✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

Image © Adobe Images

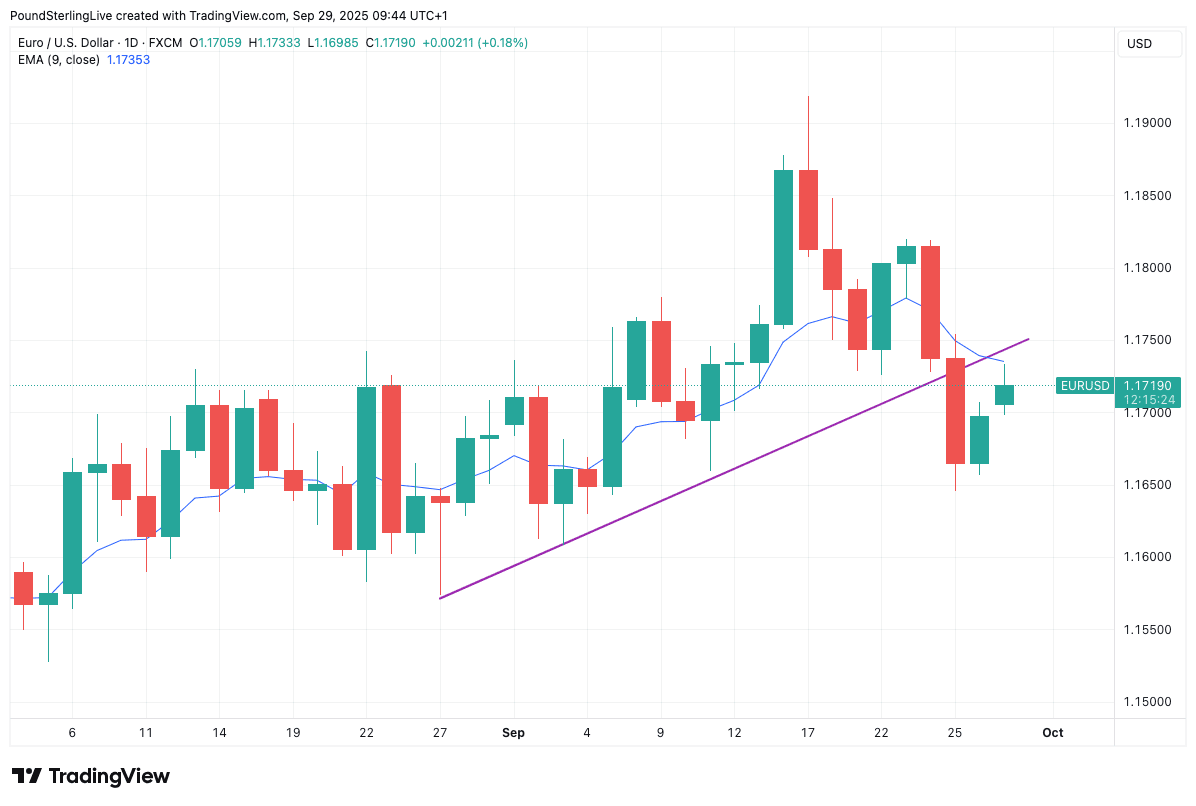

The euro uptrend is certainly looking a little more vulnerable at this point in the cycle.

The dollar starts the new week on a softer footing, letting the likes of the pound and euro catch a breather and recover recently lost value.

However, this reprieve comes ahead of some important U.S. data releases, namely two ISM PMI surveys and the all-important non-farm payrolls job report on Friday; any above-consensus readings here will turbo-charge the Greenback's recovery.

For the euro to dollar exchange rate (EUR/USD) pre-data relief takes the form of a bounce from Thursday's low at 1.1650 to 1.1718 on Monday.

The market is now back at the nine-day exponential moving average (EMA), but while below here, we would anticipate ongoing weakness.

In short, we look for periods of euro strength to be relatively short-lived, with gains ultimately drawing sellers in and delivering new multi-week lows.

A look at the daily chart shows how the euro-dollar outlook as turned down a gear: last week's selloff broke through a rising trendline, which signals an end to the September rally.

Last week, U.S. Treasury yields rose as investors responded to a mix of strong U.S. economic data and slightly 'hawkish' signals from the Federal Reserve, leading to gains for the dollar and new multi-day lows for the EUR/USD.

"A more hawkish-than-expected September FOMC meeting, initial month-end flows and better US data last week drove EUR/$ well inside the 1.14-1.18 range that has held since May," says Themistoklis Fiotakis, an analyst at Barclays.

U.S. second-quarter GDP was upgraded to 3.8% annualised, marking the fastest pace of growth in nearly two years.

Such a clip of growth doesn't exactly scream of a need for the Federal Reserve to lower interest rates, which draws a massive question mark over the market's prior expectation that the Fed will cut rates at every meeting this year.

As the tide goes out on maximum Fed rate cut bets, so the dollar rises.

"Fed Chair Powell pushed back against expectations for aggressive rate cuts, emphasising the need to remain vigilant on inflation risks, while acknowledging the recent slowdown in jobs growth," says a note from Lloyds Bank.

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

In the U.S. this week, the theme of U.S. economic resilience and the debate about Fed rate cuts will continue, with ISM PMI survey data due for release (Wednesday: manufacturing ISM, Friday: services ISM).

These surveys will give a good snapshot of activity in September, and all indications point to a set of robust figures that can further bolster the dollar.

Analysts are nevertheless wary that labour market data will disappoint, underpinning a picture of an economy that is shedding jobs, even if top-line activity is good.

Non-farm payrolls are the week's highlight in this regard, with the market looking for another downshift in job creation.

The expectation is for just 39K jobs to have been created.

For the dollar, any above-consensus outcomes will provide a boost and further pressure EUR/USD.

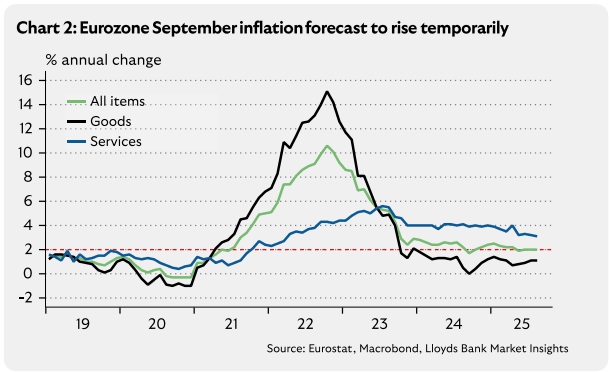

Important data out of the Eurozone this week comes in the form of national and official Eurostat inflation data for September.

Already on Monday, Spain's inflation numbers undershot expectations, with headline CPI coming in at -0.4% m/m, which is below expectations for -0.2%. The annual figure stood at 2.9%, which was up on August's 2.7% but below the 3.0% expected.

Spain is quite important as it has a relatively fast pass-through rate of inflationary prices, meaning it can serve as a barometer of where the rest of the Eurozone will end up in the next couple of months.

The headline, then, is that inflation is still above the European Central Bank's 2.0% target, but the undershoot could point to a below-consensus reading in the all-Eurozone flash estimate, due Wednesday.

If so, then the euro could trade on the soft side.

Eurozone headline inflation is expected to rise to 2.3% from 2.0% in August, driven by petrol base effects. Core inflation is expected to rise to 2.4%.

Such an outcome gives the European Central Bank (ECB) to retain a cautious approach to interest rates, underpinning market expectations that it has finished the rate cutting cycle.

The ECB's committment to holding interest rates contrasts with the Federal Reserve which cut interest rates earlier this month and is likely to do so again in the coming months.

This divergent policy path can help the euro retain support against the dollar, even if near-term trends show the dollar is prone to appreciation.