Image © Adobe Images

Rising interest rates at the Reserve Bank of Australia (RBA) are to force the country's housing market into reverse, according to economists at one of the country's biggest lenders.

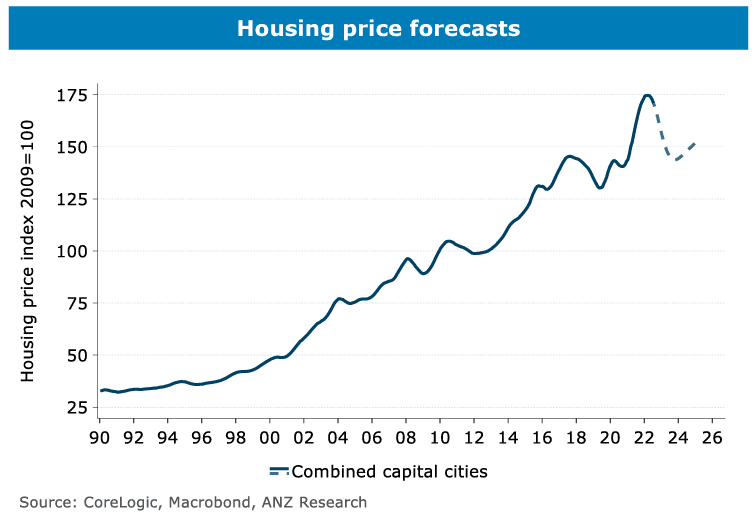

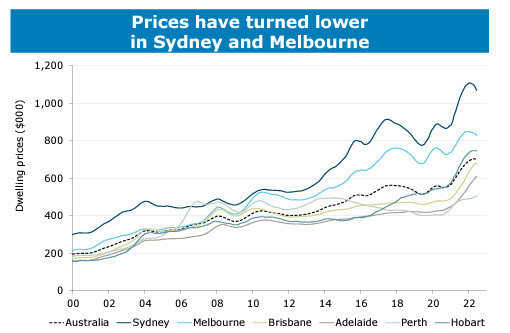

New research from ANZ finds house prices are to fall over the coming two years amidst a steep increase in mortgage rates between May and the end of this year.

The rise in the cost of borrowing comes in line with a steady policy of interest rate rises at the country's central bank, which most economists see ending towards the end of 2022 or early 2023.

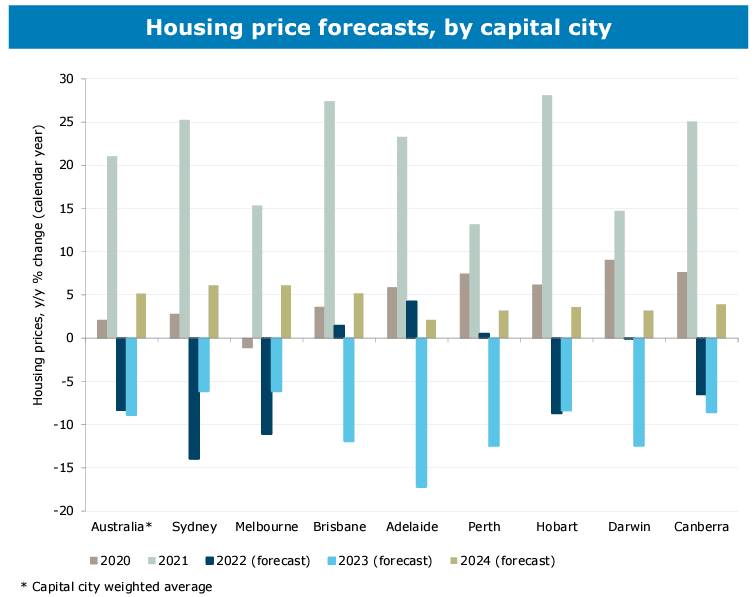

"We expect capital city prices to fall 18% over the balance of 2022 and 2023, before a 5% gain in 2024 as mortgage rates fall," says Felicity Emmett, Senior Economist at ANZ.

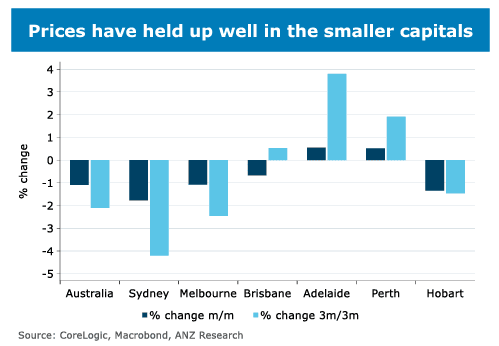

ANZ says the biggest factor driving prices lower will be a reduction in borrowing capacity, not a rise in forced sales.

Arrears rates are coming from a very low base and ANZ says that the number of households that have built negative equity is expected to be modest.

Rising immigration and low unemployment will also all help to mitigate the weakness in housing demand.

Nevertheless, the declines will be noticeable, particularly for new entrants to the market.

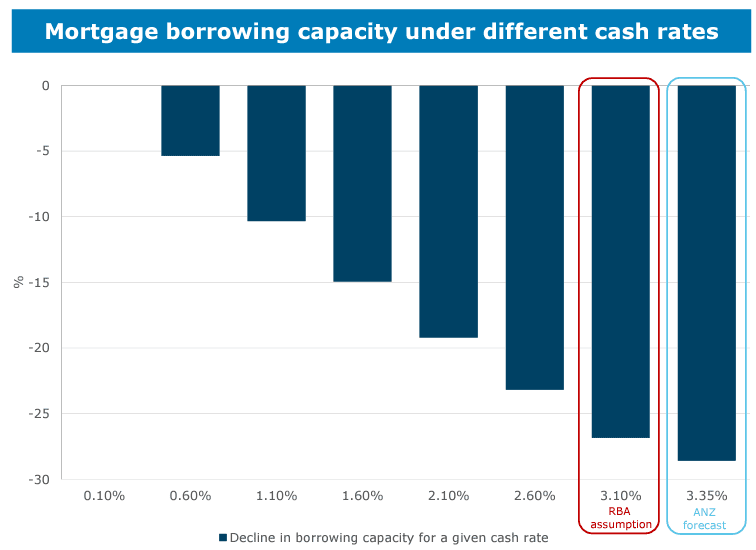

The RBA is expected to raise its basic rate to 3.35% by year-end, which will "significantly lift household interest payments," says Emmett.

A cash rate of 3.35% by end-2022 equates with variable mortgage rates reaching just under 6% according to ANZ economists.

They have calculated the rise in the basic rate will mean the average share of household income that goes to mortgage interest payments will rise to nearly 11% at the peak.

This is "much higher than the 9% or so paid prior to the pandemic".

It is nevertheless well below the 13.50% peak seen in 2008.

Total repayments are also set to rise sharply, with over half of payments on fixed rate loans rising by over 40% once the fixed rate expires, and around 28% of payments on variable loans rising by 40% or more when the cash rate hits its peak.

Already housing finance data show that average new mortgage sizes are beginning to fall.

"Despite these large rises, we know that debt is concentrated among high income households who are more likely than others to have large savings buffers and more income to cover inflation and interest rate changes. The strong labour market will also offset some of the risk," says Emmett.

With the RBA basic cash rate set to peak later this year, ANZ expects most of the impact on prices will be fully reflected by the end of 2023.

"In 2024, we expect to see the beginnings of a recovery in house prices, alongside cuts in the cash rate in the second half. We expect prices to rise around 5% in 2024," says Emmett.