The stand-out call in Standard Chartered's 2016 exchange rate forecasts is the end of the US dollar bull-run. However, the USD will advance against a select number of currencies, of which the euro is included.

Predictions of a softer 2016 for the US dollar come just as we see the currency turn notably lower on the back of softer-than-expected US economic activity.

The selling comes as memories of how well the dollar fared in 2015 remain fresh in our minds; the USD rallied strongly against both G10 and Emerging Market currencies as the Euro area, Japan, China and a number of other Asian countries initiated or expanded monetary stimulus, intensifying monetary policy divergence.

However, in their latest global exchange rate forecast note Standard Chartered caution that the US dollar will likely see its strength fade in 2016. This view is shared by fellow forecasters at HSBC.

Standard Chartered believe broad USD strength is likely to end for two reasons.

“First, a modest Fed rate hike scenario for 2016 is already priced-in. The Fed is also likely to become

more sensitive to USD strength, in our view, this may limit rate hikes should the USD continue to rally strongly,” says Tariq Ali at Standard Chartered.

Second, Ali believes the likelihood of further policy easing in many G10 countries is diminishing, and those that do ease further face the risk of a diminishing impact given how low yields already are.

Latest Pound/Euro Exchange Rates

| Live: 1.1601▲ 0%12 Month Best:1.1754 |

*Your Bank's Retail Rate

| 1.1207 - 1.1253 |

**Independent Specialist | 1.1439 - 1.1485 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

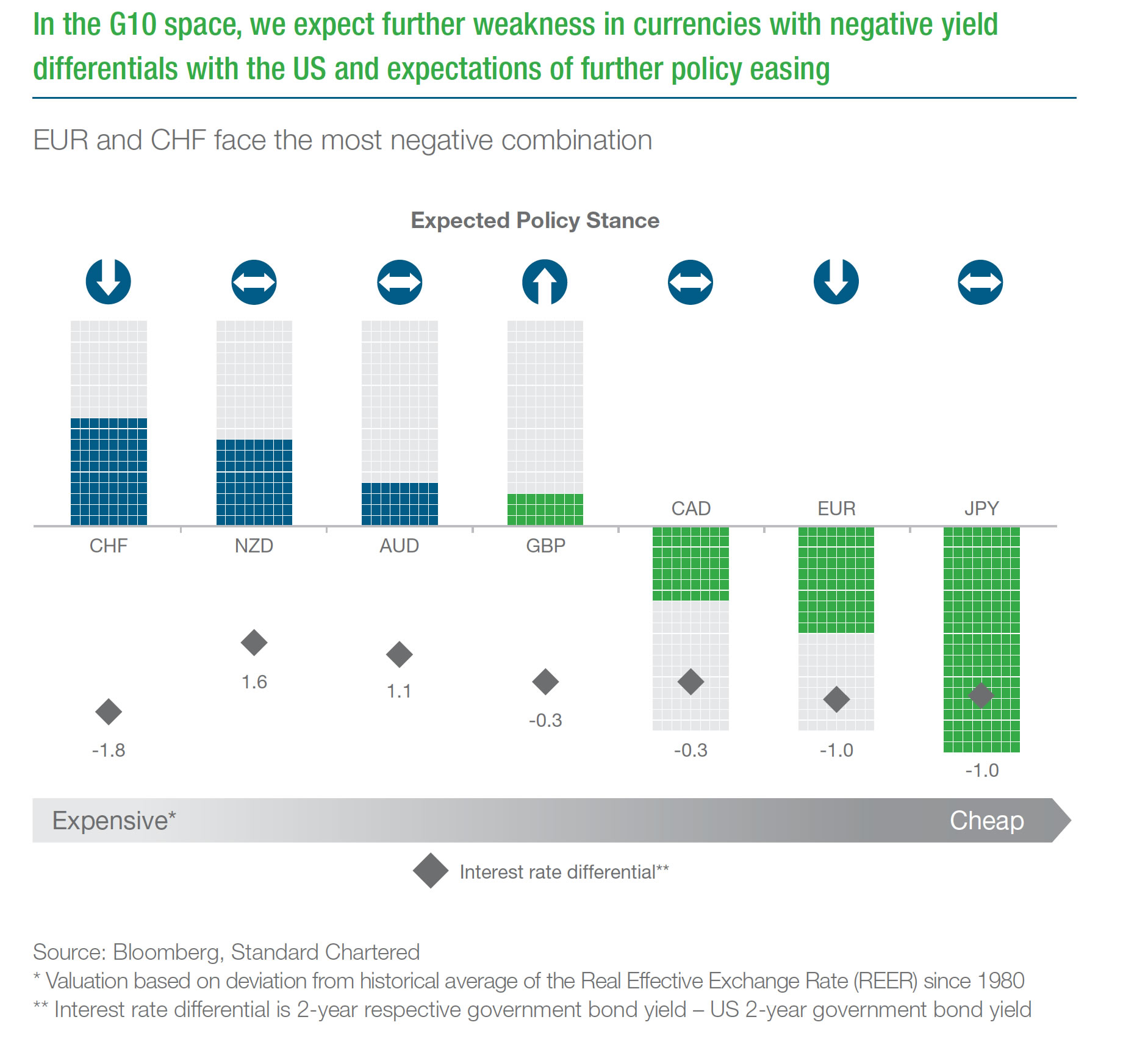

But, a case for selective USD outperformance remains in place though.

“We still see room for USD strength via continued monetary policy divergence against the EUR and CHF. In both cases, we believe authorities are likely to undertake further policy easing

measures,” says Ali.

Consequently, Euro area yields are likely to fall further into negative territory, expanding interest rate differentials with the US, and ultimately driving the EUR and CHF lower.

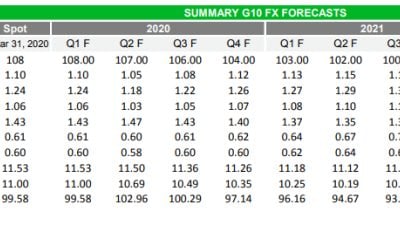

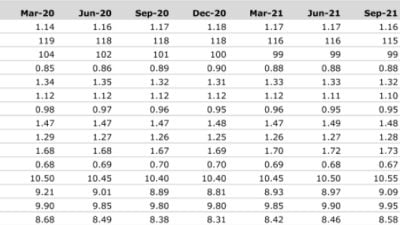

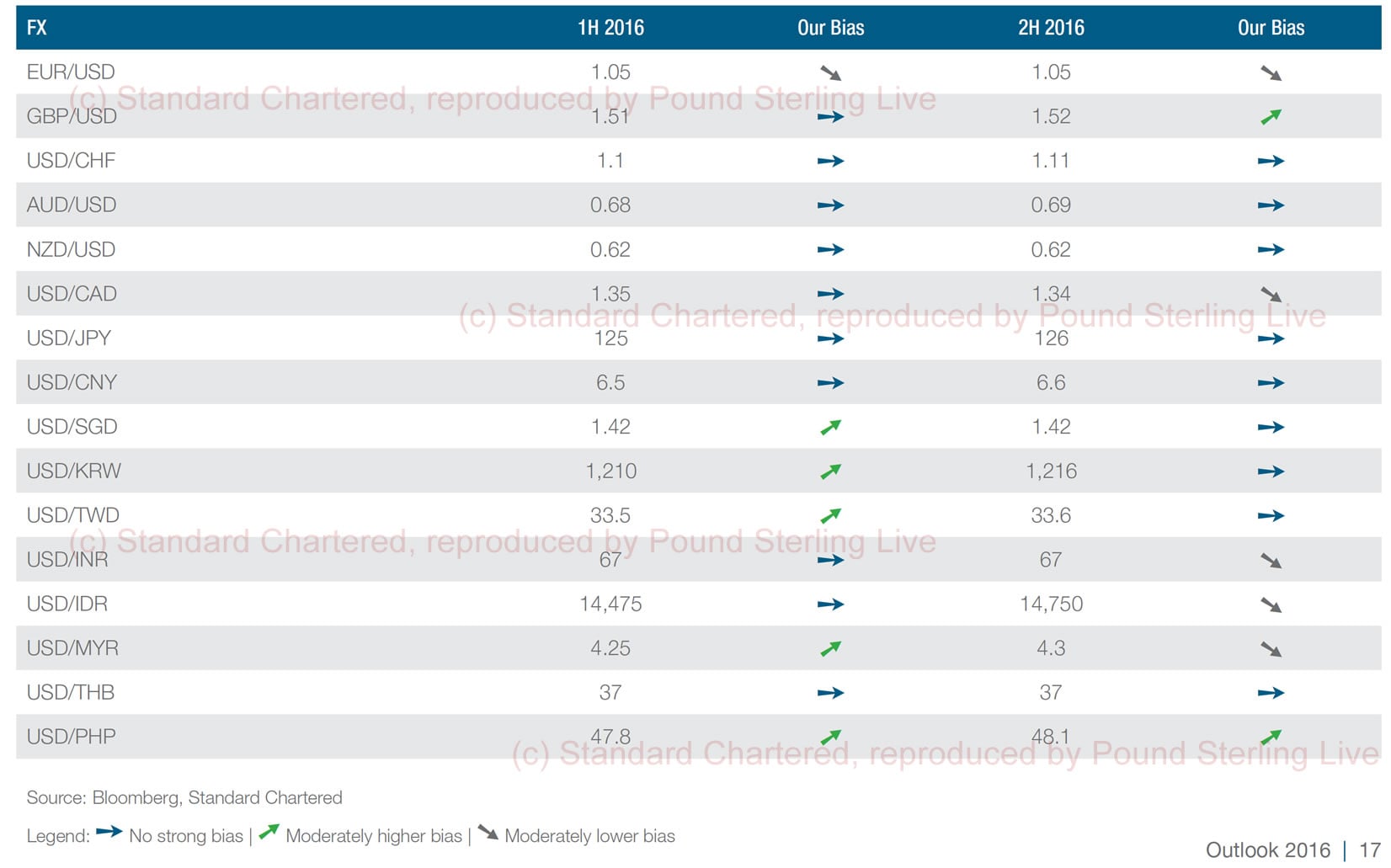

It is worth noting that the declines expected in the EUR/USD exchange rate are mild when compared to those who were forecasting parity and lower to be achieved. Standard Chartered see the rate hitting 1.05 in mid-year.

“We also see further room for USD strength against the AUD and NZD, where our negative outlook on their respective key export commodities argues for more weakness ahead,” says Ali.

The pound to dollar exchange rate is meanwhile forecast to move back above 1.50 in the first half of 2016 before seeing 1.52 in the second half of the year.

Commodities: Oil Prices to Recover

Turning to the commodity sector analysts at Standard Chartered confirm they remain negative on commodities, but say the pace of weakness likely to slow compared with 2015.

“We believe commodities are likely to underperform other major asset classes heading into 2016. 2015 was characterised by sharp weakness in prices accompanied by a rise in inventories, almost across the board,” says Standard Chartered’s Manpreet Gill.

A narrowing demand supply-gap is likely to slow the pace of losses given the magnitude of decline thus far.

“We also see room for greater divergence, with oil potentially facing the greatest upside risks and industrial metals facing continued downside risks,” says Gill.

Oil prices may rise by the end of 2016 as the demand/supply gap gradually closes through the year.

However, Standard Chartered do not expect oil prices (Brent) to exceed a quarterly average of USD65/bbl while risks of further downside remain heightened in the short term.