Above: David Bloom of HSBC, image (C) Pound Sterling Live.

- Market may be overly negative on the economy say HSBC

- Unknown impact of quantitative tightening to be key to Dollar's trajectory

- Schroders' Hornby says 0 Fed rate hikes in 2019 unlikely

The “throng” of analysts warning that the U.S. Dollar will weaken in 2019 should be ignored says David Bloom, global head of FX research and strategy at HSBC, because the U.S. currency will outperform its peers in the year ahead.

“The Dollar is still the best of a bad bunch,” says Bloom in an interview with Bloomberg News. “You can say lots of horrible things about the U.S. but you can say even worse things about others, and that puts me in a strong-Dollar camp.”

The bullish call comes against a backdrop in which the Dollar has fallen by an average of 0.7% versus its major rivals over the last month including 2.06% versus Sterling and 3.26% against the Yen.

The decline has coincided with the majority of analysts turning increasing bearish the U.S. unit. The failure of Trump to keep his majority in Congress was the first body blow for USD, whilst economic fears of excess tightening have also dampened spirits.

The lack of a Republican majority in the lower house has led to the current extended standoff over funding for the Mexican border wall and is expected to lead to a similar impasse after March 1 when the U.S. debt-ceiling reaches its extension deadline and Trump will have to go cap in hand back to Congress to ask for a further extension.

Yet political tensions are only a part of the problem. The main depressing factor for the Dollar is the convergence of multiple economic factors which appear to be signalling the start of a downturn in the economic cycle, or if not then that at least a peak.

The massive sell-off in stocks witnessed in Q4, a sudden spike lower in sentiment data at the end of 2018, and the Federal Reserve’s (Fed) sudden U-turn on raising interest rates are further signs the American economy is in slowdown mode.

Of particular importance to the Dollar is the trajectory of interest rates because these determine net capital inflows. Higher interest rates tend to attract and keep greater inflows, the opposite is true for lower.

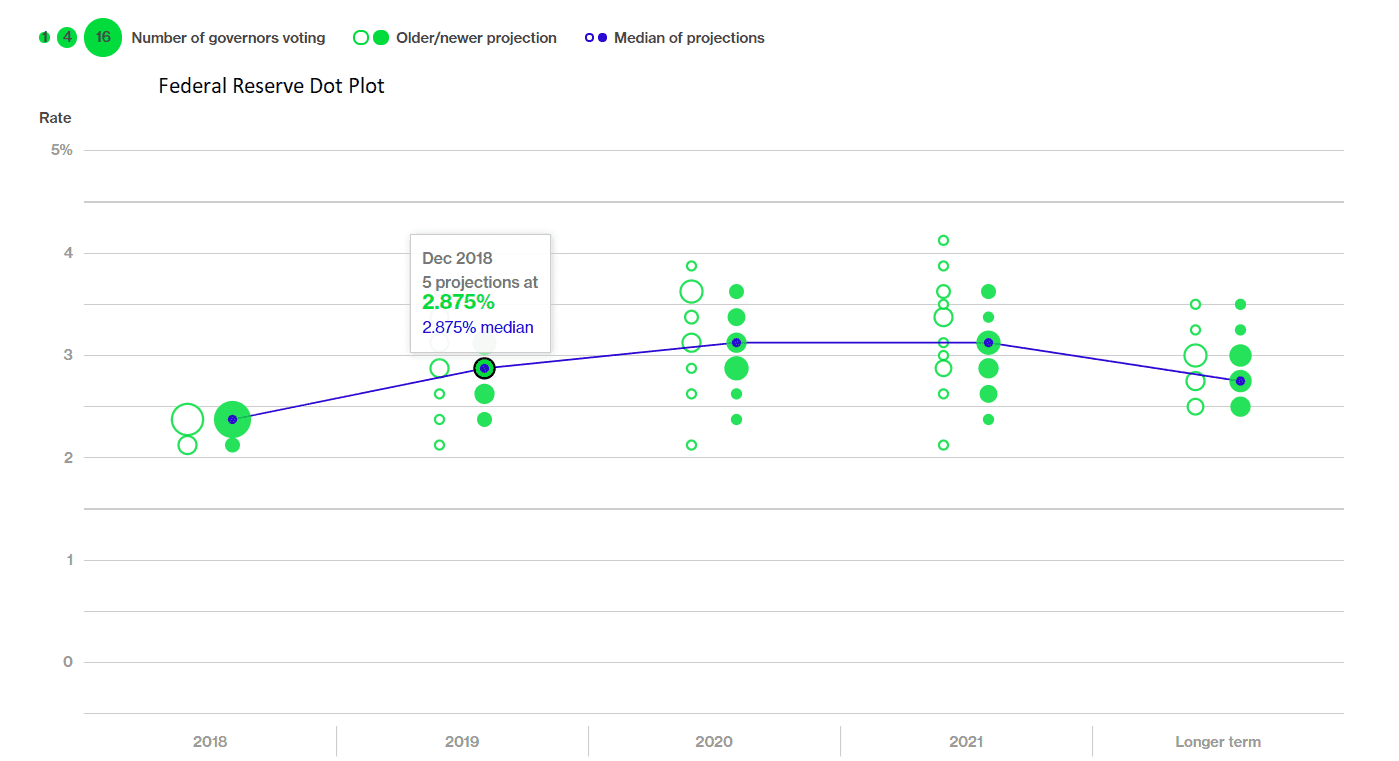

The Fed is ultimately in charge of setting interest rates which currently stand at 2.5%. It has recently reduced its forecast for interest rates in 2019. From previously expecting three to four 0.25% hikes it has now lowered its forecast to expecting only two. This translates into a forecast rate of 2.875% by the end of 2019 - the midpoint of a 3.00% headline figure.

Jerome Powell, the chairman of the Fed, recently said the Fed would “be patient and flexible and wait and see what does evolve, and I think for the meantime we’re waiting and watching.” This was taken as indicating a preference for a ‘wait and see’ approach more commonly associated with a neutral stance, and an aggressively hawkish (in favour of higher rates) position.

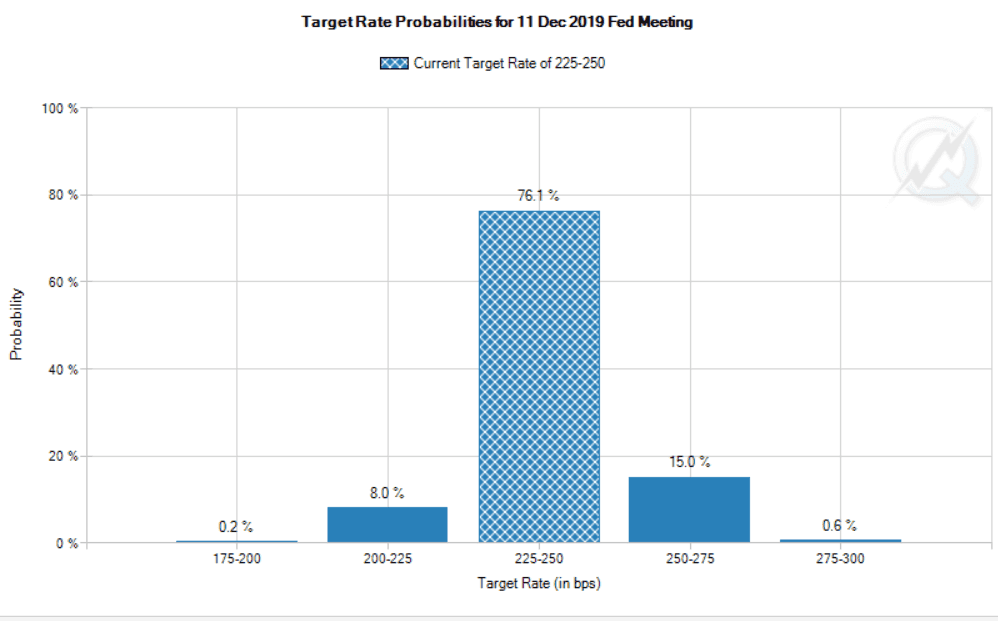

The market, however, is even more dovish (meaning favouring lower interest rates) and now sees as most probable no-change in interest rates in 2019, based on Fed Funds Futures pricing, which is showing 76.1% probability of no-change at the last Fed meeting of the year (Dec 11).

The market view that there are likely to be no rate hikes in 2019 is too extreme, according to some, and the Fed will probably hike even if only once, suggesting the Dollar may hold afloat better than the consensus thinks, and Bloom’s contrarian strong-Dollar call has ‘legs’.

“I think the market has taken that “patience” message and maybe extrapolated it a bit too much because I don’t think the economy warrants zero rate hikes in 2019,” says Lisa Hornby, portfolio manager at Schroders.

Quantitative Overkill

Part of the reason for the market’s sharp re-assessment of Fed rate hike probabilities is due to the combined monetary impact of both the rate hikes it has enacted and simultaneously a programme of ‘quantitative tightening’.

Quantitative tightening is the opposite of the ‘quantitative easing’ the Fed did during the great financial crisis when it stepped in and bought $3-trillion worth of bonds to help support the floundering financial system.

In 2014 the Fed stopped outright purchases and at the start of 2018, it stopped reinvesting the proceeds from maturing holdings, seeing no further risks to the system. As the bonds mature and the original issuers are forced to repay the principal it causes a net run-off of excess liquidity, which acts as a proxy form of tightening much like raising interest rates.

In 2018, therefore, both forms of tightening operated in tandem and some of the more dovish analysts have argued that this magnified the effect of rate hikes and caused substantially more tightening than was planned.

This caused a tightening ‘overkill’ which has led to the soft-Dollar, dovish, backlash, witnessed in markets now.

Tom Atteberry, a senior portfolio manager at First Pacific thinks the Fed chairman’s comments about patience and flexibility belie a lack of knowledge about the real impact of ‘quantitative tightening’ on the economy.

“They have this two factor model they are working on, they seem to be pretty good at figuring out how to raise short term interest rates - the Fed Funds rate - they have got lots of history, lots of experience,” says Atteberry. “They have no idea - I shouldn't say that, yeah I will - they have really no idea, like, what to do with this three trillion worth of assets. How do I get out of the room that I got into?”

Quantitative tightening (QT) could have a greater impact on the market than the Fed expects since it has little experience of withdrawing from such a massive stimulus programme, historically-speaking, unlike interest rates, so there is a risk the effect of QT could be greater-than-expected.

“Given your objective was to impact the markets when you entered into this purchasing programme, so if you are going to exit, you sort of have to figure, you know what, You are probably going to impact it then too,” says Atteberry in an interview with Bloomberg News.

Clearly, if the impact of QT is more acute than estimated, it could father a deeper slowdown in the economy, which would probably be negative for the Dollar.

If, on the other hand, the impact is milder than the Fed expects it could resume raising interest rates, a scenario in which the market would be at risk of being proven wrong, as it was with its soft-Dollar view in early 2018.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. please see here.