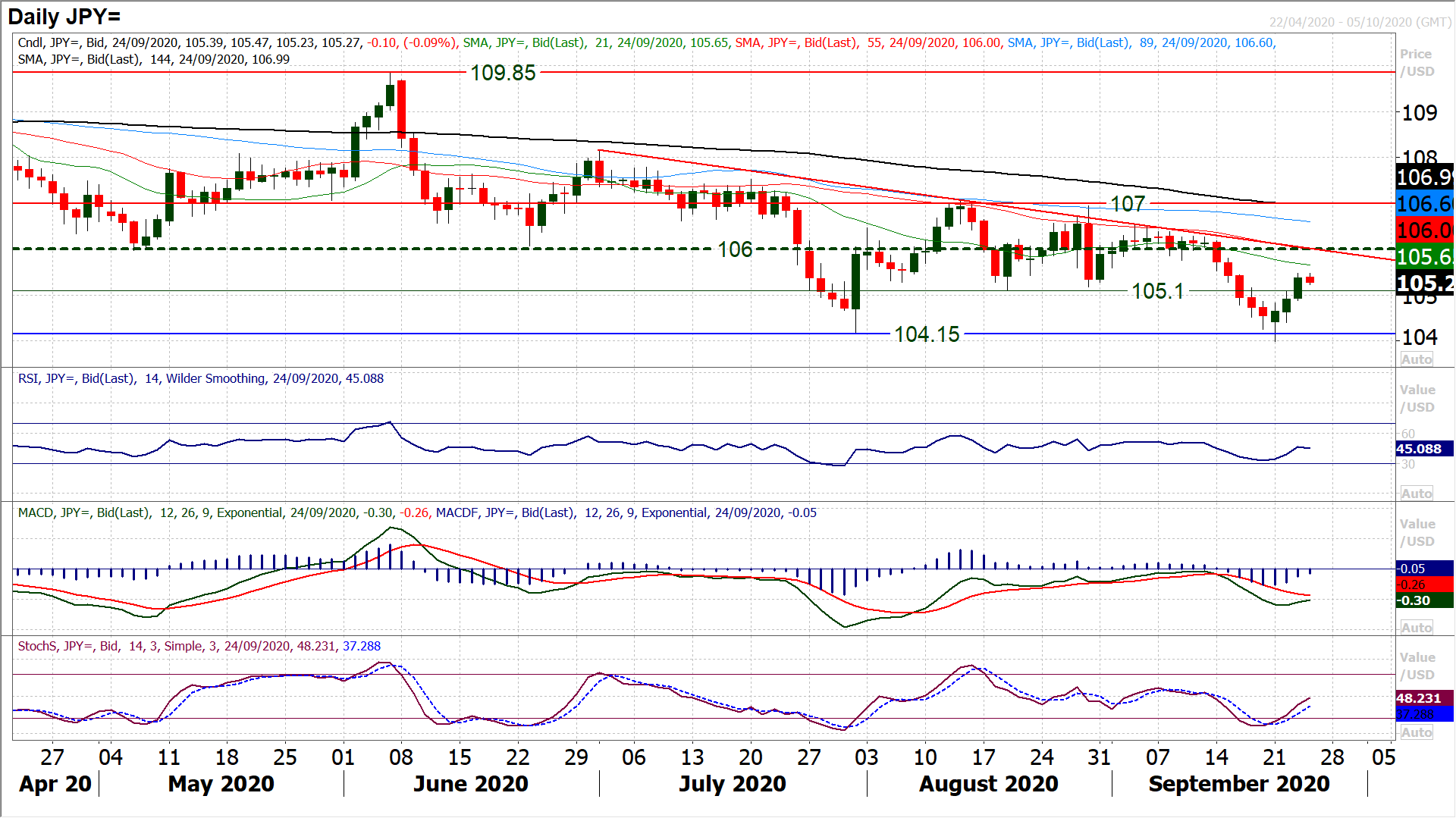

The Dollar-Yen exchange rate is seen at 105.34 on Thursday having advanced on each day of the week thus far. Further gains are possible says analyst Richard Perry of Hantec Markets.

A third consecutive decisively positive candle reflects the impressive recovery that is driving Dollar/Yen higher now.

This strong turnaround is shown in the fact that we now see repeatedly intraday weakness during the European session being used as a chance to buy in the US session.

The hourly chart shows a small base pattern completed above 104.85 which is now a neckline support, in a move that implies 105.70.

The daily chart shows the bulls pulling through the resistance 105.10/105.30 of the overhead supply from old August lows.

This should now open the way towards a recovery to 106.00 in the coming days.

It also means that 104.85/105.30 is a band of support now. Momentum is strong in the move, with Stochastics and RSI swinging higher, whilst there is still upside potential in the move (RSI has hit the mid to high 50s in previous rebounds).

We look to continue to use intraday weakness as a chance to buy into this near term recovery which looks to be unwinding the market back towards the three month downtrend again (currently around 106.00).

Momentum is really taking hold in this risk off, dollar rally now.

In the last few days there has been a real shift in outlook, with the fears mounting over the implications of COVID second waves in countries across Europe and the US.

Safe haven flows continue and the US dollar is benefitting from that.

The significant dollar negative positioning that has developed over the past few months is driving traders into a short-covering dollar rally now.

The comments of Fed chair Powell have hardly helped to stem the tide either.

Powell noted yesterday that fiscal support for the economy is vital in the battle against the impact of the pandemic.

However, it seems increasingly unlikely that Congress will be able to agree anything this side of the Presidential election in November.

That is not good for risk and helps to further fuel this flood back into the dollar.

UK Chancellor of the Exchequer Sunak (finance minister) is though expected to announce new fiscal measures for the UK today, but it is in the US Congress where markets would really take notice.

Fed chair Powell speaks once more today, this time with Treasury Secretary Mnuchin too. Will Mnuchin signal some much needed fiscal response?

What to Expect Today

There is a European bias to the economic calendar today. With SNB monetary policy first up at 0830BST, there is no change expected to the deposit rate of -0.75%.

Then the German Ifo Business Climate is at 0900BST, with a mild improvement to 93.8 in September (from 92.6 in August), driven by improvements in both expectations and current conditions.

Later in the session the US New Home Sales are at 1500BST and are expected to reduce by around -1.2% to 890,000 in August (from 901,000 in July.

For a final time this week Fed chair Jerome Powell testifies before the Senate Banking Committee at 1500BST along with Treasury

Secretary Steve Mnuchin about the CARES Act.

Once more, any clarity on Fed monetary policy could drive volatility.

There is another Fed speaker today too, with John Williams (centrist) at 1900BST.

We also note that Bank of England Governor Bailey is speaking at 1500BST, with the focus still on the potential for negative rates.