Image © Adobe Stock

-Yen tipped to rise if BOJ alter policy at next central bank meeting as rumoured

- BOJ could be tempted to remove negative deposit rate, 'investigate' solutions or do nothing

- If no-change Yen vulnerable to negative surprise

The Bank of Japan (BOJ) is tipped to make policy changes at its meeting on Tuesday, July 31, which could impact on the Yen.

Rumours have already leaked out of a possible 'tweak' to policy and led to the sudden 1.6% surge in the currency on Monday.

Although the BOJ Governor Haruhiko Kuroda denied these rumours, stating “I know absolutely nothing about the basis for those reports," the feeling is that there is 'no smoke without fire' and something could very well change at the meeting.

Yet analysts differ as to what could change if anything, and the consensus amongst economists is that nothing will change - yet.

The reports and rumours from the BOJ suggested it wanted to make its policy more "sustainable".

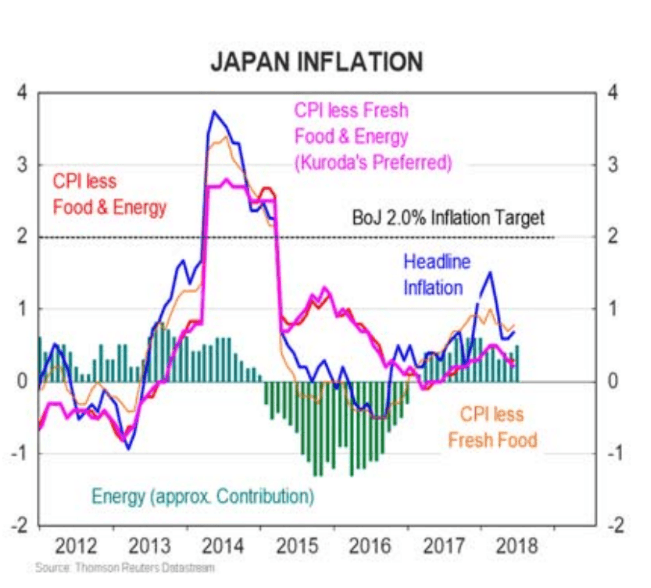

Whilst this could be interpreted in many different ways, most analysts see it as highlighting the dilemma of how its stimulus policies, implemented to raise inflation to a 2.0% target, are having the unwanted side-effect of lowering bank profitability which is causing 'financial stability risks'.

Clearly the dilemma is that if it continues to stimulate the economy by keeping borrowing cheap it will continue to make life difficult for banks whilst if it reduces stimulus to help banks it will raise interest rates and potentially stymie growth and inflation.

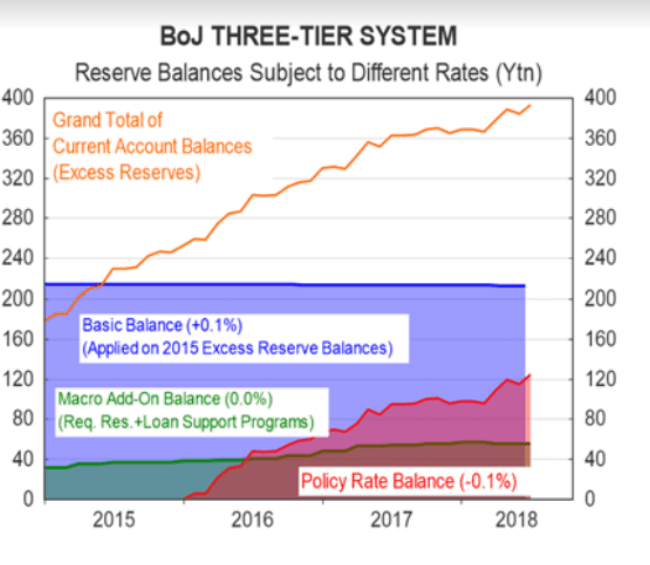

One of the policies which is causing the most pain is the BOJ's 'three tier interest rate system' which charges commercial banks three different rates, on their deposits with them, one of which is a negative -0.1% interest rate.

"The BoJ said that the negative rates decision will only affect some accounts as it adopts a “three-tier system.” Specifically, each financial institution’s current account at the Bank will be divided into three tiers to which a positive, negative and zero interest rate will be applied. The purpose of this is to maintain the stability of lenders; such a system is also used by central banks in Switzerland, Sweden and Denmark," says Jennifer Thompson, a correspondent for the Financial Times, writing about the policy when it was first implemented.

The BOJ introduced the system to encourage commercial banks to lend capital to the real economy rather than leave it with the BOJ to sit and earn risk free interest, yet the policy has largely failed - not because banks are unwilling to lend but because businesses and individuals are reluctant to borrow.

The risks that the 'three tier' system pose make it a prime candidate for reform, according to Commonwealth Bank of Australia (CBA) whose base case is that the BOJ will probably reform this area at the July 31 meeting.

"At the very least, the most likely policy change will be abandonment of the three‑tier interest rate system on current account balances, and the 0.1% negative interest rate on a certain, and growing portion, of current account balances held by financial institutions at the BoJ in particular," says Richard Grace at CBA.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

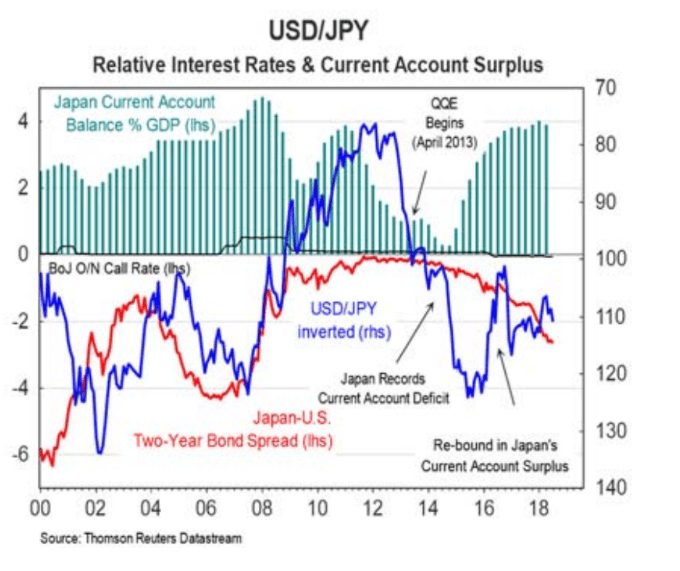

If the BOJ remove negative interest rates this will, however, result in de facto tightening, as banks will almost certainly start to increase their deposits with the BOJ. The reduction in money supply that would result and the overall upward pressure on interest rates would probably result in a stronger Yen, further depressing inflation. Indeed, CBA is watching USD/JPY closely for a move lower.

"We now see downside risks in USD/JPY ahead of a possible change to the QQE with Yield Curve Control policy, which would likely see a modest lift in JGB yields," says Grace.

"We don’t envisage a large rise in JGB yields because of the extreme structurally low inflation environment in Japan. But a modest rise in JGBs would narrow the U.S.–Japan bond yield differentials, and provide some support to JPY," he adds.

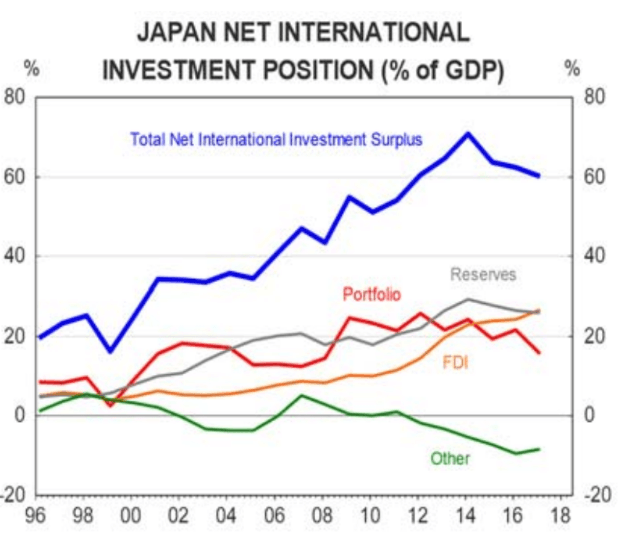

A rise in JGB yields might also lead to a growing repatriation of the relatively large proportion of capital (circa 60%) invested by Japanese investors outside of Japan, who have been in search of yield ever since interest rates fell to minimal levels in Japan decades ago. This too could power the Yen higher as inflows boost demand.

"Japan’s net international investment position is huge at 60% of GDP, indicating there is no shortage of capital that could return to Japan should investors choose to bring it back," says CBA's Grace.

A rise in the Yen off the back of a policy tweak would not be surprising to those who have been flagging up how undervalued the currency has become.

The Yen is the second most undervalued currency in the G10 after the Swedish Krona on a Purchasing Power Parity basis and is circa 33% undervalued according to recent data from Bloomberg.

Hinting at Change

Another possible outcome of the meeting is that the BOJ decides to 'pave' the way for changes later in the year by announcing that it is 'instructing it staff to investigate' how to make policy more 'sustainable' - which is the base case outcome proposed by London-based advisory service Capital Economics.

"Given the risks around being perceived to be tightening, the most likely outcome of next week’s meeting is that the Policy Board simply instruct Bank staff to investigate how best, if at all, the Bank might mitigate the impact of loose policy on the financial sector," says Capital Economics.

This would have the effect of avoiding outright tightening which would make the battle to raise inflation and spur growth even more difficult, but could appease the need for action to help banks on the financial stability front.

"That would leave open the possibility of policy tweaks at the meeting in late October when the next “Outlook for Economic Activity and Prices” is published and when the trajectory of inflation may have improved. Even then though, we suspect that the key policy settings – the anchors for the yield curve – will remain unchanged," says Capital Economics.

No-Change Please

Yet the consensus is for no-change on Tuesday, an outcome advocated by RBC Capital Markets, who also say that this will actually propel the USD/JPY higher.

"On this occasion, we are with the economists and think an unchanged decision will push USD/JPY higher," says Adam Cole, an analyst at RBC Capital Markets.

The USD/JPY has already priced in the 'rumours' of a policy tweak and this is now baked into the price, says Cole, who thinks the pair's strong uptrend will remain intact.

If anything the risks are now for a surprise rise in USD/JPY if the BOJ do nothing.

"Our analysis suggests that the market has moved to price in some form of policy modification by the BoJ on July 31," says Cole.

"As such, we feel that risks have become more asymmetrical should the BoJ refrain from making any changes. Our work highlights key support and resistance levels to watch through this event risk, along with our core views," adds the analyst.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here