- GBP/EUR near 4-month low but potentially bottoming

- UK inflation & labour data could prompt retest of 1.14

- Approximate 1.1269 to 1.1426 range likely this week

Image © Adobe Images

The Pound to Euro exchange rate entered the new week near four-month lows but could have scope for a rebound and retest of 1.14 up ahead if the latest UK inflation figures lead the market to anticipate additional monetary 'tightening' coming from the Bank of England (BoE) sooner rather than later.

Sterling was a middling performer among major currencies last week having lost half a percentage point to the Euro, Norwegian Krone and Australian Dollar while falling more than two percent in relation to a resurgent Japanese Yen, although there could be brighter days ahead.

This is after Office for National Statistics (ONS) figures suggested on Friday that the economy has so far weathered increased energy costs better than almost all forecasters including the Bank of England had anticipated.

Friday's data lifted the Sterling-Euro rate from close to four-month lows near 1.12 and could have sewn the seeds of another attempted recovery above the 1.14 handle that was tested during the early days of last week.

"We now forecast Q4 GDP to grow by 0.1% q/q (+0.5pp from our previous forecast) and Q1 to contract by 0.2% q/q (+0.1pp from our previous forecast). Our near-term revisions are predicated on the strength of the latest GDP releases," says Abbas Khan, a UK economist at Barclays.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of late September recovery indicating possible areas of technical support for Sterling. Click image for closer inspection.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of late September recovery indicating possible areas of technical support for Sterling. Click image for closer inspection.

"In the back end of the forecast (from Q1 24 onward), we expect a shallower recovery due to a larger degree of monetary tightening than previously anticipated," Khan writes in a Friday review of Barclays' economic forecasts.

November's 0.1% increase in GDP means the UK economy expanded in two out of three months in the final quarter and is a strong indication of a widely expected descent into recession being avoided despite a further large increase in business and household energy prices during the period.

This almost certainly has implications for the interest rate outlook after the BoE indicated in December that it would likely lift Bank Rate in line with expectations implied in the Overnight Index Swap even with the economy wallowing in the recession envisaged in November's forecasts.

"To give the most straightforward but also immediately relevant example: the scope for energy price rises to trigger the infamous second round effects in price, wage and cost dynamics – the dynamics that threaten to create persistence in inflation even after the original external stimulus abates – is greater when the corporate sector enjoys pricing power, and the labour market is tight," the BoE's chief economist Huw Pill said in a speech last week.

"In an attempt to protect their own real income from the unavoidable impact of higher external prices, the longer that firms try to maintain real profit margins and employees try to maintain real wages at pre-energy price shock levels, the more likely it is that domestically-generated inflation will achieve its own self-sustaining momentum even as the external impulse to UK inflation recedes," he also later told the Money Marketeers of New York University.

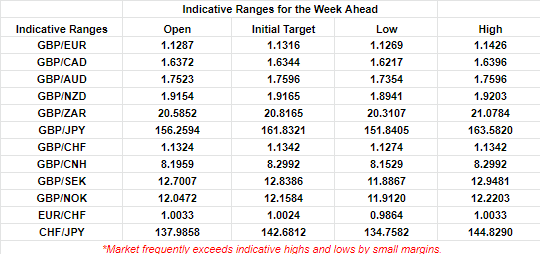

Above: Financial model-derived estimates of probable trading ranges for selected currency pairs this week. Source Pound Sterling Live. If you are looking to protect or boost your international payment budget you could consider securing today's rate for use in the future, or set an order for your ideal rate when it is achieved, more information can be found here.

Above: Financial model-derived estimates of probable trading ranges for selected currency pairs this week. Source Pound Sterling Live. If you are looking to protect or boost your international payment budget you could consider securing today's rate for use in the future, or set an order for your ideal rate when it is achieved, more information can be found here.

With the economy proving more resilient than imagined, many in and around the markets may already be expecting the BoE to announce additional increases in Bank Rate sooner rather than later but such expectations could potentially be encouraged further by the inflation figures due out this week.

"After the CPI measure hit a 40-year high of 11.1% in October, it dropped to 10.7% in November, the biggest month-on-month fall since July 2021. There are some reasons to think the decline continued in December," says Andrew Goodwin, chief UK economist at Oxford Economics.

"On the other hand, volatility in some of components of core inflation, which drove a chunky drop in November, may not have been so helpful the following month. On balance, this leads us to expect that CPI inflation held steady at 10.7% in December," he writes in a Friday research briefing.

The market consensus is for inflation to have declined from 10.7% to 10.5% in December and for the core inflation rate to have eased from 6.3% to 6.2% but if the Oxford Economics team is on the money with its forecast then there may well be implications for the Bank Rate outlook.

Wednesday's inflation figures are the highlight but will be preceded on Tuesday by employment and wage data covering the December and November months respectively, which could also have implications for BoE policy.

Above: Pound to Euro rate shown at daily intervals with selected moving averages and Fibonacci retracements of March 2022 and April 2022 declines indicating possible areas of technical resistance for Sterling. Click image for closer inspection. To optimise the timing of international payments you could consider setting a free FX rate alert here.

Above: Pound to Euro rate shown at daily intervals with selected moving averages and Fibonacci retracements of March 2022 and April 2022 declines indicating possible areas of technical resistance for Sterling. Click image for closer inspection. To optimise the timing of international payments you could consider setting a free FX rate alert here.