- USD fades as Fed set to update on new approach to inflation.

- Policy settings seen unchanged ahead of year-end adjustment.

- But a surprise extension of bond buying programmes possible.

- Additional action would weigh USD rates & support GBP/USD.

Above: Federal Reserve Chairman Jerome Powell. Image © Federal Reserve.

- GBP/USD spot rate at time of writing: 1.2893

- Bank transfer rate (indicative guide): 1.2566-1.2656

- FX specialist providers (indicative guide): 1.2724-1.2802

- More information on FX specialist rates here

The Dollar faded on Wednesday as a prior rebound melted away ahead of September’s Federal Reserve (Fed) policy decision in which the bank is expected to set out how its actions could change in the months ahead as a result of a new inflation targeting strategy announced in August.

Dollars were sold widely, with all major U.S. exchange rates quoted lower as stocks crept higher alongside major economy bond markets in price action that might indicate caution among some investors ahead of Wednesday's Fed meeting and after the U.S. indicated it could ignore a World Trade Organization ruling on its Chinese trade tariffs.

U.S. retail sales for August will be released at 13:30 and could cultivate a somber and enhanced soft-Dollar backdrop ahead of the Fed decision if sales growth falls off the edge of a cliff in response to lawmakers' failure to extend enhanced unemployment benefits provided by the CARES Act beyond July.

"A dovish Fed this evening could see the world’s reserve currency weaken further. EUR/USD has consolidated around the $1.18-$1.19 zone, but could look to re-test $1.20 ," says George Vessey, a currency strategist at Western Union Business Solutions. "If a deal isn’t reached by the EU summit on October 15, the probability of a no-deal scenario is likely to increase, and history would suggest GBP/USD could fall to $1.20.”

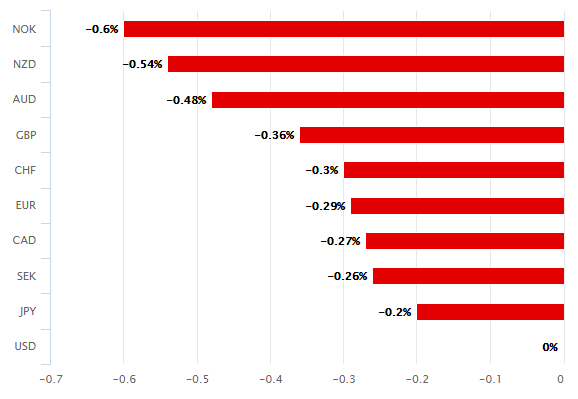

Above: U.S. Dollar performance against major counterparts on Wednesday. Source: Pound Sterling Live.

Consensus sees interest rates unchanged at between 0% and 0.25%, leaving market attention fixated on the level of government bond buying under the Fed’s quantitative easing programmes and its new economic forecasts which, if anything, are seen as likely to be upgraded.

The decision is a closer-than-usual call for the foreign exchange market given the Fed’s late August announcement that it will move to a so-called average inflation targeting framework where it leaves interest rates and other policy settings unchanged for a period of time even after the consumer price index (inflation) rises above the 2% target.

“We expect a change of forward guidance and an increase in QE buying. We think the Fed will recognise the importance of building up credibility right away, especially as inflation expectations remain subdued,” says Kristoffer Kjær Lomholt, an analyst at Danske Bank.

The Fed's new idea is that such an ‘overshoot’ of the inflation target would make amends for past periods where consumer price growth has run an for extended periods below the target level only to elicit rate hikes from the bank almost as soon as it’s risen above the objective, if not before then.

"The Fed has now made an inflation overshoot an explicit policy objective, in the wake of an almostunbroken 12-year streak of undershoots in the core PCE measure. They aren’t going to blink anytime soon, even if core PCE inflation hits 2.5% next spring; it won’t stay there for long, because base effects will push it back down again in the second half of the year," says Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Above: Dollar Index shown at daily intervals.

It’s thought by policymakers that sparing the economy from sooner-than-otherwise interest rate hikes will bolster the economy’s long-term inflation-producing capacity and deliver the target level in a more sustained way, but the Fed has often seemed like a passenger on its own train in recent years.

Some analysts have suggested it the Fed might announce further action this Wednesday due to perceived policymaker fears that they might not be able to deliver the above-target price growth which has recently been promised.

"The market expectation is that the Fed’s new ‘dot plot’ forward guidance will be prepared to flag rates on hold until well into 2023. That sounds decidedly optimistic. Why not 2025? So let’s see what Powell says today: be still, my beating heart,” says Michael Every, a market strategist at Rabobank. "The argument is then between those who think the Fed watching the weeds grow and waiting for inflation to sprout is bullish emerging market FX, and those who think the fact that the Fed is having to do that means that EM central banks will be diving in with debt monetisation, which is very bearish. Therein still lies some kind of market. Until they ban or supress it."

All major central banks have struggled to deliver their inflation targets at least in the last decade. U.S. inflation has been above its target in recent years, although this was the result of White House tax reform and no thanks to the Fed, which raised interest rates at a more rapid pace almost instantly out of fear that inflation would lift above the target as it eventually did.

Similarly, the Bank of England saw inflation rise above its own 2% target and as far as 3.1% in November 2017, although this resulted from currency devaluation and rising import costs kicked up by the Brexit vote, which the BoE never welcomed under its previous governor, more than anything the bank itself did.

“The inflation they cannot generate will now be measured over the medium term, which effectively means they will have nothing to do for years as they fail to see inflation rise: just look to Japan, where a new Suga Daddy is taking over stewardship of the Good Ship Structural Deflation. Or Europe," Every adds.

Above: Euro-to-Dollar rate shown at daily intervals.

The Federal Reserve has created $2.9 trillion, an amount equal to 14.3% of annual GDP for the world’s largest economy, since the beginning of the pandemic in order to support an extraordinary array of new policy programmes intended to facilitate government support of companies and households throughout the coronavirus shutdown.

"Extrapolating the Fed’s 2021 and 2022 median projections from their June update into 2023 would yield a reasonable core PCE projection in the region of 1.9% and an unemployment around 4.5%. While that would mark ongoing progress, these forecasts would still leave the Fed short of its long run goals, not to mention their plans for “moderately above 2% inflation” and a hotter labour market," says Robert Rennie, head of strategy at Westpac. "While the Fed is unlikely to deliver fresh accommodation this week a close look at 2023 under the spotlight of average inflation targeting would surely compel them to at least consider the option. Powell could open the door to it at this meeting.”

An overwhelming majority of the new money created by the Fed has been directed into bond markets where the bank has bought mostly government bonds but also corporate debt including for the first time, liabilities that are of low credit quality and so rated as so-called ‘sub investment grade.’

The bank has also spent money and time buying up small business and other loans directly from commercial lenders, broadening accessibility for an essential crutch of support during a time when government actions taken in response to the pandemic had crippled economies, companies and households alike.

But most of these are due to expire at year-end unless extended for a second time. The Fed said last that it'll continue “in the coming months...at least at the current pace,” and few analysts expect a withdrawal of support any time soon given the coronavirus still disrupts the economy.

“Chair Powell will be asked how the Fed ‘reaction function’ will change. This will be where the Fed will need to send a more dovish message to the market to reinforce the prospect of ‘lower for longer’. Of course how aggressive and explicit Powell is with those comments will be important for the rates market and the dollar,” says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG.

Above: Pound-to-Dollar rate shown at daily intervals.

“Those comments will also need to be quite forceful given today’s announcement will coincide with the release of the updated Summary of Economic Projections. In June, the Fed forecast real GDP to contract by 6.5% in 2020. The Bloomberg consensus is currently at -4.5% while MUFG puts the calendar year GDP growth estimate at -3.6%," Halpenny says.

Many expect the Fed to extend the duration of some existing programmes, which would be a natural opportunity for it to announce other changes are intended to help generate the extra inflation the bank has committed to delivering. This additional support could potentially come in the form of another increase of the pace at which it buys new debt issued by the government and mortgage lenders, if not other commercial firms too.

The Fed is obliged by law to use monetary policy to deliver steady inflation of around 2% and “maximum sustainable employment,” which normally sees it cutting interest rates and using quantitative easing to force bond yields and other borrowing costs for everybody lower in the hope of incentivising greater economic activity that bolsters employment, growth and prices.

All of the new Dollars created by the Fed this year have played an integral role in curtailing a two-year U.S. Dollar rally that turned ugle amid the coronavirus-inspired liquidity crisis of March so if the bank was to surprise markets with an expansion or extension of the above programmes on Wednesday then it might be likely to further undermine the greenback. However, anything less than that might ultimately serve to counter Wednesday's renewed U.S. decline that lifted even the Brexit-battered Pound-to-Dollar rate.

"The Fed needs to show its good intentions in action, and it needs to do so soon in order to safeguard credibility of its proposed shift in policy to flexible average inflation targeting. This may come as soon as [today] If we are right, this should help put USD back on a weak footing," says Mikael Olai Milhøj, a senior analyst at Danske Bank. "The disbelief in the Fed and Brexit has weighed on GBP/USD [but] we look to buy the cross on autumn dips towards 1.27, targeting 1.43."

Above: Pound-to-Dollar rate shown at weekly intervals.