Chancellor Rachel Reeves. Picture by Kirsty O'Connor / Treasury.

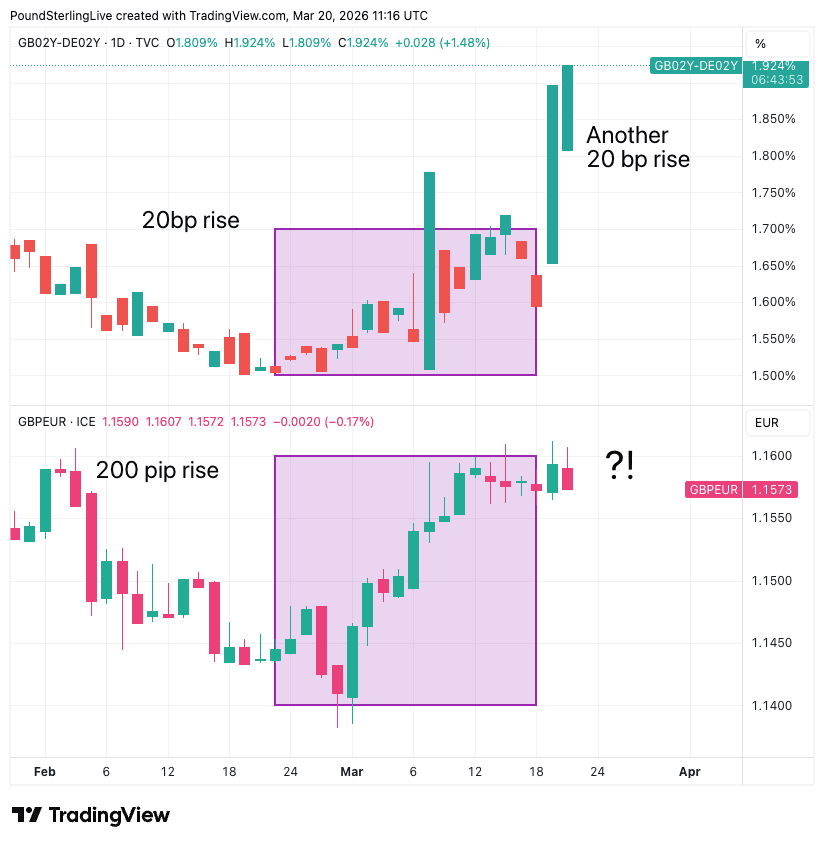

Pound sterling should be much higher against the euro; something is bothering it.

We're watching the pound-euro exchange rate and think the market is sending a concerning signal. It has tried, and tried, to break above €1.16 but is just not getting anywhere; Friday's attempt to advance was rebuffed and now bulls have been forced into retreat, with spot back at 1.1574 at the time of writing.

Yet, underlying bond yields are screaming out loudly that the pair should be much higher: the UK two-year bond yield minus the German equivalent is the benchmark we're watching.

A 20 basis point rise in the spread between March 01 and March 15 propelled GBP/EUR from 1.14 to 1.16.

Since March 15, we've had another 20 basis point rise in that differential, and yet there's nothing to show for it in the GBP/EUR exchange rate. If the transmission mechanism was consistent GBP/EUR should be another 200 pips along, at 1.18!

So, there's a message here for us: interest rates aren't supporting the pair anymore.

The question is why? We think concerns are starting to mount as the market sees these bond yield rises as destabilising for the country's finances.

Bond yields are effectively the interest rates the government has to pay on the debt it issues. The significant climb in recent days means the government must dedicate more and more of its receipts and new borrowing to pay off debt.

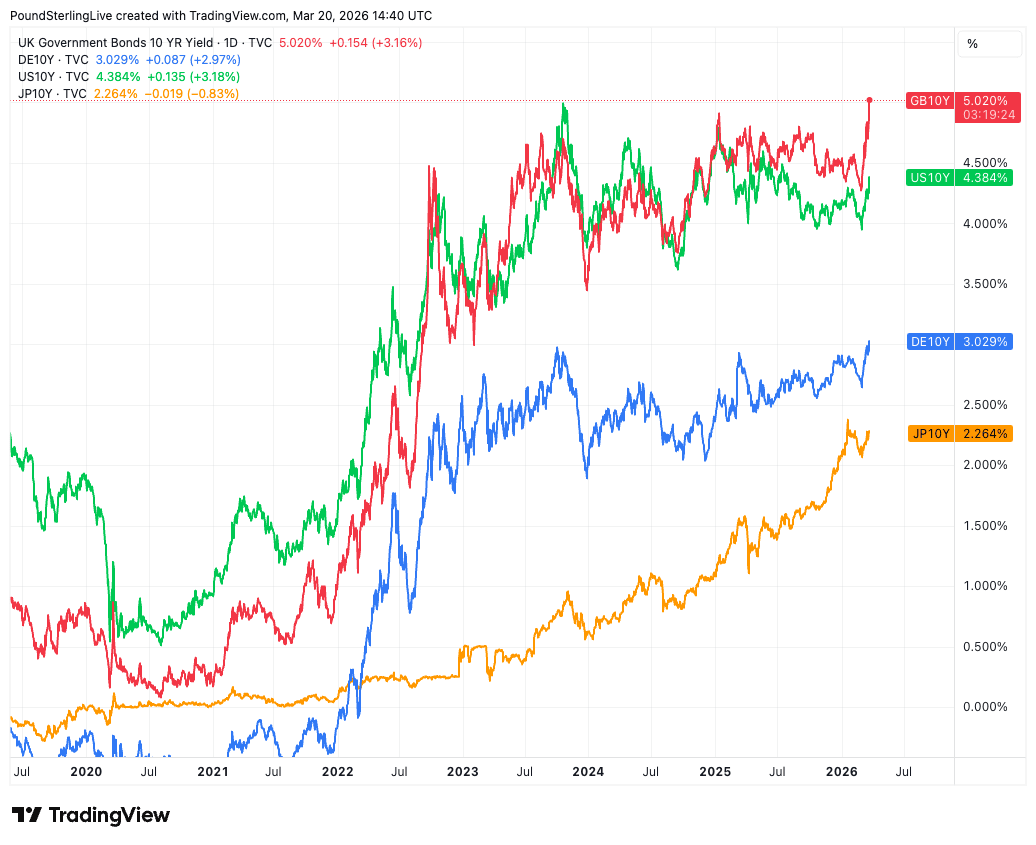

The UK ten-year bond yield trades well above G10 peers and is back to levels last seen during the 2008 crisis. That means the market demands a premium of the UK and thinks it is the most vulnerable country to an emerging inflationary spike.

Above: UK ten-year bond yields trade at a premium to major peers.

The ONS said Friday that government borrowing was at £14.3BN in February versus the £8.8BN that was expected. Debt interest payments have more than doubled from a year ago, rising from £5.5BN to £13BN.

Surging borrowing costs could force the government into uncomfortable trade-offs in the Autumn when it has to deliver a new budget. More taxes are likely, and unfortunately for Chancellor Rachel Reeves, avoiding spending cuts won't be an option this time around.

Simon French, economist at Panmure Liberum, has also been watching developments. He says on Friday, "I am surprised GBP has held up so well."

Economists are watching the surge in short-term borrowing costs this Friday with mounting concern.

To be sure, bond yields are rising everywhere as markets brace for higher central bank interest rates in response to the surge in oil and gas prices of recent weeks. But, the UK's borrowing costs are rising faster than elsewhere, and that's a concern for the currency as it shows a heightened concern for UK bonds and debt dynamics.

The UK is by Developed Market standards a high inflation economy "because it rations energy, land and capital). Inflation has averaged 3%/year since 2010. An energy shock hits UK hardest, so inflation premia on short-dated Gilts quickly emerges."

French says there are five reasons why the UK is being singled out:

1️⃣ The UK is by Developed Market standards a high inflation economy "because it rations energy, land and capital). Inflation has averaged 3%/year since 2010. An energy shock hits UK hardest, so inflation premia on short-dated Gilts quickly emerges."

2️⃣ "UK rate cuts and an inflation slowdown were a consensus trade for Q2 so unwinding that positioning by allocators risks overshooting, particularly with a scarcity of institutional Gilt buyers (one of the legacies of the ongoing DB-DC pensions transition) and ongoing QT."

3️⃣ "An expensive bailout of household and business energy bills would likely result in an unexpected increase in short-dated Gilt issuance, so higher interest rates will be required to clear the market."

4️⃣ "Rayner manoeuvres of recent days brings UK political change (with more issuance, more spending, more friction, institutional uncertainty) back on the table. Pricing that impact (comments about the OBR are classic bogeyman tactics) remains tricky, but qualitatively, it certainly has been noticed"

5️⃣ "BoE appears worried around inflation expectations - that remain elevated, at least in survey-based measures. A hawkish reaction that asserts low tolerance for any “look through” reprices the UK rate path. That kicked off yesterday’s move - but the qualitative MPC comments couldn’t justify, in isolation, the degree of repricing."