- EUR/USD seen bottoming in Q4 2021, edging higher in 2022

- As USD eases amid market reappraisal of Fed policy outlook

- Transatlantic growth differential seen turning in EUR’s favour

- EZ, U.S. inflation dynamics seen boosting EUR’s yield appeal

Image © Adobe Images

The Euro has been one of the bigger fallers in 2021 when major currencies are measured by their performance against the Dollar although the latest Barclays forecasts suggest Europe’s unified unit could find itself on the road to recovery in 2022 as the greenback retreats steadily from this year’s highs.

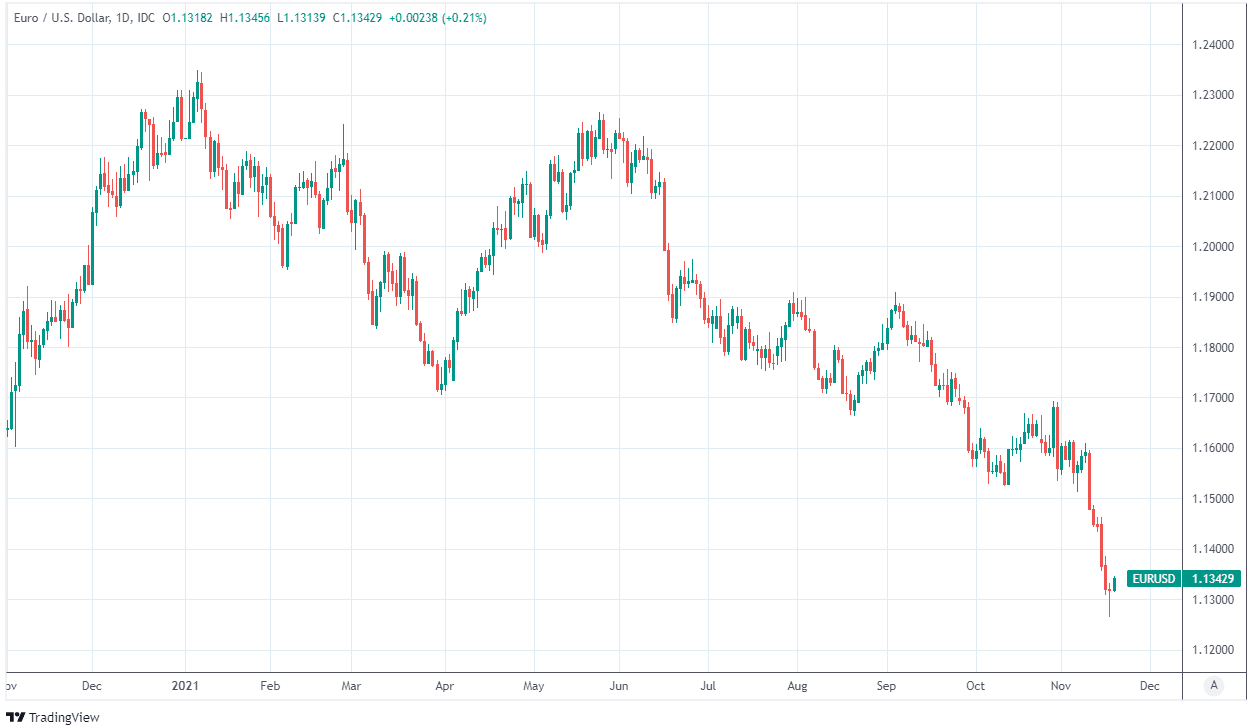

Europe’s single currency came into 2021 comfortably above the 1.20 level and with the wind in its sails but it wasn’t long before the greenback began to find its feet and forced the Euro-Dollar exchange rate into what was an 11-month retreat on Thursday.

The Euro to Dollar exchange rate was down more than seven percent for the year when trading a fraction above the 1.13 handle in the penultimate session of the week after sustaining a punishing run of losses that pulled it from above 1.16 at the beginning of November to its 2021 low near 1.1250 on Wednesday.

The latest forecasts from Barclays suggest that this could have been the single currency’s nadir however, and that the Euro-Dollar exchange rate could be in with a shot at recovering back to 1.15 by year-end ahead of a further gradual recovery throughout 2022.

“While deviations from market expectations of the EU-US real rate differential have occurred, they have been short-lived with EURUSD correcting in line with real rate expectations. We expect this to continue to be the dominant driver of EURUSD,” says Eimear Daly, a strategist at Barclays.

Above: Euro-Dollar rate shown at daily intervals.

- Reference rates at publication:

EUR to USD: 1.1345 - High street bank rates (indicative): 1.0948

- Payment specialist rates (indicative: 1.1288

- Find out about specialist rates, here

- Or, set up an exchange rate alert, here

“Our forecasts for euro area inflation to peak in Q4 21 and quickly fall back below target by end-2022 means the shift in real rates will be in the EUR’s favour in the year ahead,” Daly wrote in a presentation to clients of Barclays’ views on the year ahead outlook.

Barclays was one of the few major banks out there whose forecasts envisaged the Euro’s stellar 2020 recovery against the Dollar going into reverse over the course of 2021, having tipped the Euro-Dollar to end the year at 1.14 for much of it before upgrading that forecast as the year unfolded.

The bank now sees the single currency recovering back to 1.19 before the curtain closes in 2022 and has cited a range of Euro and Dollar centric factors for the forecast including a possible market reappraisal of the Federal Reserve (Fed) outlook and improved optics around economic growth and inflation.

“We expect modest USD depreciation over the coming year, reflecting our views of a positive backdrop for risk and commodities alongside moderate USD overvaluation. Upside risks are largely from risk-off moves rather than US outperformance and are limited relative to downside risks stemming from aggressive market pricing for tighter Fed policy,” says Aroop Chatterjee, Barclays’ U.S. head of FX and emerging market strategy.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Barclays has warned there are risks to its view on the Euro including the possibility that demand for the Dollar could be boosted by a slowdown in China’s economy, possible continued disruption to the supply chains of multinational companies and elevated energy prices, which could weigh on global economic growth and support investor demand for the greenback.

However, the bank says it’s more likely that the Federal Reserve will be slower to begin lifting its interest rate than investors expect and that developments relating to economic growth and inflation will turn in Europe’s favour, likely lifting the Euro-Dollar rate through a positive impact on the EU-US interest rate differential when it’s measured in real or inflation adjusted terms.

“Our base case is for US CPI to peak at a higher level and remain elevated throughout 2022. This should undercut US real rates given our base case assumption that the Fed will not hike rates until Q2 23,” Barclays Eimear Daly says.

“The risks around the French presidential election are now well priced. We rule out it impacting EURUSD bar some intraday volatility into the event. The fiscal impulse from Next Generation EU funds also support our bullish EURUSD view as a fiscal drag sets in the US,” Daly also said.

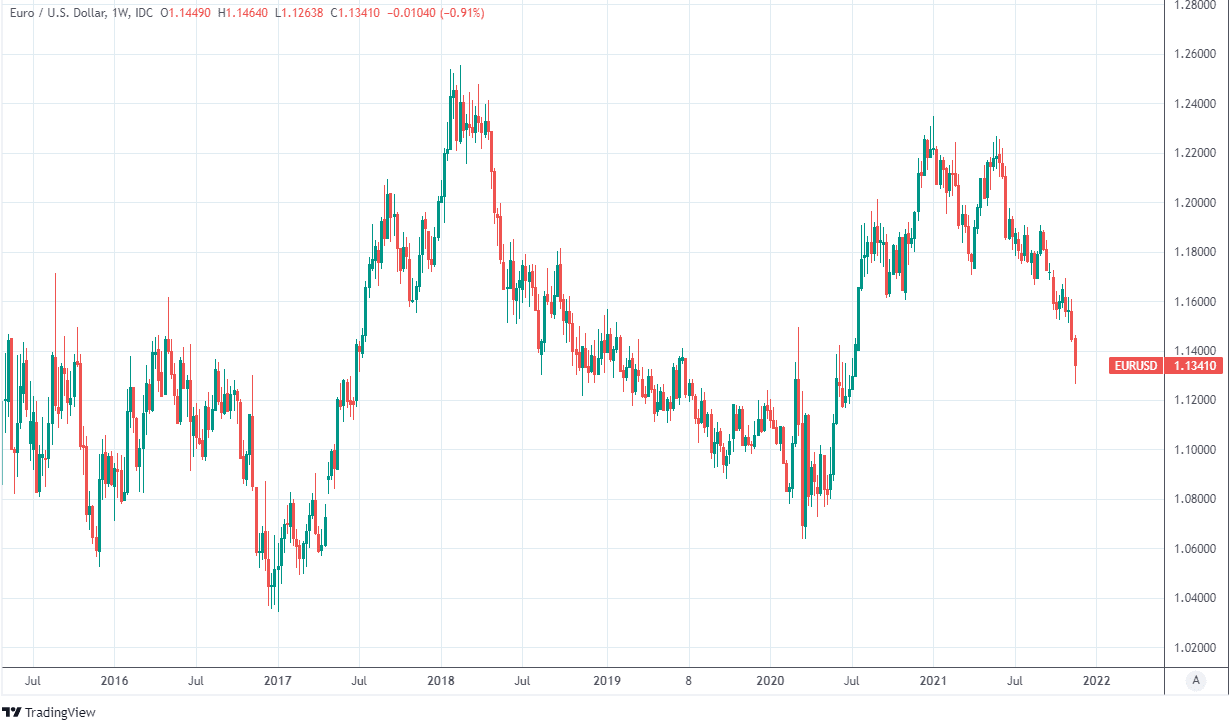

Above: Euro-Dollar rate shown at weekly intervals.