-USD falls after a "dovish" set of FOMC minutes jilt a hawkish market.

-"Gradual" pace of hikes, modest inflation "overshoot", order of the day.

-TD Securities eyes weaker USD, says sell USD/JPY, it's headed to 105.

© Xiong Mao, Adobe Stock

The US Dollar fell during overnight trading and into the London session Thursday as traders responded to the minutes of the latest Federal Reserve monetary policy meeting, which were interpreted by the market as being on the "dovish" side of expectations and so, bad for the greenback.

Wednesday's minutes showed a majority of Federal Open Market Committee members agree another interest rate rise will be appropriate "soon" but otherwise appeared to overlook the current level of US inflation, as well as the prospect of US consumer price growth continuing to exceed the Fed's 2% target in the months ahead, leaving the meeting record devoid of the hawkish tones that would have been necessary to boost the Dollar.

"What we don't see in the minutes is much clarity on the specifics of follow-up rate hikes, leaving our view that there's only one more this year after June (and three more in 2019) neither confirmed or denied. Perhaps a tad more dovish than what markets had started to build in, given the lack of real concern about overheating and a tolerance for a bit of overshooting on the inflation front," says Avery Shenfeld, chief economist at CIBC Capital Markets.

The Federal Reserve held its interest rate target range steady at 1.5% to .75% at the beginning of May while the statement accompanying the decision appeared to show policymakers discouraging markets from betting on a faster pace of interest rate rises during the months ahead.

Rate setters said they expect inflation to "run near the Committee's symmetric 2% objective over the medium term", which marks a step change from their earlier forecast that inflation would "move up in the coming months".

But this came as data showed the US consumer price index rose to 2.5% during April, above the Fed's 2% target, while the more important core measure of inflation held steady at 2.1%. Other measures of inflation, such as the Fed's preferred personal consumption expenditures index, are also sat at 2%.

Markets interpreted the statement at the time to mean rate setters would be willing to tolerate a so called "overshoot" of the target for a period of time, instead of rushing to raise interest rates further as that would risk damaging the economy if the recent increase in price pressures proved to be only temporary.

"Policymakers disagree on where the neutral funds rate is and, therefore, how much more tightening will be necessary, but for now there's broad agreement that the "gradual” normalization can continue," says Ian Shepherdson, chief US economist at Pantheon Macroeconomics. "In short, then, the FOMC still thinks it has the luxury of time to see the full impact of the fiscal easing and the uncertainty over foreign trade, so a shift to a more aggressive stance - dropping "roughly balanced” risks, for example - is still some way off."

Wednesday's minutes did little to discourage this view but, nonetheless, provided too few clues on the pace of future rate hikes for pundits to change their entrenched views on the trajectory of US monetary policy.

As a result, analysts and economists remain split into two camps, which are divided between those who forecast the Fed to maintain its current pace of three rate rises per year and those who expect an increase to four.

"We doubt that officials will be so relaxed about inflation rising above the target over the coming months, and continue to expect three more interest rate hikes this year, with the next move coming in June," says Andrew Hunter, an economist at Capital Economics.

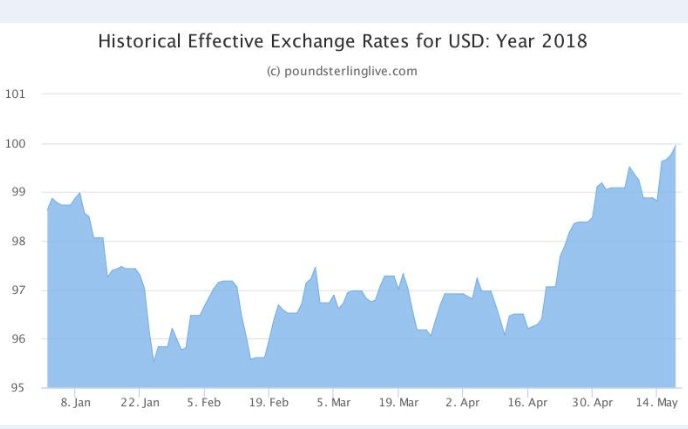

Above: US Dollar index in 2018. Captures April and May rally.

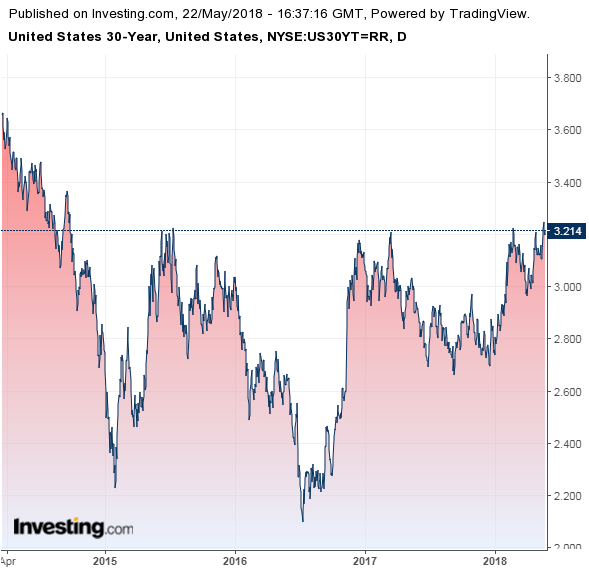

Wednesday's FOMC minutes came after a weeks-long period in which US 5, 10 and 30 year bond yields reach mulit-year highs of 2.94%, 3.15% and 3.25% respectively, which shocked the US Dollar back into life and helped it convert a 3% 2018 loss into a 1.38% gain.

Above: 10 Year US Government Bond Yield.

This has been a game changer as it has altered the relative returns equation for international investors and so called carry traders so that a greater number of those money managers are now incentivised to sell a range of other currencies in order to by the Dollar and invest in the American bond market to exploit these higher US yields.

"We think the USD could easily be vulnerable to a dovish tone – such as greater comfort with an inflation overshoot narrative – or perhaps evidence of a robust discussion about yield curve flatness. The latter has been top of mind for many investors as the 5s30s curve is not far from inversion and the inevitable concern that will spread of an impending recession because of it," says Mazen Issa, an FX strategist at TD Securities, in a note ahead of the release.

With Wednesday's minutes and the subject of inflation overshoots aside, Issa's statement strikes right at the heart of how and why the FOMC might show concern for the economic outlook at some time in the future. Notably, as much as yields have risen during the last month or more, the difference between short, medium and longer term borrowing costs in the US is strikingly low. Such that the so called "yield curve" has begun to appear flat when viewed on a chart.

Above: 30 Year US Government Bond Yield.

In ordinary times the curve should be upward sloping as borrowing over a 30 year period would typically be much more expensive than borrowing over just a two year period. Instead, the curve is flattening and economists are now debating whether this levelling of short and long term rates is a sign of the market calling last orders on the current economic cycle and pricing in an eventual recession - which would explain lower interest rates further out along the "curve".

"Given the mature stage of the economic cycle and wider deficits forecast for the foreseeable future, we are sympathetic to this view. But we do not see immediate risks on the horizon. In the past, it typically isn't until when policy becomes too tight that the yield curve inverts," Issa adds.

Issa and the TD Securities team say the yield curve is unlikely to invert, or in other words become downward sloping, at any point in the near future but they do flag that the move in US bond yields has been so swift it won't take much to see yields ease back from their recent peaks. If and when bond yields do this they would almost certainly take the US Dollar lower with them.

"The FOMC minutes confirmed that the Fed is tolerant of an inflation overshoot, suggesting unattractive risk/reward of pricing in more hikes. Against this backdrop, and with USDJPY rekindling its romance with 10yr USTs, we expect the pair to exhibit the first signs of USD fatigue", Issa says. "Trade rhetoric and geopolitical tensions have also intensified, while the situation in Italy - though overblown in our view - remains fluid. This is not a conducive backdrop for risk."

Issa and the TD Securities team have recommended that clients of the bank bet on a fall in the USD/JPY rate over the coming weeks, entering trades around Thursday's 109.50 level and targetting a move down to 105.0. They have a stop loss at 112.10.

The US Dollar index was quoted 0.12% lower at 93.82 at the London open Thursday while the USD/JPY rate was 0.29% lower at 109.54. The Pound-to-Dollar rate was 0.13% lower at 1.3352 and the Euro-to-Dollar rate was 0.05% higher at 1.1716.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.