BlackRock Wants More U.S. Shares as AI Trade Broadens

- Written by: Sam Coventry

Image © Adobe Images

The world's largest asset manager says it will increase exposure to U.S. equities as the AI trade broadens.

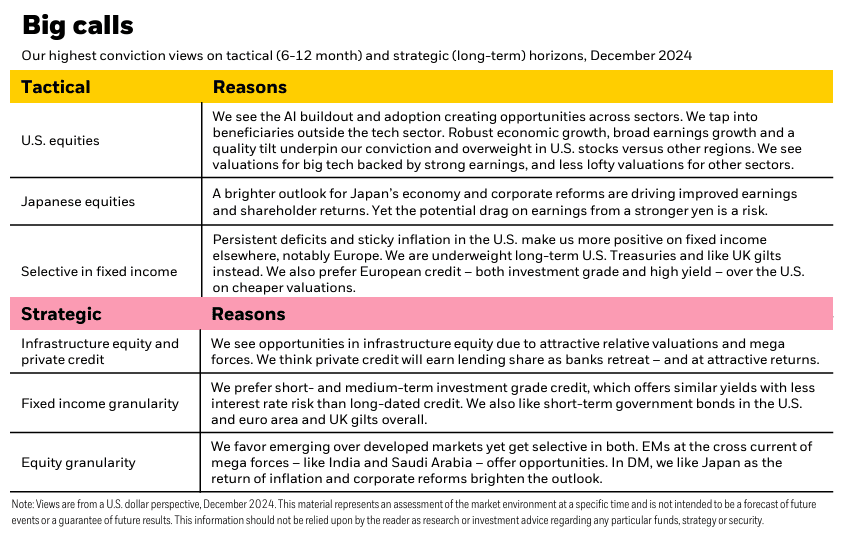

BlackRock is increasing its overweight position in U.S. equities because it believes that the benefits of artificial intelligence (AI) will extend beyond the tech sector.

The AI stock boom of 2023-2024 was centred on stocks that produced the physical components that power AI and tech companies that produced the initial AI engines.

The "magnificent 7" mega-cap tech stocks - Amazon, Apple, Google, Meta, Microsoft, Nvidia, and Tesla - are mentioned as examples of companies that are already benefiting from this trend.

However, BlackRock thinks the number of AI beneficiaries will broaden out, leading to robust economic growth, broad earnings growth, and a quality tilt that supports its conviction in U.S. stocks over other regions.

AI buildout and adoption are creating investment opportunities across various sectors.

Here are more details about BlackRock's allocation strategy:

- BlackRock's outlook for 2025 is "risk-on," meaning they are willing to take on more risk to achieve higher returns.

- BlackRock believes that investors should no longer think in terms of traditional business cycles (with their short-term fluctuations in activity) but should instead focus on mega forces like AI that are driving long-term economic transformation.

- The rise of AI is already being reflected in the markets. For example, the “magnificent 7” mega-cap tech shares, which include companies like Amazon, Apple, and Microsoft, now make up almost a third of the S&P 500’s market capitalisation.

- The company also believes that U.S. equities can continue to outperform global peers because of the U.S.'s ability to better capitalise on these mega forces.

Analysts also cite the favourable U.S. growth outlook, potential tax cuts, and regulatory easing as reasons for their bullishness on U.S. stocks.

BlackRock analysts acknowledge that U.S. equity valuations, based on price-to-earnings ratios and equity risk premiums, are high.

However, they argue that valuations have less of an impact on long-term returns than they do on short-term returns. BlackRock points to the equity risk premium for the equal-weighted S&P 500, which is currently near its long-term average, as evidence that valuations are not overly stretched.

BlackRock is not as optimistic about U.S. government bonds. Analysts are tactically underweight long-term Treasuries because they believe investors will demand more compensation for the risk of holding them due to persistent budget deficits, sticky inflation, and greater bond market volatility.

Instead, BlackRock favours government bonds in other developed markets.