Image © Adobe Images

Year-end effect comes early, and the euro stands to be amongst the biggest losers.

The euro is now the focal point of year-end reversion risks in FX markets, both technically and positioning-wise.

This is the finding of a new research report from Royal Bank of Canada's Capital Markets division, that finds the euro risks losing value as a defensive unwind takes hold.

"Positioning unwinding is our main theme as the Year-End effect comes early," the bank writes in its latest FX Market Beta update. The clearest trade to express that shift, RBC says, is short EUR/JPY, the strongest directional view for the fourth quarter.

In valuation terms, EUR/JPY trades about 6% above its 200-day moving average, making it one of the few G10 crosses RBC sees as over-extended.

The bank has closed its short NZD/JPY and shifted to short EUR/JPY, arguing that the cross is unlikely to rally further given the emerging risk-off tone.

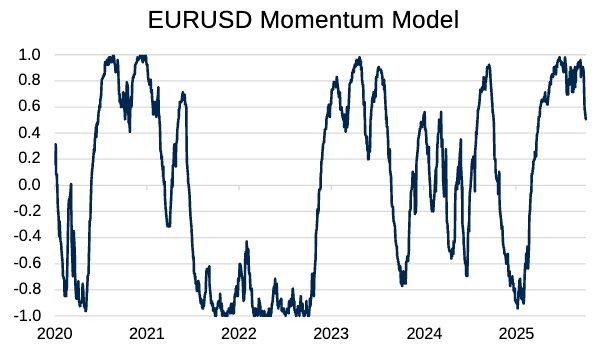

Momentum models across the G10 complex have turned sharply lower, marking what RBC calls the "first major shift since April."

The biggest reversals are showing up in EUR, GBP, CAD, NZD, and JPY, where speculative long positions are now under pressure.

Commodity trading advisors (CTAs) are meanwhile estimated to hold roughly $17BN in long EUR/USD positions, much of it built between 1.13 and 1.10, leaving them vulnerable to forced liquidation if spot returns to that range.

"Most of these contracts were built between spot 1.13-1.10, implying downside convexity if we trade into this range. Two triggers cause CTAs to close or reduce positions, momentum reversals and higher volatility. FX markets are capturing both," says the report.

Positioning is also a headwinds: for the first time in six months, long EUR is no longer the dominant position against the dollar, it’s been replaced by long AUD and SEK, while USD net-longs are now the largest since March.

Shorts in JPY and KRW remain near record levels, suggesting crowded exposure against the yen even as volatility builds.

The shift comes amid a wave of negative economic surprises that has followed the U.S.–China tariff escalation.

RBC notes that most global surprise indices have turned negative, signalling broad disappointment across developed and emerging markets.

With the U.S. government shutdown ongoing and trade deadlines looming on November 1 and 10, the bank sees “defensive positioning” as the rational stance for the weeks ahead.

Volatility has already started to move, particularly in AUD/USD, USD/JPY, and EUR/JPY, where three-month implied volatility is at its highest since June.

Even so, RBC says volatility is "still far from elevated," leaving room for further spikes if the trade dispute deepens.

The AUD/USD skew is the most bearish since April, showing investors rushing to buy downside protection, while risk reversals in USD/JPY and EUR/JPY stand out as “rich.”

Further out, RBC’s forecasts show a softer dollar profile through 2026, with EUR/USD expected to climb to 1.24, GBP/USD to 1.43, and USD/JPY to 130 as U.S. policy normalises and global growth stabilises.