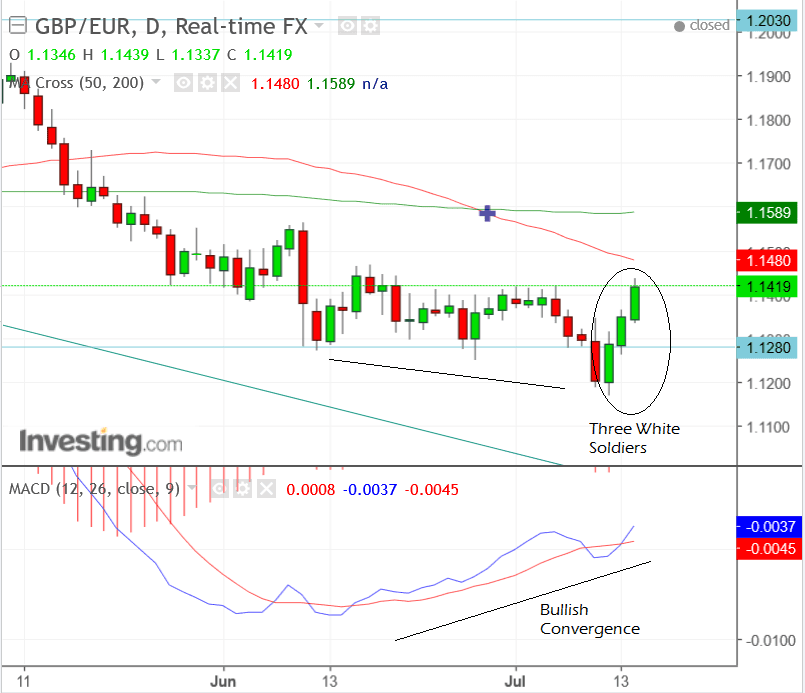

Pound Sterling opens the new week at 1.1419 and is seen trading flat through the Asian and early European sessions.

Concerning the near-term outlook, our technical studies suggest GBP/EUR is positively configured which suggests the short-term downtrend is reversing and the pair could be set for greater gains.

Sterling dropped to eight-month lows last week before staging an impressive rebound; the strength of which caught many in the market by surprise.

The three consecutive up-days at the end of last week formed a clear 'Three White Soldiers' Japanese candlestick pattern which is a very bullish reversal sign, coming as it does at the end of a trend:

This combined with the rising momentum from the MACD which has been converging bullishly with price over recent weeks is a sign the pair may be about to move higher.

We look for a break above Friday’s highs at 1.1440 to signal an extension higher, however, an obstacle soon presents itself at 1.1480 in the form of the 50-day moving average, which is likely to be the focus of much selling pressure, and is a probable location for a pull-back or reversal.

So even a break above 1.1440 is unlikely to extend far before meeting tough resistance; nevertheless, the pair will probably eventually break above the 50-day, indicated by a move above 1.1515 and reach the 200-day MA at 1.1580, given the strength of the perceived bullish reversal.

Get up to 5% more foreign exchange by using a specialist provider. Get closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here

Data that will Guide the Pound

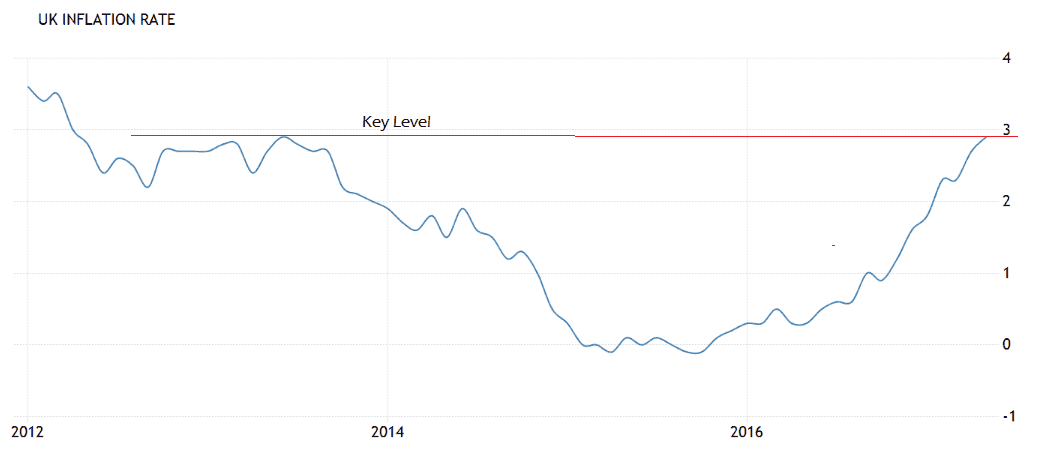

The standout release for Sterling in the week ahead is June Inflation data which is out at 9.30 BST on Tuesday July 18.

The release is important because it impacts on the decision making of the Bank of England (BOE), which in turn is a major driver of the Pound.

Inflation has risen steeply after the Pound weakened following the referendum, which had the consequence of pushing up the prices of imports.

Inflation in May stood at 2.9% year-on-year (yoy: ie compared to May 2016), and 0.3% month-on-month (mom).

The consensus amongst analysts is that it will remain at 2.9% in June yoy but rise at a lesser 0.2% mom.

However, global investment bank TD Securities think the market is being too dovish and forecast a higher 3.0% rise in inflation.

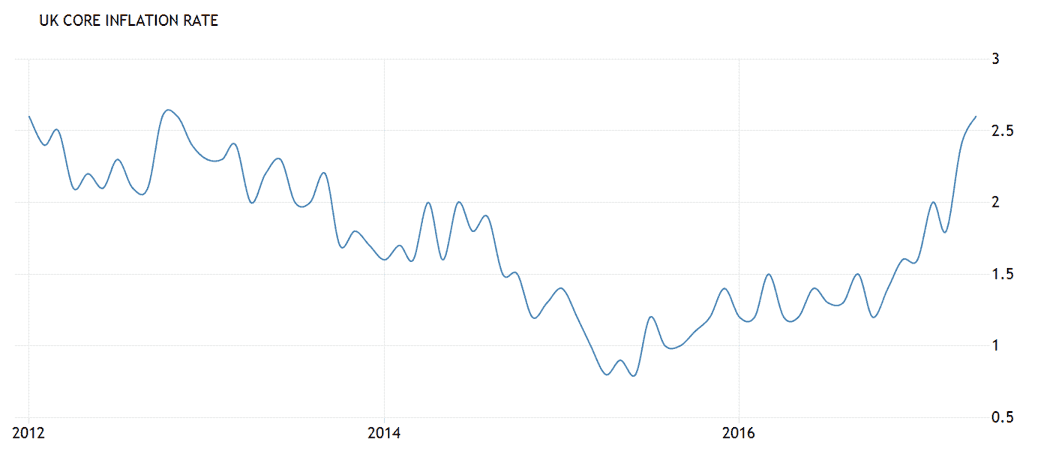

TD expect Core inflation to come out at 2.6% which is the same as the market.

A rise in the cost of utilities is likely to be the driving force behind higher broad inflation and stable core.

“Inflation is likely to have continued its march upward in June, in part due to utility price increases. Core inflation, meanwhile, is likely to have remained stable.”

Nor do TD Securities see this as the “peak for inflation” as core could rise 1 or 2 basis points and headline could rise to the “min-3% range”, which would, “head up the debate about a (single) rate hike later this year.

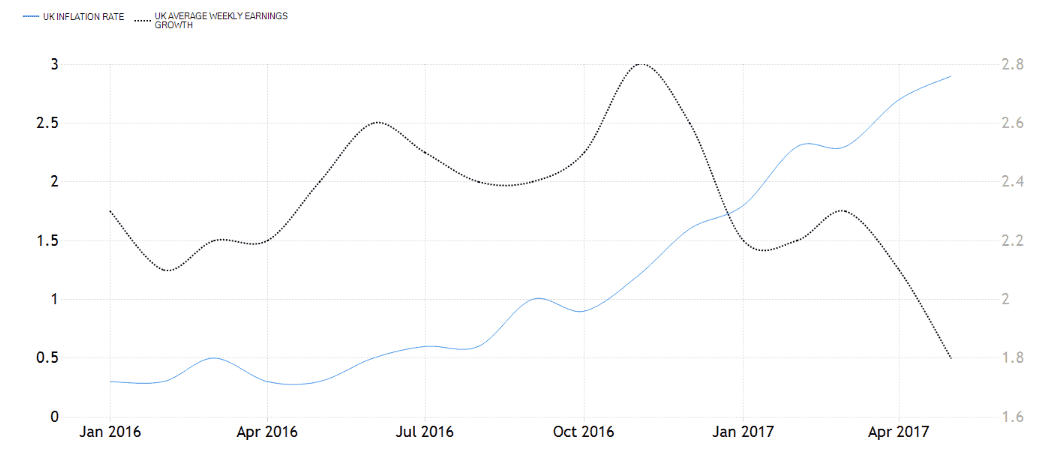

Incidentally the divergence between slowing average earnings in the UK and rising inflation is probably the root cause of the slowdown in the high street or “consumption” as economists like to call it.

The drag on growth from people spending less money is likely to keep the hawks at the BOE in check and limit any possibility of a rate hike.

We know Carney for one won’t change his view until the “trade-off” facing the MPC “continues to lessen” by which he means the trade-off between slowing growth and rising inflation.

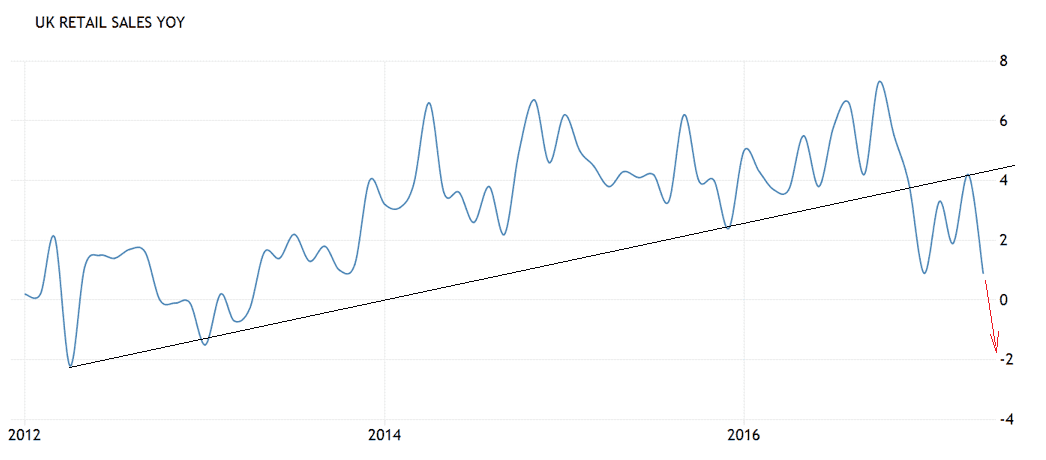

Which brings us on to the other major release of the week for Sterling – Retail Sales on Thursday, July 20 at 9.30.

The market is currently being very optimistic about the gains expected in June.

They see headline Sales rising 2.6% yoy – which is a big jump from the previous 0.9% print; and Core increasing 2.4% from May’s very much lower 0.6% rise.

The market also expects a monthly rise of 0.4% for headline and 0.5% for core from -1.2% and -1.6% respectively in May.

This turnaround appears hugely optimistic from both our and TD Securities perspective, and seems to have little logic backing it up.

Analysts at TD Securities are of the opinion that Sales will not rise by anything (0.0%) mom in June rather than the 0.4% suggested by the market – we agree.

The picture below showing historical Retail Sales data shows a breakdown in the prior up-trend which gives the outlook a definite bearish hue.

The look and feel of the chart betokens a more negative print next Thursday than a more positive, which would also make more sense given the fall in real earnings.

BK Asset Management’s Kathy Lien, however, thinks there is a chance of a better-than-expected print:

“The smaller decline in shop pricesand the uptick in BRC retail sales monitor points to stronger numbers that should help rather than hurt the GBP/USD rally,”

Whilst this fits with the bullish technical outlook we, nevertheless, retain a negative bias.

Data for the Euro

The main event for the Euro in the week ahead is the European Central Bank (ECB) rate meeting on Thursday at 12.45 BST.

No actual policy changes are expected at the meeting, ie changes to interest rates or the QE programme.

There is a possibility, however, that the ECB may tweak the language in their accompanying statement which provides guidance.

They may well remove the phrase that they will ‘increase the pace of QE’, or asset purchases as they are also known, should conditions require it, as suggested in a recent note by Nomura bank, for example.

A variation on this idea has also been suggested by Canadian investment bank TD securities:

“We expect policy to be left unchanged, but the ECB is likely to tweak the language, indicating that QE can now only be increased in duration, but not size.”

According to Nomura, however, this expectation sets up the risk that if the ECB do not change the language of the statement the Euro will fall, as it has already reached relatively overstretched levels.

An important data release in the run up to the rate meeting is inflation data on Monday, which is forecast to show a 1.3% rise in June – the same as the previous month – on a year-on-year basis, ie compared to June 2016.

Any slowdown in inflation, incidentally, will weaken the Euro as it will make the ECB more reluctant to unwind stimulus.

The other major release in the week ahead is the ZEW economic sentiment survey, out at 10.00 BST on Tuesday, July 16.

The ZEW is based on interviews with 350 economists and analysts and assess their views on the economy and the medium-term outlook, e.g the next 6-months. It is considered an accurate leading indicator for the Eurozone economy.