Lloyds Commercial Banking have issued their latest FX forecasts, which offer a slither of hope for those out there waiting for a stronger US dollar and pound sterling.

The latest editon of Lloyds' International Financial Outlook is out, and markets get an insight into what economists are predicting for perhaps the most notirously difficult market of all to predict.

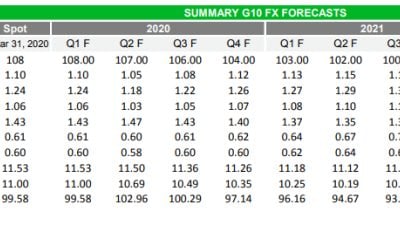

The summary table is below, but first a look at how the key pairs are expected to perform.

The euro to dollar exchange rate is to pull back into the range to 1.12 by the end of the year after flirting with breaking out above the 1.1500 range highs.

This to be as a result of the US Federal Reserve raising interest rates in June, which is expected to support the dollar side of the pair.

The pound to dollar exchange rate is to ‘stabilise’ in a zone between 1.35 and 1.38 which they note is a level unbroken since 1985.

GBP/USD is expected to then rally to 1.47 by year-end, presumably as a result of the referendum vote resulting in the UK remaining within the EU (although Lloyds do not specify this).

The assumption is investors’ expectations about when the Bank of England will raise rates will be brought forward dramatically.

Latest Pound/Euro Exchange Rates

| Live: 1.1601▲ 0%12 Month Best:1.1754 |

*Your Bank's Retail Rate

| 1.1207 - 1.1253 |

**Independent Specialist | 1.1439 - 1.1485 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Currently, markets are pricing a 45% chance the BoE cutting rates before the end of the year, but Lloyds stick to their belief the central bank will actually start raising rates in November.

The pound to euro exchange rate is to “find a floor soon” at the sturdy 1.22 level before moving back up to 1.31 by year end.

Compare this to suggestions at ABN Amro that the pair will find a floor at 1.17 but fall to parity on an 'Out' vote in the EU referendum.

Again presumably - although not stated as such - based on the success of the Bremain camp, but most definitely as a result of a November rate hike by the BOE.

In contrast, Lloyds see no change in policy from the European Central Bank for now, and continued modest growth in line with current trends.

Interest Rates Surprising to the Upside

Lloyds’ expect the Federal Reserve to raise interest rates in June, followed by December. This is more than current market expectations for only one interest rate increase in 2016.

They also hold onto the view that the Bank of England (BOE) will raise interest rates in November, despite current investor expectations based on futures rates that the BOE will now reduce interest rates by 0.25% in 2016 - a complete reversal of the previous bias towards foreseeing rate hikes.

Lloyds see the European Central Bank remaining on hold for now, and modest growth in the euro-zone continuing in line with the trend of about 1.5% per year.

Commodity Currencies Marching Higher

As far as their outlook for other pairs goes, below are summaries of their comments for the commodity group:

AUD/USD is actually expected to rise marginally to 0.78 by the end of the year. This runs contrary to current market expectations that the Aussie will fall as a result of the Fed raising interest rates and commodities falling back down towards their 2015 lows again as their current recovery move runs out of steam.

Lloyds mention that, “it is noteworthy that, despite the appreciation in AUD so far this year, RBA Governor Stevens has chosen to not actively talk down the currency in recent speeches.”

They further mention that: “As long as the global risk environment remains stable, we favour AUD/USD consolidating around current levels, with gradual appreciation toward 0.78 by year-end.”

USD/CAD to retrace higher, going back up to 1.35 as a result of the Fed hiking interest rates in June, but then falling back down to end the year at 1.30 as a result of the price of oil rising steeply up to 55 dollars a barrel.

They expect the Bank of Canada to maintain its current policy stance at April’s meeting, “with Governor Poloz’s likely to maintain an optimistic tone”.

NZD/USD to weaken as a result of the Fed surprising with an interest rate rise in June, but to then track higher again based on New Zealand’s strong underlying fundamentals (despite notable weak spots such as the dairy industry), and assuming stable inflation, to return to the 0.68’s by the end of the year.