The Euro to US Dollar is in a strong uptrend which has reached a major trendline connecting the October 2016 and January 2017 highs.

The expectation would normally be for the exchange rate to pull-back from a trendline of such importance, however, price action has not shown any significant weakness and although it has stalled since touching the trendline, there is no sign of weakness yet, as such.

In the absence of bearish price action, we would expect the intact uptrend to extend higher, breaking above the trendline and moving into new territory beyond.

The R1 monthly pivot is not far above the trendline at 1.1540 and presents bot an initial target and an obstacle to the uptrend, however, one breached the pair should then move up to the 1.1650 level and possibly even higher longer-term.

Momentum, measured by MACD, is slowing somewhat and diverging with price action, however, this alone is not sufficient to indicate a change in the trend.

Data for the Euro

The main event for the Euro in the week ahead is the European Central Bank (ECB) rate meeting on Thursday at 12.45 BST.

No actual policy changes are expected at the meeting, ie changes to interest rates or the QE programme.

There is a possibility, however, that the ECB may tweak the language in their accompanying statement which provides guidance.

They may well remove the phrase that they will ‘increase the pace of QE’, or asset purchases as they are also known, should conditions require it, as suggested in a recent note by Nomura bank, for example.

A variation on this idea has also been suggested by Canadian investment bank TD securities:

“We expect policy to be left unchanged, but the ECB is likely to tweak the language, indicating that QE can now only be increased in duration, but not size.”

According to Nomura, however, this expectation sets up the risk that if the ECB do not change the language of the statement the Euro will fall, as it has already reached relatively overstretched levels.

An important data release in the run up to the rate meeting is inflation data on Monday, which is forecast to show a 1.3% rise in June – the same as the previous month – on a year-on-year basis, ie compared to June 2016.

Any slowdown in inflation, incidentally, will weaken the Euro as it will make the ECB more reluctant to unwind stimulus.

The other major release in the week ahead is the ZEW economic sentiment survey, out at 10.00 BST on Tuesday, July 16.

The ZEW is based on interviews with 350 economists and analysts and assess their views on the economy and the medium-term outlook, e.g the next 6-months. It is considered an accurate leading indicator for the Eurozone economy.

Data for the Dollar

Politics may be a significant driver for the Dollar in the week ahead.

A new health care bill proposed by Republicans to replace Medicare could be voted on as soon as next week.

The problem is that a number of Republican senators have expressed reservations about the bill which they think is too tough and will result in millions of Americans losing free access to healthcare, so its passage is likely to be fraught with complications.

Trump has made it clear that the expected tax reforms cannot be implemented until the bill has been passed and savings have been made on healthcare.

Tax reforms – or rather cuts – were one plank of Trump’s promised fiscal stimulus reforms which so supported the Dollar previously.

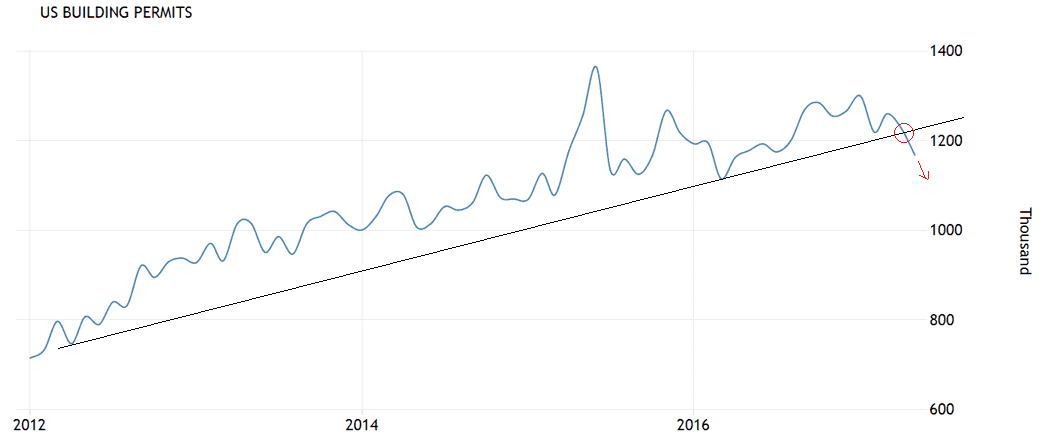

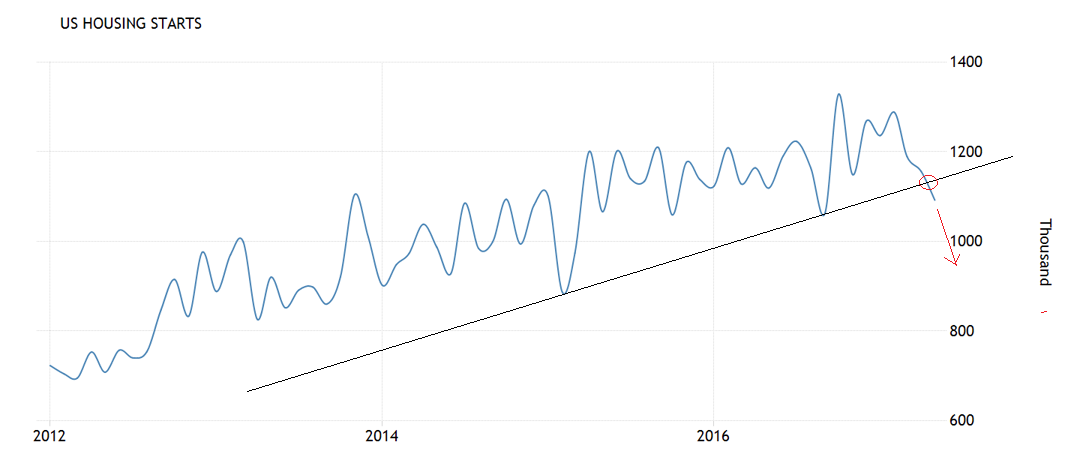

Housing in Decline

On the hard data front, housing, comes front and centre in the week ahead.

Housing is key because it is often said to ‘lead the economy’, thus it can be an early warning of either a slowdown or growth.

Both Housing Starts and Building Permits data (June) are released at 13.30 BST on Wednesday, July 19.

Markets are expecting housing stats to bounce back after declining substantially last month, however, looking at the historical charts of the two releases we are sceptical.

Both show the data sets starting to decline and reverse their uptrends.

Both also show breaks below key trendlines for the data which are extremely bearish indicators for future results.

Given Housing leads the economy, a decline is not a positive forward indicator for US growth.