- Chinese iron ore demand is falling and a key risk to the AUD say BofAML.

- Other analysts argue RBA to become a supprtive force

- Australian Dollar forecasts range from 0% change to 7% downside

© 孤飞的鹤, Adobe Stock

The Australian Dollar is expected to drift lower toward the bottom of its recent range over coming months, according to strategists at Bank of America Merrill Lynch, although developments in the Chinese property market will be key to its direction once past the second quarter.

Australia’s Dollar has traded back and forth between the 0.75 and 0.80 thresholds against the US greenback in 2018 and is forecast to fall steadily, from 0.7720 Monday, back toward 0.75 before the end of the second quarter.

There is even a risk the currency moves even lower than that in the near future, although the eventual destination of the currency will depend on whether China’s residential property market can avoid a further slowdown.

“The deceleration in iron ore shipment growth warrants caution against buying AUD until the data distortions dissipate. Moreover a stronger USD, firmly neutral RBA and rising trade tensions at a global level are unlikely to present a constructive backdrop for the currency,” says Adarsh Sinha, an FX strategist at Bank of America Merrill Lynch.

Source: Bank of America Merrill Lynch

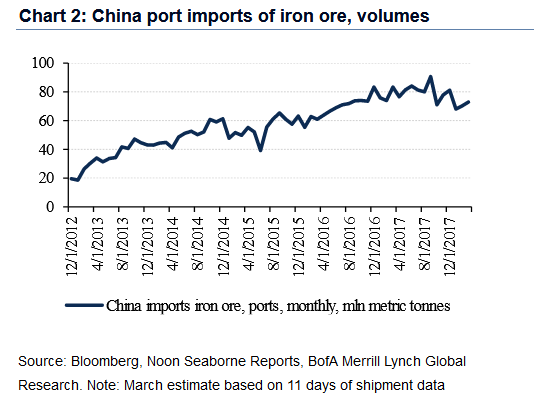

Sinha and the BAML FX team advocate watching a series of so called high frequency indicators of conditions in the Chinese property market in order to get a steer on the likely direction of the Australian Dollar. The best of these indicators is shipments of iron ore into China.

Many analysts watch shipments out of key Australian shipping locales such as Port Hedland closely for insight into Chinese demand, but the BAML team look instead at inbound shipments into key Chinese shipping centres like the port at Qingdao to gauge the country’s appetite for iron ore.

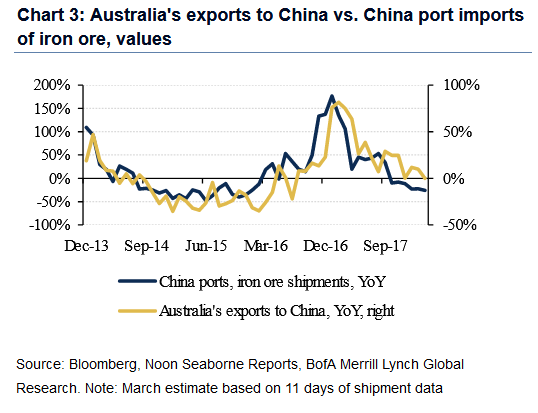

“It is clear the downtrend in iron ore shipments began well before the Lunar New Year distortions, coinciding with the broader slowdown in fixed-asset investment. The smoothed growth rate (3mma YoY) of iron ore shipments in value terms is now at its weakest since February 2016, falling 23.7% YoY. This is partly related to high inventory at Chinese ports, but at least partly symptomatic of a weaker demand trend. As Chart 3 shows, this bodes poorly for Australia's exports to China,” Sinha adds.

Source: Bank of America Merrill Lynch.

“Key factories have evidently taken up the slack from the decline in production at smaller factories, keeping the nationwide growth rate roughly flat. In our view, watching steel production growth at the key factories, coupled with the development of steel prices that so far remain in an uptrend, will help assess the investment demand for commodities over the coming month,” says Sinha.

Steel production is another useful indicator of the trend in Chinese iron ore demand. This measure was seen as unreliable during 2017, due to suspensions of production for the winter period and state mandated closures of facilities on environmental grounds. But with these actions now in the past and production picking back up again following the winter period, the BAML team advocate watching Chinese steel factories once again for a steer on iron ore demand and the Australian Dollar.

“Ultimately we expect AUD/USD to stay within range, forecasting a trough of 0.75 in 2Q 2018 - however there are downside risks to this forecast if tighter financial conditions, particularly funding costs and crackdown on leverage, begin to weigh on the Chinese property market,” Sinha says, in a March research note.

Above: AUD/USD shown at weekly intervals.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

A Chinese economic slowdown, driven by a fall in fixed asset investment and the property market, was flagged by BAML as one of the key risks facing Australia and the global economy more broadly back at the start of the year.

In the absence of this, Sinha and the Bank of America team forecast the Australian Dollar will dip to 0.75 against the US Dollar in the next three months before recovering to 0.77 in time for year-end.

For the Pound-to-Australian-Dollar rate, they forecast Sterling will dip to 1.78 against its Antipodean rival in the second quarter, before rising back to its current level of 1.83 in time for year end.

Above: Pound-to-Australian-Dollar rate shown at weekly intervals.

While the team at Bank of America may see the Australian Dollar's fortunes closely tied to certain Chinese sectors, others are increasingly eyeing the Reserve Bank of Australia as a source of potential gains for the Aussie currency this year.

"The RBA is concerned with the amount of leverage in the household sector and the lack of wage growth. However, the last statement from RBA Governor Lowe noted that wages have likely ‘troughed’ given the skill shortage in several sectors (signalling a hawkish shift in tone)," says Bipan Rai, a macro strategist at CIBC Capital Markets. "True, wages are still well below the RBA’s preferred level of 3.5%, but the view at the Bank on the trajectory is changing and the market doesn’t necessarily need to wait until wages are at that level before AUD price action moves."

The RBA has held its cash rate steady at a record low of 1.5% for 20 months while the outlook for a change in narrative from policymakers appears to have dimmed in 2018. After alll, Australian growth came in lower than was expected for the fourth quarter, with GDP rising just 2.4% for the year overall, which is down from the 2.9% in 2016.

Meanwhile, the RBA recently appeared to have become less confident in its own forecasts for growth in 2018 and 2019 too. It said around the same time the GDP number was released that it expects the economy to "grow faster in 2018 than it did in 2017". This marks a departure from the RBA's earlier, and more explicit, forecasts of 3.25% GDP growth in 2018.

In addition, Australian inflation remained subdued and, it turns out, fourth quarter wage growth was driven substantially by a less-important and unsustainable increase in public sector pay, not private sector pay.

Nonetheless, the CIBC Capital Markets team say an interest rate rise could come faster than markets expect. They liken the RBA's current position to that of the Bank of Canada back in early 2017, which faced a lacklustre wage and inflation outlook at the same time as momentum in the economy was also thought to be waning. It turned out that growth actually picked up notably during the first half of 2017 and inflation showed signs of life. This led the BoC to surpise markets with an interest rate rise in July and another in September.

"The OIS market has only around 9bps of tightening priced in by the November 6th meeting. That’s to be too low by our estimates as we expect the initial RBA rate hike to be around then. Correspondingly, the AUD should outperform on a relative basis and also against an overvalued USD over the medium-term," Rai says.

CIBC Capital Markets forecast the AUD/USD rate will rise from its current 0.77 level to 0.83 before year-end as markets respond to an evolving monetary policy outlook. They also project the Pound-to-Aussie rate will fall by some 6% over the rest of the year, dropping from 1.83 on Monday to 1.72 before year end.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.