- CAD lags into New Year as underperformance continues.

- BoC policy may see underperformance extend into 2021.

- As competitiveness, recovery fears keep BoC up at night.

Above: BoC Governor Macklem. Image © Bank of Canada, Reproduced Under CC Licensing

- GBP/CAD spot rate at time of writing: 1.7415

- Bank transfer rate (indicative guide): 1.6759-1.6881

- FX specialist providers (indicative guide): 1.7106-1.7245

- More information on FX specialist rates here

The Canadian Dollar continued its trend of underperformance, lagging major rivals on Thursday as the curtain began to close on 2020 and ahead of a year in which Bank of Canada (BoC) concerns about export competitiveness could feature prominently as a driver of the currency.

Canada's Dollar was on course to cede ground to even Pound Sterling for 2020, which has itself been an underperformer, and was matched only by the U.S. Dollar in the breadth of its declines against major currencies following a coronavirus-contaminated year of almost unprecedented economic disruption.

"Total economic activity was about 4% below February's pre-pandemic level. Both goods-producing (+0.1%) and services-producing (+0.5%) industries were up as 16 of 20 industrial sectors posted increases in October," Statistics Canada said ahead of the Christmas holiday.

Just like after the financial crisis of 2008, Canada's economy has been quick to attempt a rebound from its coronavirus-inspired trough earlier in the year, although back then its recovery was later characterised by an underperformance of its export sector even after snapping out of recession earlier than most.

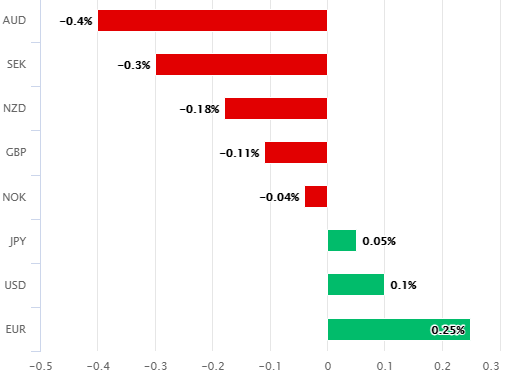

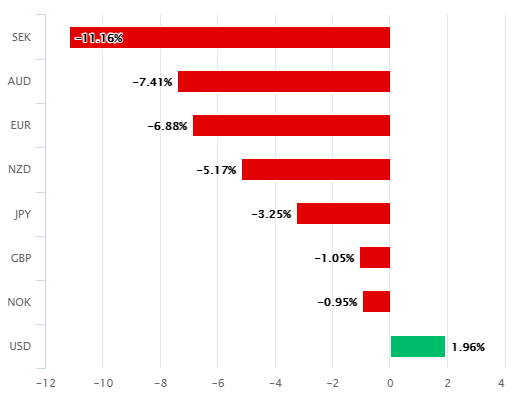

Above: Canadian Dollar performance against major currencies on Thursday (left) and for 2020 year (right).

Close ties to the badly damaged U.S. economy were a key part of the post-crisis underperformance, although so too was a lack of competitiveness connected to low productivity growth and the Loonie's reticence to adjust fully to domestic challenges. This is according to a December speech from Bank of Canada Governor Tiff Macklem, who'll be watching the currency closely in 2021.

"Today’s sub-1.30 dollar-Canada levels aren’t really out of line with pre-Covid experience, but there’s plenty of evidence that Canada’s export performance has been held back since 2008 by an overvalued exchange rate. It’s been a 12-year period of red ink in the trade balance, and generally weak contributions to growth from real exports, even when the global economy was booming. That left the economy excessively dependent on leveraged consumers and housing," explains Avery Shenfeld, chief economist at CIBC Capital Markets. "Macklem has now rightly called out the recent appreciation in the C$ as a concern."

The "impact of a stronger currency," was one of the two foremost drivers that were cited by Macklem this month for the post-2008 underperformance of Canada's export sector, which left the broader economy overly reliant on debt-funded consumption by already highly leveraged households.

After the pandemic of 2020, with all of its associated economic disruption and the resulting increases in debt burdens across the board, a debt-financed recovery led by domestic consumption will be even less viable.

Above: Pound-to-Canadian Dollar rate shown at daily intervals with USD/CAD (blue).

"Hope is not a strategy," either, according to the BoC, even more so because the "disproportionate impact of the pandemic on trade in services has significant implications for Canada." With services industries shuttered due to the coronavirus and expected to wear scars for a while after the pandemic abates, the manufacturing industry has a larger than usual role to play in the forthcoming recovery, and one that's more critical to the economy's long-term prospects than at any point in the past.

"We believe that inflation is likely to test the BoC's commitment to its lower bound as we have inflation reaching 2% by 2Q followed by strong growth. But at least part of the increase will be due to a base effect and since we have unemployment falling slowly we believe the BoC will look through it," say Carlos Capistran and Ben Randol, economist and currency strategist respectively at BofA Global Research. "We expect a near-term rise to 1.34 in 1Q on a temporary rebuild in CAD risk premium, moderating to 1.29 by 2H 2021 as the global economy, oil prices and risk-appetite extend their respective recoveries and trade policy uncertainty remains low under the new Biden Administration."

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

With few exceptions, major economy central banks are often loathe to intervene directly in currency markets, instead preferring to limit themselves to verbal objections to market views and the resulting price moves. Verbal intervention hasn't always served the BoC well in the past, although fortunately for the bank there is another option and Canadian inflation metrics could compel Macklem and colleagues to take advantage of it as soon as the first-quarter 2021.

"Core inflation measures were unchanged at 1.70% on average after downward revisions to October. Q4 CPI is now tracking well above BoC projections, however, the Bank will be content to look through this given elevated uncertainty around the second wave of COVID-19," says Andrew Kelvin, chief Canada strategist at TD Securities.

Above: USD/CAD shown at weekly intervals alongside U.S. Dollar Index (blue).

The Federal Reserve across the border in the U.S. has successfully sank its Dollar, the strength of which posed as an additional threat to global economic and financial stability earlier in 2020, by shifting to an average-inflation-targeting strategy that takes a symmetric view of the bank's target to produce a steady medium-term average of 2% inflation using its monetary policy.

That policy shift effectively means the Fed will keep interest rates on the floor even after inflation rises above the target and for something like as long as the consumer price index spends undershooting the desired level beforehand. This is a recipe for 'negative real interest rates' and a falling U.S. Dollar, one the BoC might be able to replicate effectively if it chooses to, in a decision that would circumvent any need for direct or even continued verbal intervention.

A BoC pivot to an average-inflation-targeting regime would provide Canadians with a more protracted period of favourable policy conditions, buttressing the domestic economic recovery, and could be particularly effective in discouraging investors away from the Canadian Dollar in the early part of next year if as some analysts and economists expect - inflation continues to recover promptly from coronavirus-inspired lows in the months ahead.

"The economic backdrop is mixed; on the one hand, employment trends have been healthy and prices appear somewhat sticky, which may leave the Bank of Canada (BoC) reluctant to ease policy further. On the other, second wave effects risk undermining the economic momentum that developed since mid-year and foreign investors may eye the large (through not unusual, in the current international environment) fiscal imbalances," says Shaun Osborne, chief FX strategist at Scotiabank. "CAD’s rise may slow or stall over the holiday period and we note an historic tendency for USDCAD to rally somewhat early in Q1 of the calendar year. We think USDCAD rebounds to the 1.29/30 area—if indeed the USD can reach that high—will attract renewed USD selling however."