Image courtesy of City Index.

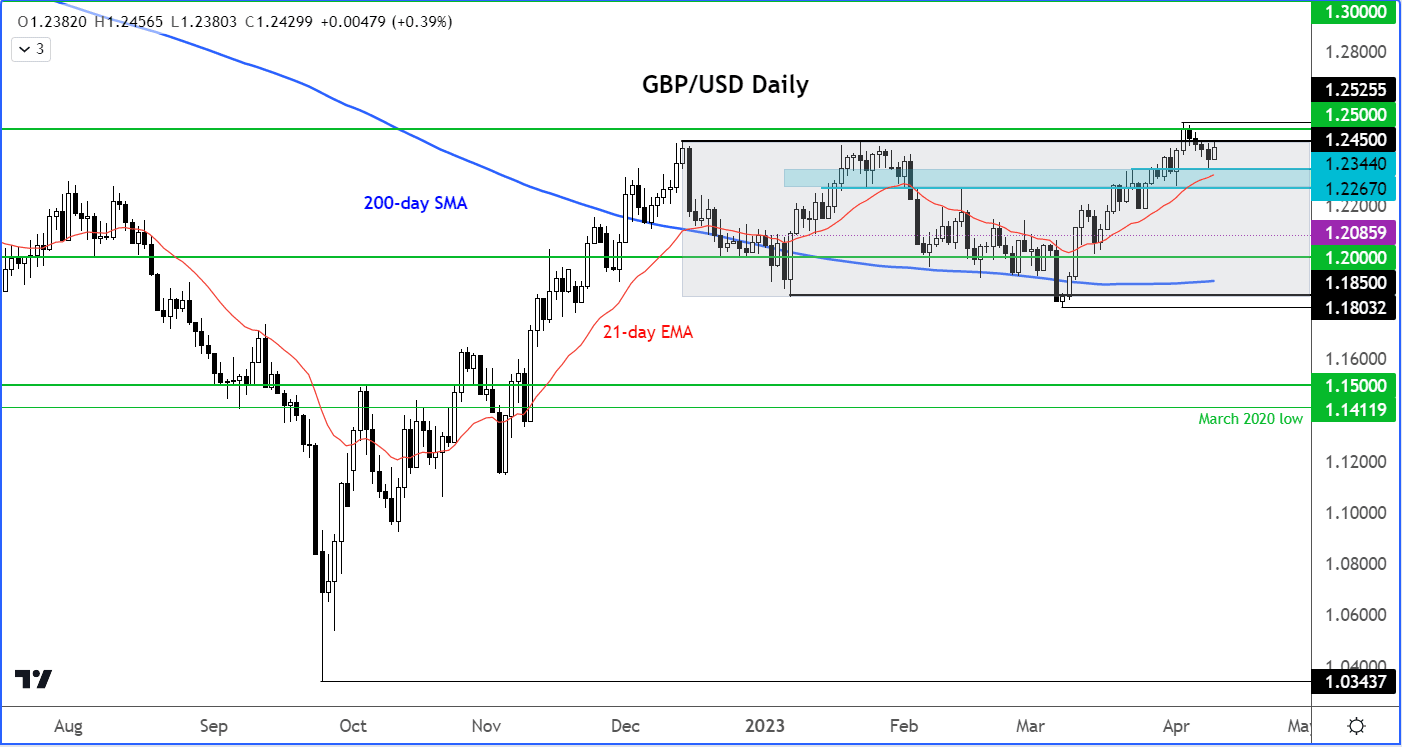

The GBP/USD reached the 1.25 handle last week, before dipping back below the high of its prior range around 1.2450. This level is now very important.

A daily close above 1.2450 would confirm that the bullish trend remains intact. In that case, we could see the onset of a rally towards the high 1.20s or even low 1.30s.

However, if the GBP/USD goes below the shaded blue area first, and thus breaks key short-term support in the range between 1.2265ish to 1.2345ish, then this would put the bulls in a spot of bother.

In this case, a move back towards 1.20 would become likely.

As things stand, we are leaning towards the bullish side of the argument given the recent price structure.

The U.S. dollar traded higher during Easter Monday after finding some support on the back of Friday’s U.S. non-farm payrolls report.

GBP/USD Forecasts Q2 2023Period: Q2 2023 Onwards |

But at the time of writing most of those moves had unwound and the likes of the EUR/USD and GBP/USD were back at pre-NFP, while gold rose back above $2K and Bitcoin climbed north of $30K for the first time since last June.

Investors will be looking forward to the release of some key data this week to provide fresh impetus for the FX majors.

Thus, there’s a chance we will see continued range-bound activity until at least the middle of the week in the dollar, before it establishes a clear directional bias.

Our GBP/USD forecast remains bullish.

Key Events that will Impact GBP/USD This Week

Thursday’s UK data dump aside, it is clear that the GBP/USD forecast will be impacted mostly by the release of macro data from the west side of the Atlantic this week.

Wednesday’s publication of U.S. Consumer Price Index is likely to be the most interesting one.

Unless we see a much weaker CPI print, then this should make the case for a 25bp Fed hike on 3 May.

U.S. CPI and FOMC minutes (Wednesday, April 12)

Thanks to weakness in US data, the market has been repricing lower the Fed’s projected interest rate path in recent weeks, causing a significant downward move in the dollar.

The market will continually question whether this is the right approach. So, a lot of attention will be on CPI as investors try to front-run the Fed.

Headline CPI is expected to have fallen further to 5.2% year-over-year in March from 6.0% the month before. Core inflation is seen edging higher to 5.6% from 5.5% previously.

There will be more inflation data on Thursday in the form of PPI. However, the latter is not going to be as important as the former.

The FOMC meeting minutes will be released later in the day, and they will reveal some of the Fed's thinking behind the 25bp hike in March, amidst the banking crisis.

If the minutes reveal concrete signs that the central bank is very close to a peak in interest rates, or policymakers confirm the market expectation of cutting interest rates later in the year if needed, then this would likely be seen as dollar negative.

US Retail Sales and UoM Consumer Confidence (Friday, April 14)

The Fed’s rate projections have been cut sharply in recent weeks owing to weakness in US data and signs of peak inflation.

Worries over the health of US consumers will intensify if we see a weaker print in either retail sales or consumer confidence, especially as they are going to feel the impact of higher gasoline prices in light of OPEC’s decision to sharply cut crude production. Both headline and core retail sales are seen falling 0.4% month-over-month.

The University of Michigan’s consumer confidence index is a more forward-looking indicator of consumers' health and may thus trigger a sharper move in the dollar should we see a bigger-than-expected deviation from the expected 62.0 reading.

Fawad Razaqzada is an analyst for City Index and Forex.com