- GBP/USD facing a battle to hold 1.38 this week

- Risks slippage to 1.37, finds resistance at 1.40

- FOMC minutes dominate ahead of UK GDP data

Image © Adobe Images

- GBP/USD reference rates at publication:

- Spot: 1.3810

- Bank transfers (indicative guide): 1.3420-1.3523

- Money transfer specialist rates (indicative): 1.3686-1.3713

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Pound-to-Dollar exchange rate enters the new week near to three-month lows and with minutes of June’s Federal Reserve (Fed) meeting threatening to keep the greenback on its front foot, Sterling could now face a battle to hold onto the under-pressure 1.38 handle.

This coming Friday’s GDP data for the month of May is the highlight for Sterling in the week ahead given that it will reveal the extent to which the economic recovery is thus far living up to Bank of England (BoE) forecasts.

GDP data would impact Sterling through the effect that the report has on market expectations for interest rates and other BoE monetary policies, although before then investors and traders will likely give the bulk of their attention to Wednesday’s 19:00 release of minutes from last month’s meeting of the Federal Open Market Committee (FOMC) at the Federal Reserve.

“The 850,000 rise in non-farm payrolls in June may be a sign that some of the temporary labour shortages holding back the employment recovery are starting to ease. But with the labour force rising by just 151,000 and still more than three million below its pre-pandemic peak, we aren’t entirely convinced that this is the start of a much stronger trend,” says Andrew Hunter at independent research and consultancy Capital Economics.

“The key event next week will be the release of the minutes from the Fed’s June meeting, which are likely to provide more details of discussions about asset purchase tapering,” Hunter adds.

Wednesday’s minutes are set to hit the wires hard on the heels of June’s non-farm payrolls report, which showed employment rising by almost 1 million last month and lifted the six-month rolling average of payrolls growth to a robust 481k.

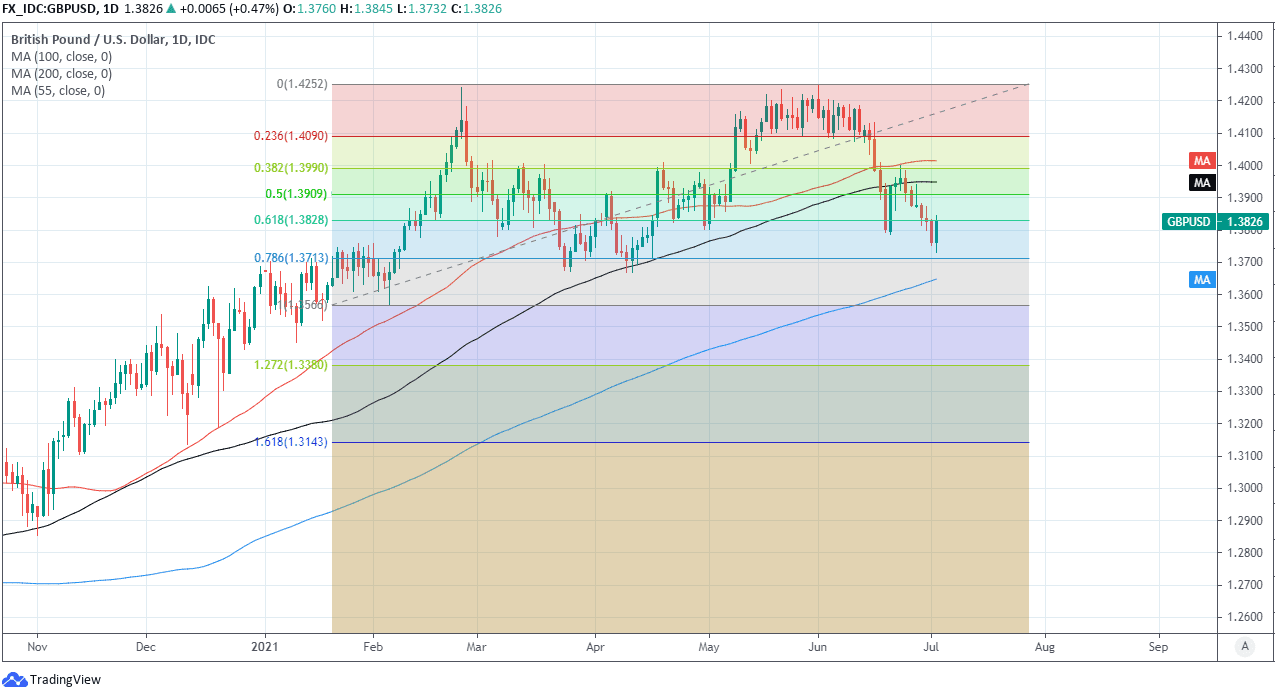

Above: Pound-to-Dollar rate shown at daily intervals with Fibonacci retracements of Feb-to-June rally indicating support levels, alongside selected moving-averages.

In the event that U.S. employment growth continued in line with that average over the coming quarters it would take just less than the eight months to February 2022 in order for the American job market to return to its pre-pandemic level of employment where there were 5.7 million people who met the official definition of unemployed, although there was still 9.5 million such people last month.

It’s arguably if-not evidently unlikely that the U.S. labour market would continue to be repaired at the same rates seen in the recent months immediately after the reopening of state economies which chose to impose the ‘lockdown’ measures used in other countries, which is partly why Wednesday’s FOMC minutes will be scrutinised so closely by the market for clues on the timing of forthcoming changes to Fed policy settings.

“The sluggish dollar performance on Friday probably owed to profit-taking ahead of the Independence Day holiday and some large FX option expiries,” says Chris Turner, global head of markets and EMEA regional head of research at ING.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

“US trading will likely be quiet in a shortened holiday week. The calendar is quite light, with the highlight probably being the release of the FOMC minutes on Wednesday evening. Much focus will be given to how the doves and hawks are arguing their cases,” Turner adds.

The Dollar ended last week on its back foot even after Friday’s payrolls surprise, enabling the Pound-Dollar rate to rise back above a 1.38 handle that had appeared in danger of ceding and potentially indicating the directional bias of the U.S. currency ahead of this Wednesday’s minutes, although it’s the market’s reading of and response to the minutes that will dictate how and where GBP/USD ends the week.

The risk is that Wednesday’s meeting notes bring attention back to bear on the Fed’s $120 billion per month quantitative easing (QE) programme and questions about what would be the most appropriate time to begin winding it down and the pace at which such an exercise should be carried out; potentially leading to increased bond yields and, or a bid for the Dollar in the latter half of the week.

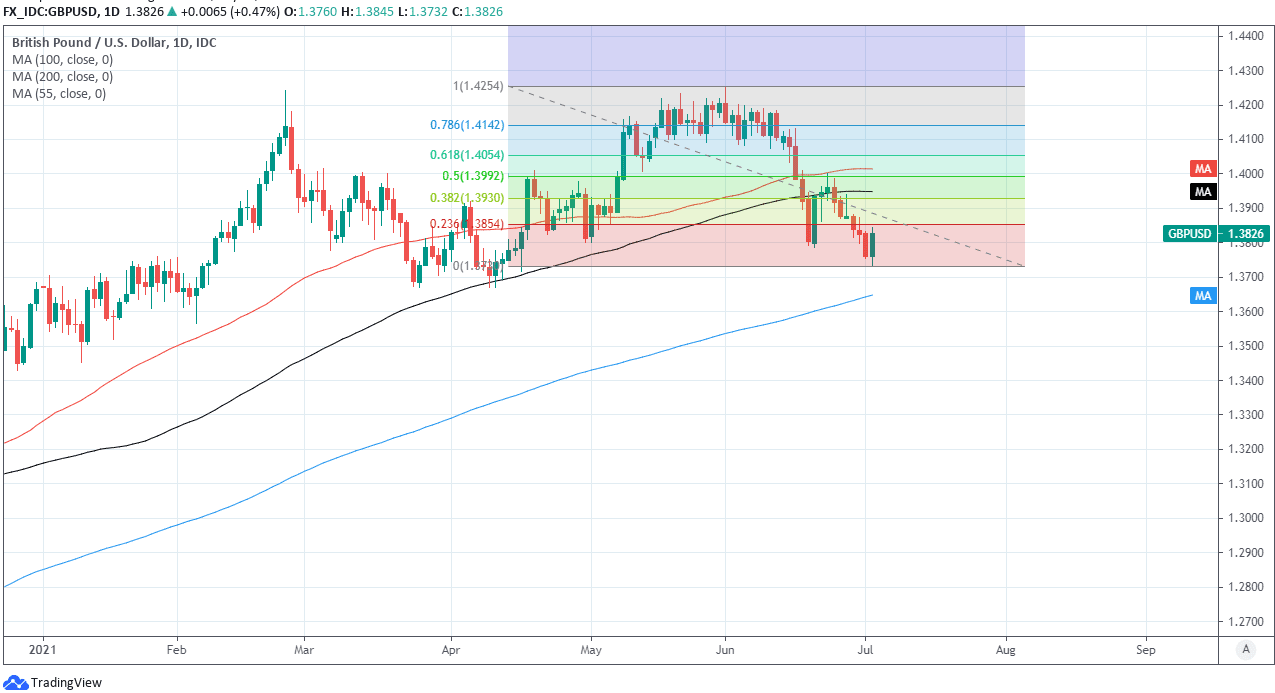

Above: Pound-to-Dollar rate shown at daily intervals with Fibonacci retracements of correction from early June highs and key moving-averages indicating possible areas resistance to any recovery.

“The US fiscal stimulus is by far the largest in G10, helping the US outgrow the rest of the world and likely supporting USD this year and possibly next. The Fed is on track to announce tapering at an upcoming meeting, and we continue to think the September meeting is most likely, with tapering starting at the turn of the year,” says Michalis Rousakis, a strategist at BofA Global Research.

“Our key difference with the consensus is that we expect the USD to rally against currencies of central banks that will not be normalizing policies, including EUR, CHF, JPY and SEK, but not necessarily against the rest. Indeed, this is exactly how G10 FX has performed this year, with CAD, GBP, USD and NOK at the top, JPY, CHF, SEK and EUR at the bottom, and AUD and NZD in the middle,” Rousakis adds.

The Dollar has been lifted in the last month by a lessening of bearish sentiments toward it which was brought about by evolving expectations for Fed policy, with investors and traders increasingly wagering that the bank could raise its interest rate before the end of next year, before lifting it back to 1% by the end of 2023 even as Chairman Jerome Powell poured cold water over other policymakers’ suggestions that any changes to interest rates are in any way likely within this time period.

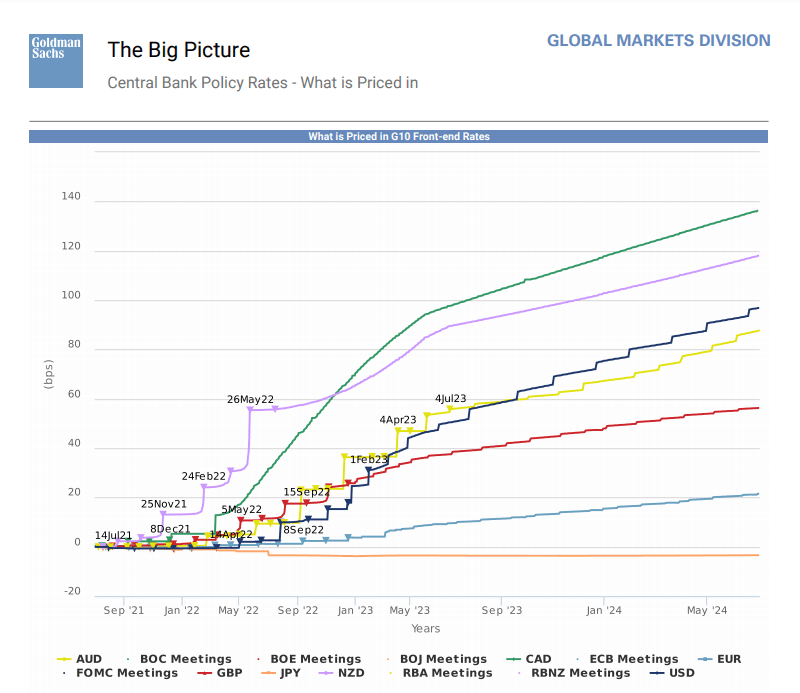

Above: Goldman Sachs graph showing market expectations for changes in major central bank policy rats (BoE in red).

“There are still a number of open questions around the Fed’s balance sheet, including the taper announcement timeline, the duration of the tapering process, and whether the committee will rule out rate hikes while the balance sheet is still growing,” says Zach Pandl, co-head of global foreign exchange strategy at Goldman Sachs.

Prospects for U.S. interest rates have dominated the market conversation even as Chairman Powell and others made clear in June that the Fed’s policy priority is the government bond buying programme and its eventual, gradual winding down, details of which may or may not be revealed by Wednesday’s meeting minutes: To the extent that these do reveal anything about the likely timing of a decision by the Fed to reduce its footprint in the U.S. government bond market they will determine whether the Pound-Dollar rate holds onto or gives up the 1.38 handle ahead of Friday’s GDP report.

“Minutes from the June 15-16 FOMC meeting, released on Wednesday, may help clarify Fed officials’ views on the exit path. While maintaining our forecasts for broad Dollar depreciation over the medium-term, for now we remain broadly neutral on USD vs G10, while sticking with recommended USD shorts in “deep value” EMs (BRL and RUB),” Goldman Sachs’ Pandl says.