© European Union, reproduced under CC licensing

- Days numbered for expansive monetary policy

- Lower liquidity expectations supporting Euro

- Dollar has more scope to fall from Fed stimulus

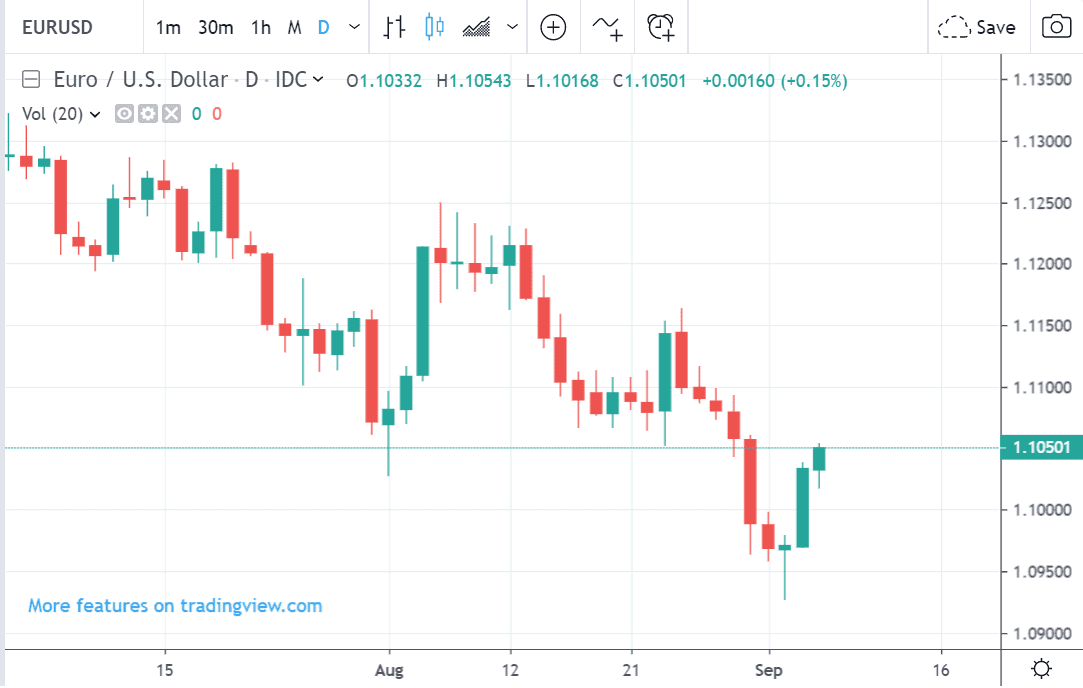

The Euro is rebounding against the U.S. Dollar, helped in part by a growing view that the European Central Bank (ECB) might prove less ambitous than markets were expecting when they announce additional monetary stimulus at their September meeting.

Members of the ECB board - who determine monetary policy measures - could be finding that the ECB has run out of ammunition to further boost inflation and economic growth, thereby rendering any new decisions to ultimately prove pointless.

In fact, there are increasing suggestions that the ECB's policy stance now risks doing more harm than good. And should the ECB show restraint as a result, the Euro could find itself going yet higher.

“They’re running out of firepower, basically,” said Panicos Demetriades, a former ECB governing council member and now professor of financial economics at the University of Leicester.

Reflecting on ECB President Mario Draghi’s now infamous promise to "do whatever it takes" to save the Eurozone economy, Demetriades says, “doing whatever it takes - even if you want to - is becoming harder.”

The ECB would normally be expected to use expansive monetary policies to help the economy out of its current rut, like cutting interest rates or quantitative easing (QE) - both of which would have a negative impact on the Euro.

Lowering interest rates would normally be expected to weigh on a currency by reducing foreign capital inflows which tend to prefer higher yielding jurisdictions. QE weakens a currency because it increases liquidity and also lowers rates.

But this time round experts say the ECB does not have the same scope to ease, which may help partly explain why the Euro is recovering.

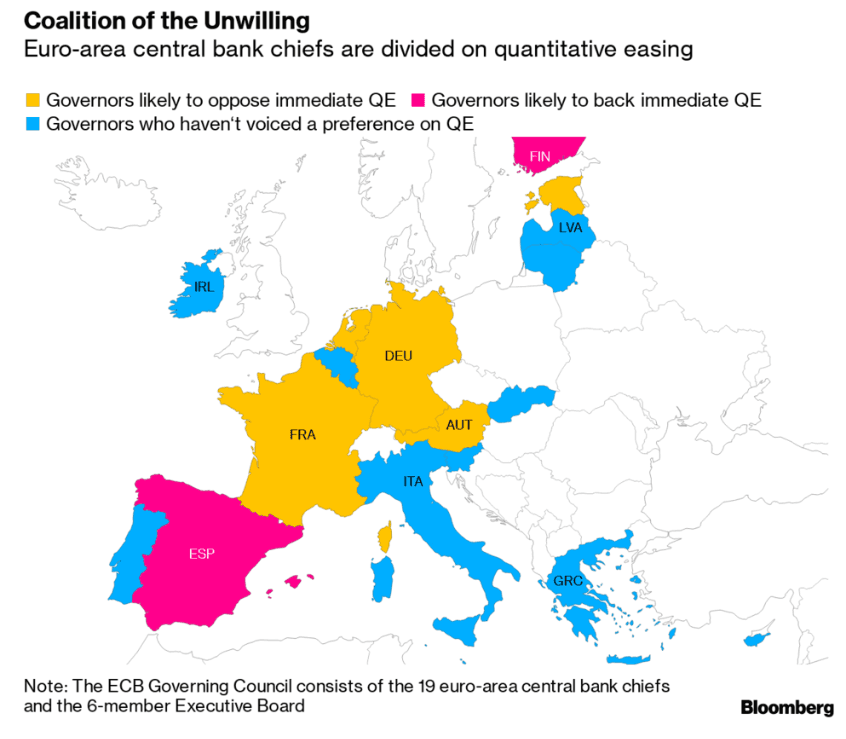

Decision-makers at the ECB - which is expected to announce a new programme of money printing at its September meeting - appear to be gathering to limit Draghi’s ambitions.

Members from Germany, Austria, France and Estonia have expressed skepticism about QE and whether it would have the desired effect or be the right tool for the job.

The latest ECB member to express concern was Banque de France President Francois Villeroy de Galhau, who said he thought a move to increase QE would be premature. Although he did seem to be more in favour of cutting the deposit rate.

His argument was that QE, which involve the ECB in purchasing bonds - mainly longer-dated - from banks, tended to bring down longer-term interest rates and this was not necessary or desirable at the moment since these were already depressed due to global growth concerns.

“The Governing Council estimated in July that this tightening risk mainly concerned the short-term part of the yield curve,” said Villeroy in an interview with French magazine L’Agefi, adding, “in the current context, the aim of any new cut in the deposit rate would be to avoid a tightening of financial conditions for economic actors.”

Indeed, if Villeroy is right and QE did depress long-term interest rates, then a further risk would be that the yield curve would become increasingly flat or even inverted as has happened in the U.S. - something the ECB will want to avoid.

A cut in the deposit rate might be the most benign method to use policy but it is questionable how effective it would be.

There have been other suggestions the ECB may use a tiering system if it cuts rates, which will make certain banks, exempt.

Ultimately, the bottom line is that longer-term policy options for the ECB appear to be running out, especially when compared to the U.S. central bank, the Federal Reserve (Fed).

Interest rates at the Fed are 2.25% so they have more scope to fall than in Europe.

Some analysts have been arguing this poses a medium-term risk to the U.S. Dollar which has more scope to fall from the Fed cutting than the Euro has from the ECB cutting.

It is possible this September we shall find out whether this theory holds up - if it does the short-term recovery in the EUR/USD could turn into something bigger.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

More Harm than Good

The ECB’s interest rates are already at rock-bottom, with a base lending rate of 0.0% and a deposit rate of -0.4%, which means it actually costs commercial Eurozone banks to deposit money with the central bank - a complete reversal of the normal state of affairs in which banks would normally earn interest and get a ‘free lunch’ from depositing their cash with the ECB.

The risk is that more policy would be self-defeating as it would further risk harming the already fragile Eurozone banking system.

In Europe, banks are the lifeblood of the economy since they are the main conduit for financing. This is unlike the U.S. where companies often use other methods such as bond issuance or flotation.

Yet negative interest rates are thought to be costing Eurozone banks E4.8bn a year already with that figure rising should the ECB go ahead and cut rates lower.

Part of the problem is that low interest rates tend to constrict bank’s scope for adding margin on the interest they charge on the loans which is their primary profit channel.

Some Eurozone banks are now even being forced to lend at a loss. Denmark’s third-largest bank, Jyske Bank A/S, for example, announced on Monday, Aug. 5, that it is offering 10-year mortgages at a rate of -0.5%. Another Scandinavian lender Nordea bank are offering 20-year fixed-rate mortgages at 0.0%.

Recently the CEO of German lender Deutsche bank, which is struggling to remain solvent and recently had to amputate its loss-making equity trading arm, as well as let 18k staff go, said that a cut in interest rates would have zero effect on lending and exacerbate inequality because it would boost asset prices such as house prices and penalise savers.

His views echo those of U.S. hedge fund manager Ray Dalio who’s economic model predicts ultra-loose monetary policy will help those with assets - homeowners, stockholders, bondholders etc - and in the process disproportionately widen the wealth gap.

His arguments suggest a political dimension may increasingly come to bear. Rising inequality partly explains the growing popularity of nationalism and populism which are protest movements often supported by the ‘have nots’ - ie those who missed out on the QE fuelled asset boom.

The situation is similar to the late 1920’s and 30s according to Dalio’s model when the last long-term debt cycle ended in the 1929 Wall Street crash and the great depression.

He argues that the next stage of the cycle will see central banks monetise government debt and fiscal spending accelerate as government’s come to replace central banks as the primary method to stimulate the economy - policies driven by a demand to have fed more directly into the hands of people rather than the financial system as is the case with QE.

* Advertisement