The US Dollar exchange rate complex fell back after the US Federal Reserve opted to temper expectations for an imminent interest rate rise with the release of their July 27th statement.

- US FOMC statement prompts broad-based USD decline

- Losses to be shortlived say ING, who have expressed surprise at the market's reaction

- Deutsche Bank see potential 5% upside in US Dollar index

- Westpac's propriotory model increases exposure to USD

The US Federal Reserve's Open Market Committee statement released on July 27th proved to be no game-changer for those watching the US Dollar based on US interest rate expectations.

While the Fed said that it continues to closely monitor global and financial developments (same as in June), it did upgrade its assessments of the economy and the labour market.

It now suggests that risks have diminished which is a new and significant addition.

"The takeaway is that the Fed is clearly eying higher rates this year. The dollar reacted positively initially, but the move was quickly corrected and the dollar weakened as the FOMC refrained from sending any clear signals of a September hike," says Erica Blomgren at SEB.

Treasury yields and the Dollar dropped while the S&P 500 erased earlier losses ending the day -0.1%.

Some analysts have expressed surprise to the market’s reaction in driving both US rates and the Dollar lower after the FOMC statement.

The Fed did generally acknowledge the recent pick-up in US activity and most commentators have interpreted the phrase that ‘near term risks to the economic outlook have diminished’ as meaning that a December rate hike could be possible after all.

"Yet market pricing of a December rate hike (which was already under 50%) actually fell. We still like the USD on a near term basis (particularly against Europe), so would expect overnight losses to be recouped – perhaps when US 2Q16 GDP is released tomorrow," says Chris Turner at ING in London.

Latest Pound / US Dollar Exchange Rates

| Live: 1.3479▲ + 0.36%12 Month Best:1.3867 |

*Your Bank's Retail Rate

| 1.3021 - 1.3075 |

**Independent Specialist | 1.329 - 1.3344 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

5% More USD Upside

Alan Ruskin, analyst with Deutsche Bank, and his team believe that even a dovish FOMC is likely to view the probability of a rate hike this year as significantly above what the market has priced, but will be reluctant to signal far in advance of the September FOMC meeting, for fear that they are forced to retreat again in the face of unexpected data or events.

"Nonetheless, the evolving Fed rhetoric is expected to support the more constructive USD tone in coming weeks and months," says Ruskin.

It is expected by Deutsche Bank that the USD could appreciate at least 5% on a broad trade weighted basis, before USD strength would again undermine US financial conditions to the point where it would impact Fed policy, in turn limiting USD strength.

Westpac Seen Increasing Exposure to USD

A recent rapid improvement in US dollar economic fundamentals has seen Westpac Institutional Bank's G10 FX Model increase portfolio exposure to the US Dollar.

USD exposure in the portfolio now stands at 12.2%, the highest of the G10 behind the Yen and the Euro which both have 16% shares.

The increased exposure to the US Dollar comes at the expense of the Australian Dollar which has fallen to a mere 4.2% from above 20% in the previous week.

The Westpac G10 FX model is a multi-factor approach to systematically trading the G10 currencies. The overall system includes a forecast model and a currency portfolio model.

Economic fundamentals analysed by the model include the difference between 2-year sovereign bond yields, relative central bank balance sheet trends, relative growth and world energy prices.

"This sort of sudden improvement in economic fundamentals is normally as a result of falling commodity prices and a radical reappraisal in Federal Reserve rate rise expectations," says Westpac’s Franulovich.

Westpac report that their analysis has shown 'fair value' for the USD index has risen sharply over recent weeks with some of the biggest gains in recent history, close to 3-4%.

It is noted too that such rapid advances in fair value are relatively rare and are usually triggered by either sharp falls in commodity prices and/or a significant repricing of Fed tightening expectations.

Interestingly, both of these factors have boosted USD fair value so far in July - there has been a slight repricing in Fed tightening expectations and commodity prices are lower.

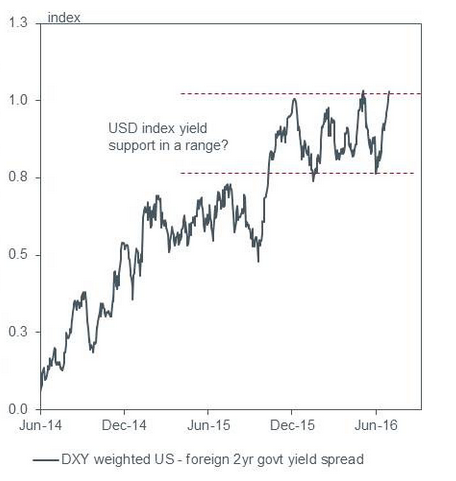

Two-year US Treasury bond yields are now 100 basis points in USD favour – an extreme reading in the dollar’s favour, and about as ‘good as it gets’ from a yield differential perspective for USD.

Higher yields lead to currency appreciation as they attract more foreign capital seeking higher rates of return.

Despite showing a lot of strength, Westpac’s Franulovich says US Dollar fundamentals may also now be stretched.

“The run-up in yield spreads in the USD’s favour may be nearing a peak and the fall in commodity prices does not seem like it will accelerate sharply.”

He notes how commodities may not have much lower to go, pointing to signs Chinese financial conditions are improving:

The upshot is that the Dollar index is likely to rise in the short-term to 100 perhaps, but will probably struggle to overcome that level due to a recovery in commodity prices and a snap back in overstretched yield differentials.

JP Morgan Neutral on the US Dollar

The view held by Westpac is marginally more bullish to that held at JP Morgan who remain neutral the Dollar, arguing for it to continue oscillating within a range.

JP Morgan’s John Normand argues the dollar gained more as a result of the ‘fortuitous’ weakness of its foes then from its own intrinsic strength:

“These include Brexit’s run-up and aftershocks, Trump’s threats, PBoC policy and Japanese whispers about helicopter money. With so many themes in play, the dollar has been able to gain over the past three months despite fitful swings in Fed rhetoric and in US rates.”

Nevertheless, they see little reason to revise up their forecasts of the dollar:

“There is no change to the view outlined in the mid-year outlook that the JPM USD Index will continue to respect the 115 to 122 range it has occupied for the past year, and that the more interesting opportunities and risks are pair-specific.”

Whilst JP Morgan are sanguine about the dollar, it is Westpac’s more positive outlook which is the one shared more broadly, and there is no doubt the current outlook looks substantially better for the dollar.