✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

Image © European Commission Audiovisual Services

Diverging Views on Euro-Dollar: Donnelly Sees Year-End Bounce, ABN AMRO Calls Further Fall.

Two influential voices in foreign exchange are reading the year-end euro-dollar setup in opposite ways.

ABN AMRO is calling for the euro to lose ground against the dollar into year-end, as the U.S. currency's recent bounce has more room to run before its longer-term decline resumes.

In its latest FX Weekly, the Dutch bank says the dollar’s rebound from its mid-September lows is not a random blip.

"We expect the dollar recovery versus the euro toward the end of the year," says senior FX strategist Georgette Boele.

However, she adds that the broader bearish trend in the greenback will likely reassert itself only later in 2026.

The call comes amidst a near-term shift from months of dollar pessimism: ABN AMRO points out that despite constant negative headlines about US politics and policy, the dollar has held up surprisingly well.

"There has been an excess of negative news about the U.S., but its influence on the dollar seems to be fading," says Boele.

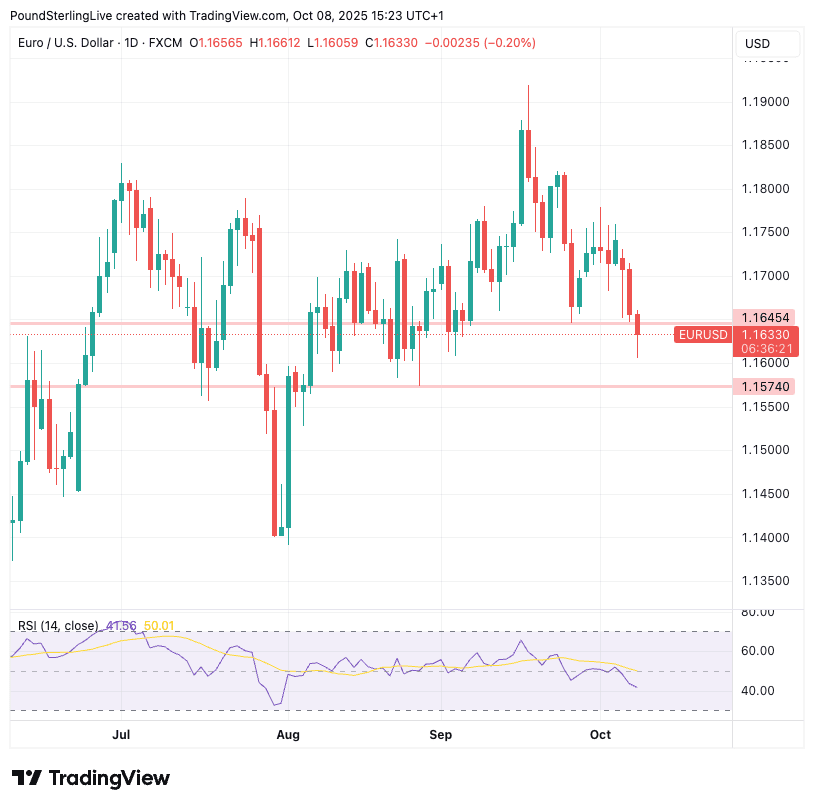

Above: EUR/USD at daily intervals showing a building downside momentum that could target 1.1574 next.

Part of that resilience, she says, comes from America’s leadership in artificial intelligence and digital assets, sectors that continue to attract global investment inflows.

U.S. equities remain strong, and foreign investors have been net buyers even as they hedge their exposure more actively.

Speculative positioning is another factor: traders already hold sizeable net-long euro positions and modest dollar shorts, leaving little appetite to push those trades further.

"There is hesitation to expand these positions," says Boele, noting that technical signals now point to consolidation rather than a continuation of dollar weakness.

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

ABN AMRO also highlights that other regions face their own credibility problems: fiscal strains in the UK and France, political instability in Paris, and uncertainty over Japan’s new government are dampening demand for those currencies.

In short, while the U.S. has its flaws, “there are significant issues elsewhere as well,” Boele says.

For EUR/USD, the bank forecasts a dip from 1.1625 to 1.15 by the end of Q4 2025, before the pair gradually climbs again through 2026 toward 1.25.

The team frames this as a “temporary countertrend” within a still-intact long-term dollar downtrend.

ABN AMRO’s longer-term dollar view remains bearish, citing an overvalued greenback, unsustainable fiscal deficits, and what it calls "aggressive tariff policies, wavering military support for allies, and threats to the independence of the Federal Reserve.”

Those factors, Boele argues, will weigh on the dollar over the next 12 to 18 months.

Taking the other side of a bet against euro-dollar into year-end is Brent Donnelly at Spectra Markets.

He acknowledges that the broader dollar can continue to recover, but that euro-dollar could stand apart from other dollar-based pairs and rise.

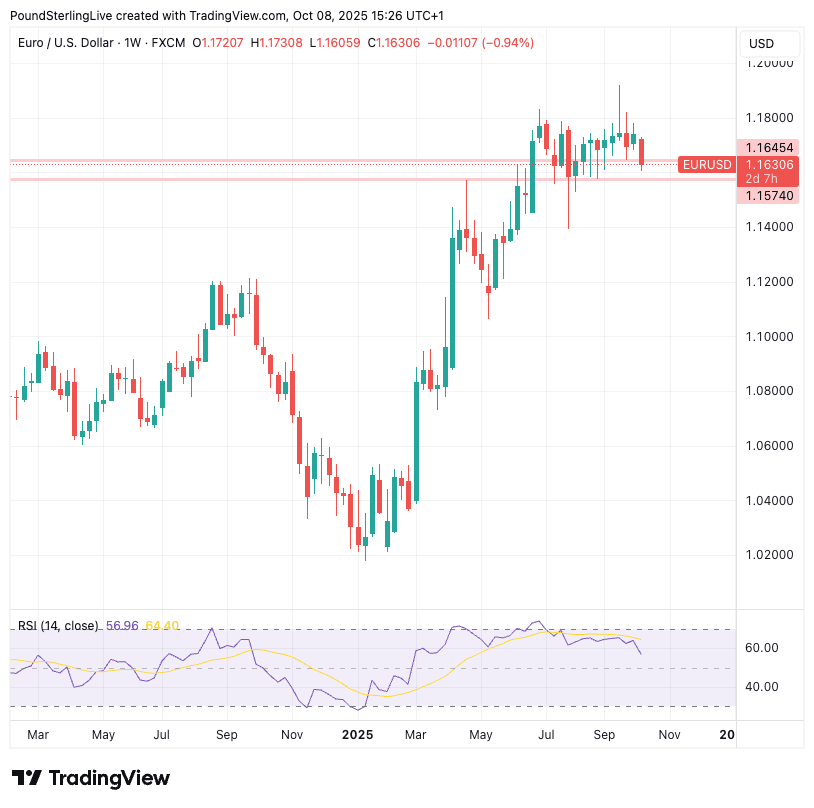

Above: Zooming out to the weekly chart shows the bigger trend remains higher, and current weakness is potentially a consolidation on a multi-month timeframe.

"I believe that the EUR/USD year-end seasonal could still work," he says in a regular FX note, "because there is room for European pension funds to do another round of hedging and central banks are much more likely to buy euros into year-end, not sell."

He explains that seasonal bets aren't working very well in 2025, but that the euro is one of the few places where the old year-end patterns still make sense.

In past cycles, December has often brought waves of euro buying as European asset managers and reserve managers rebalance exposures.

Even though seasonality has "not worked at all this year," Donnelly argues that EUR/USD is the exception, a corner of the FX world where structural flows can still overpower fading global correlations.

His reasoning rests on what he calls "room for central banks to buy euros."

He also cites European pension funds, who, after a strong year for equity markets, may again increase their currency hedges, a move that typically involves buying euros and selling dollars.

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.