We would argue the USD unwind is overdone, such a scenario should test the oil price rebound,” says Stretch.

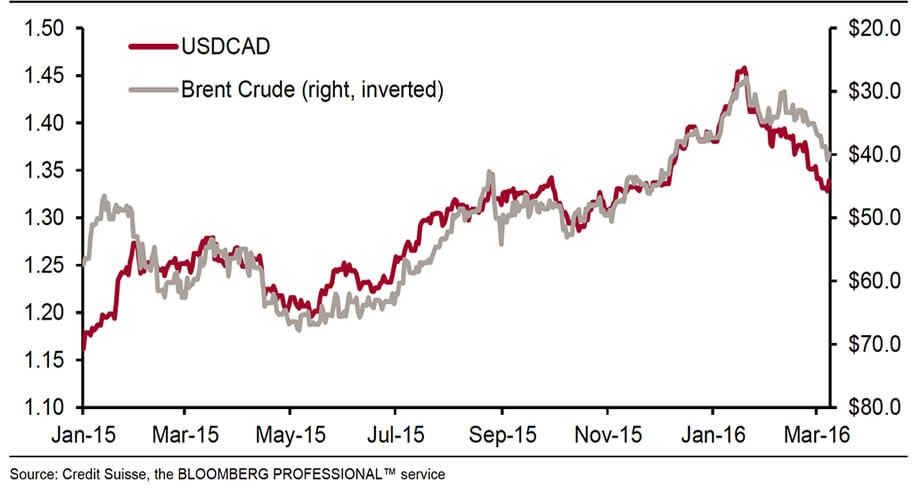

Oil and the CAD, Still Best of Friends

The price of oil continues to rise despite ongoing evidence of over-supply, with WTI reaching above $40/barrel on Thursday March 17.

The rise was put down to heightened expectations that major producers will cut supply following reports the Saudis and Russians have managed to gather together all-bar-Iran for a conference on the subject later in the month.

Indeed, it seems producers have little choice but to cut production or watch weaker members die a slow death due to unprofitable margins.

For the US dollar to Canadian Dollar exchange rate pair the price of oil is the most significant driver, so a continuation of the rally has spurred the pair to fall a near equivalent amount.

So close is the correlation between black gold and the Canadian Dollar, in fact, that some traders use the USD/CAD to trade oil.

Both the Canadian Dollar and oil were given another leg-up by recent reports of 800,000 ‘missing’ barrels of crude which the International Energy Agency (IEA) cannot account for, as reported in the Wall Street Journal.

Although total global production is 89 million barrels a day and the missing quotient is less than 1.0% of that, it accounts for roughly 40% of the oversupply, thus, if as some analysts believe the barrels do not even exist – as many do – and are simply a result of accounting errors - oil being a notoriously slippery thing to keep track off - the possibility of a major spike higher could result.

Standard Chartered have revised up their projections for the price of oil to $63 by year end to reflect the missing barrels discount.

However, in the short-term they seem more bearish, expecting the black stuff to come back down to 30 bucks a barrel in the 3-6m window.

Another supporting factor for crude is growing demand for the commodity, which is likely to absorb oversupply eventually, when Standard Chartered see the price “rebalancing”:

“Crude oil demand, on the other hand, remains more resilient. According to the International Energy Agency (IEA), total crude oil demand continues to climb, with a pick-up in momentum in US crude oil demand. In sum, we believe markets are likely to rebalance by the end of the year, putting upward pressure on oil prices."

Potential Dollar Weakness Could Back-Wind Oil

Oil is priced in dollars so the price of oil is not just due to supply and demand for the commodity but is also influenced by the value of the dollar.

The stronger the dollar, the more oil one dollar can buy and therefore the lower the dollar price of a barrel; the weaker the dollar, the higher the price of a barrel of oil, since a single dollar has that much less purchasing power.

Part of the reason for oil’s rapid decline in 2014-15 was that for much of the bear market the dollar was rising – multiplying the impact of the root-cause oversupply. This also explains the precipitous fall in the Canadian Dollar versus the US Dollar.

If the dollar were to weaken, that fact alone, regardless of supply concerns would lead to a rise in oil prices simply because they are priced in dollars.

The Fed’s dovish retrenchment aside, there are other factors which could lead to a fall in the dollar.

A recent report from Credit Suisse argued that there might be a ‘Trumpxit’ premium which has not yet been factored into the value of the dollar. However given recent polls put Hillary Clinton ahead of Trump by a margin of over 10% it would seem he currently does not have the support to pose a real threat.

What is more of a threat to the dollar, however, is global central bank impotence.

By this we mean the loss of impact of central bank policies as a tool for weakening exchange rates and hence aiding dollar strength via the backdoor.

This has already happened to the euro in relation to the ECB’s weakening grip and the BOJ which has failed to weaken the yen.

If the problem spreads to other central banks it could start to substantially negate the dollar’s potential to rise against these currencies, based on policy divergence alone.

This in turn could provide oil with more up-lift, purely from a dollar pricing perspective.

From a USD/CAD perspective, rising oil and falling dollar could precipitate as sharp a fall as the previous rally proved.

Our current forecasts are for USD/CAD to fall to 1.2800 on a break below the 1.2944 lows.