- EUR tumbles during ECB press conference

- As Lagarde sends mixed messages on future policy

- Eurozone fragmentation risks also grow

Above: The ECB held its Governing Council Press Conference on 9 June 2022 in Amsterdam, The Netherlands. Photo by Dirk Claus/ECB.

The Euro fell against the Dollar and British Pound during the course of a press conference delivered by European Central Bank Christine Lagarde on the occasion of the Bank's June policy update.

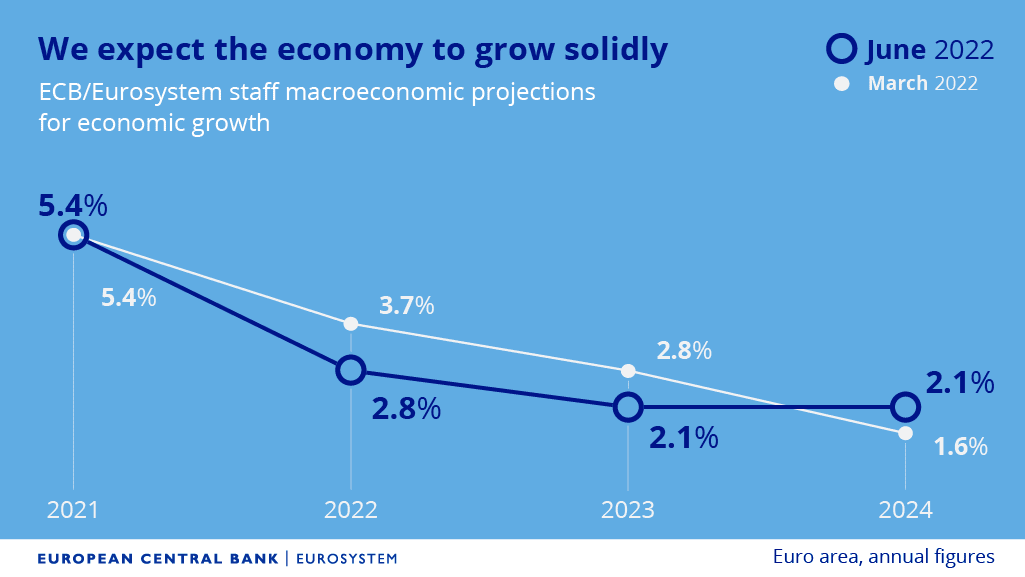

The Bank initially sent a clear message of intent in its initial written statement in which it signalled a 25 basis point rate hike in July and another hike in September (this could be a 50bp move depending on inflation expectations) while lowering GDP forecasts and raising inflation forecasts.

The Euro was relatively steady in response as the guidance was largely as expected, but it lost ground in a marked fashion when Lagarde fielded questions from assembled journalists.

"Once the press conference began, however, the path forward from the ECB became more ambiguous again," says Simon Harvey, Head of FX Analysis at Monex Europe. "The theme of opaque forward guidance continued throughout the press conference."

The Pound to Euro exchange rate fell to a low of 1.1638 on the day before rallying to a peak at 1.1783 during the press conference. The Euro to Dollar exchange rate was as high as 1.0772 before retreating to a low at 1.0645.

Of note to Harvey was Lagarde's unwillingness to talk about 'neutral' rates, which is essentially the level interest rates must rise to in order for monetary policy to become neither stimulatory or restrictive.

This "should provide a ceiling for terminal rate pricing in this current environment – along with outlining what the ECB’s mechanism would be to mitigate bond market fragmentation," explains Harvey.

But what appeared to be of primary concern to markets was Lagarde's confirmation to the press the ECB does not yet have a concrete 'anti-fragmentation' tool at hand.

This anti-fragmentation tool is what investors believe is required to ensure fractures do not emerge in the Eurozone economy once interest rates start to rise.

Of concern is that rising ECB rates will push up the cost of borrowing for all Eurozone countries, via higher yields paid on government-issued bonds.

But countries with weaker economies and poorer finances would see their cost of borrowing rise faster than the core Eurozone economies of Germany and France.

Italy is of particular concern.

Above: Watch the ECB press conference in full.

The verdict delivered by financial markets to Lagarde's comments was negative: the Euro fell, Italian bank stocks fell and Italian funding costs rose sharply; classic signs of wobbling financial market confidence.

"Literally worst possible outcome for ECB - EUR is lower, rates are higher, peripheral is wider and Stoxx is lower," says Brent Donnelly, CEO of Spectra Markets. (Set your FX rate alert here).

During the Lagarde press conference Italy's 10 year risk spread over Germany rose to its highest since May 2020 in recognition of no specific new anti-fragmentation instrument being mentioned.

Above: Italy 10 year risk spread over Germany. Image: Bloomberg, courtesy of Holger Zschaepitz.

By selling the Euro the market is signalling a concern that rising interest rates could fuel a return to stresses last seen during the region's debt crisis of 2010-2012.

Italian bank stocks meanwhile went sharply negative in the wake of the developments, reflecting growing investor fears over the implications of rising ECB rates to economies such as Italy's.

At some point the ECB will need to put in place a mechanism to ensure the spread between the bond yields of various Eurozone economies remains manageable.

Holger Schmieding, an economist at Berenberg Bank says the ECB issued a "muddled message on fragmentation... with the end of net asset purchases, the risk that yield spreads may widen more than a majority on the ECB council considers warranted has increased".

Analysts suggest the outlook for the Euro remains challenging in the wake of Thursday's developments.

"EUR/USD is a 'first into a recession play'. Risks of a debt crisis + Ukraine war + squeeze in household incomes = Europe will fall into a recession ahead of the US. Puts EUR firmly on a path to parity. Even the most hawkish ECB in a decade can't support the single currency," says Viraj Patel, Macro Strategist at Vanda Research.

"Although the rate statement in isolation suggested that 1.07 may be a firm support for EURUSD over the coming weeks, the lack of assurances by President Lagarde stressed that downside risks for EURUSD remain over the coming weeks. In response to today’s event, we remain committed to our month-end EURUSD target of 1.06, with tomorrow’s US CPI report the next hurdle en route," says Monex's Harvey.

A weakening EUR/USD would on balance suggest a weakening EUR/GBP, all else being equal.

Details of the ECB's June Policy Update

- ECB expects to raise rates 25 basis points in July and again in September

- Inflation to remain undesirably elevated for some time

- ECB raises inflation forecasts, now predicts 2.1% in 2024, up from 1.9% previously

- 2023 inflation forecast at 3.5% vs. 2.1% previously

- 2022 inflation is forecast at 6.8%, up from previous forecasts of 5.1%

- ECB to continue monitoring bank funding conditions

- Reiterates PEPP can be restarted if Covid crisis worsens

"ECB is woefully behind the curve if they are taking 50bps off the table in July. Saying they intend to hike by 25bps in Jul & in Sep again. But they need to go harder & faster else they'll miss the window to get rates above 0%... with recession risks kicking in 2H22," says Vanda Research's Patel.