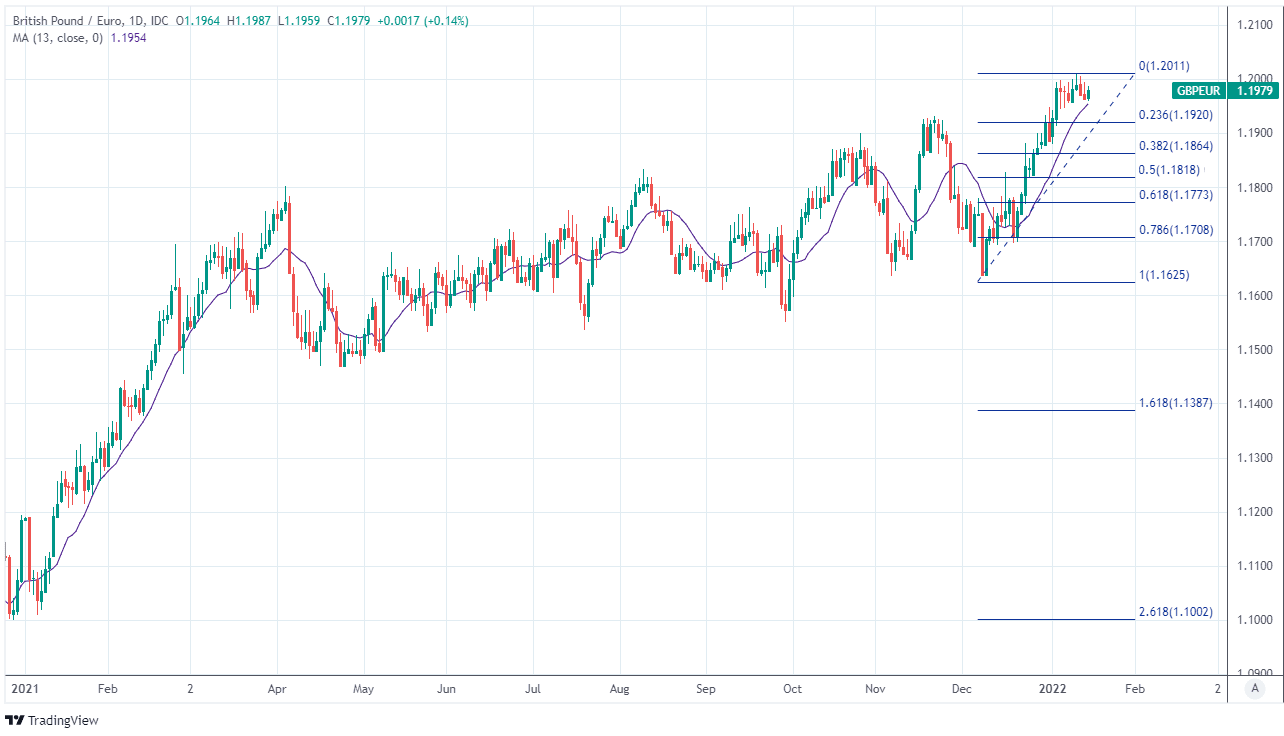

- GBP/EUR looking to hold above 1.1950

- Supports near 1.1954, 1.1920, 1.1864

- UK jobs, CPI data & BoE policy in focus

- Potential to fuel bets on a Feb rate rise

- But rejuvenated EUR could limit upside

Image © Adobe Images

The Pound to Euro exchange rate rose tepidly above 1.20 for the first time since February 2020 last week and could be set to remain buoyant above the 1.1950 level over the coming days, although upside for Sterling may be limited by a perkier performance from the European single currency.

Pound Sterling held onto early January’s gains over most major counterparts last week but was little changed against the single currency by the Friday close after a mid-week rally in EUR/USD helped to cut short the Pound to Euro exchange rate’s earlier foray above the 1.20 handle.

GBP/EUR had climbed briefly above the round number before Wednesday’s rally in EUR/USD curbed Sterling’s upward momentum, leaving it trading in a narrow band between 1.1954 and 1.2005.

That range could continue to define price action through much of the week ahead unless Wednesday’s release of UK inflation figures for December happens to provide Sterling with inspiration for another attempt at reclaiming 1.20.

“A 25bp BoE rate hike is still priced with an 80% probability for the February 3rd meeting - which will likely keep GBP supported over the coming weeks,” says Francesco Pesole, an FX strategist at ING.

“The UK has just released some better activity numbers for November, including monthly GDP, industrial production and services indices. Even the trade deficit narrowed. This suggests the UK economy might have had a little insulation heading into the Covid-restricted December,” Pesole said on Friday.

Above: GBP/EUR shown at daily intervals with selected moving-averages and Fibonacci retracements of December rally indicating possible areas of technical support for Sterling.

- Reference rates at publication:

GBP to EUR: 1.1979 - High street bank rates (indicative): 1.1660 - 1.1740

- Payment specialist rates (indicative: 1.1870 - 1.1920

- Find out more about specialist rates and service, here

- Set up an exchange rate alert, here

Wednesday’s inflation figures are the highlight of the week for Sterling but will come in the wake of the latest employment data on Tuesday and a short time ahead of appearances before the Treasury Select Committee by Bank of England (BoE) Governor Andrew Bailey and Deputy Governor Jon Cunliffe.

“After rising to a 10-year high of 5.1% in November, we think that CPI inflation will tread water for a couple of months until a leap in utility prices pushes it up all the way to 6.9% in April,” says Ruth Gregory, a senior economist at Capital Economics.

“The next big shift will come when utility prices rise on 1st April. We think a rise in the region of 50% is on the cards. That would add 2.1ppts to overall inflation and push it up to 6.9%,” Gregory and colleagues said in a research briefing on Friday.

Consensus among economists suggests the annual rate of inflation climbed from 5.1% to a new decade high of 5.2% in December and the Pound could potentially be sensitive to the actual outcome if it impacts market expectations for the timing of a further interest rate rise from the BoE.

Pricing in the overnight-indexed-swap market suggested on Friday that investors saw the March decision as the most likely for an increase in Bank Rate from 0.25% to 0.50%, with the market implied rate for the February 03 decision sitting at 0.42% last week.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

“The headline rate of CPI inflation likely was unchanged at 5.1% in December. Pick-ups in food and car price inflation probably were offset by falls in the tobacco and clothing components,” says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

Sterling could potentially benefit if Wednesday’s data surprises on the upside of expectations and if as a result the market comes to view February as more likely for a next step by the BoE to withdraw the interest rate cuts announced in support of the economy at the onset of the pandemic.

“I remain positive on the GBP and bearish EUR/GBP but a touch more cautious on the latter given the recent move,” says Jonathan Pierce, a currency trader at Credit Suisse. “A bit more flexibility is required but I’m still inclined to be selling the cross towards .8400 {buying GBP/EUR toward 1.1904].”

Financial markets have come to anticipate a series of rate rises from the BoE in 2022 as part of a process intended to ensure that inflation returns to the 2% target over the coming years, with some measures of expectations suggesting scope for Bank Rate to rise to one percent or more.

The rising tide of market expectations for Bank Rate has had an uplifting influence on the Pound to Euro rate although with the rhetorical stance of the European Central Bank (ECB) recently beginning to shift in a less ‘dovish’ direction, Sterling may now struggle to sustain its recent upward momentum.

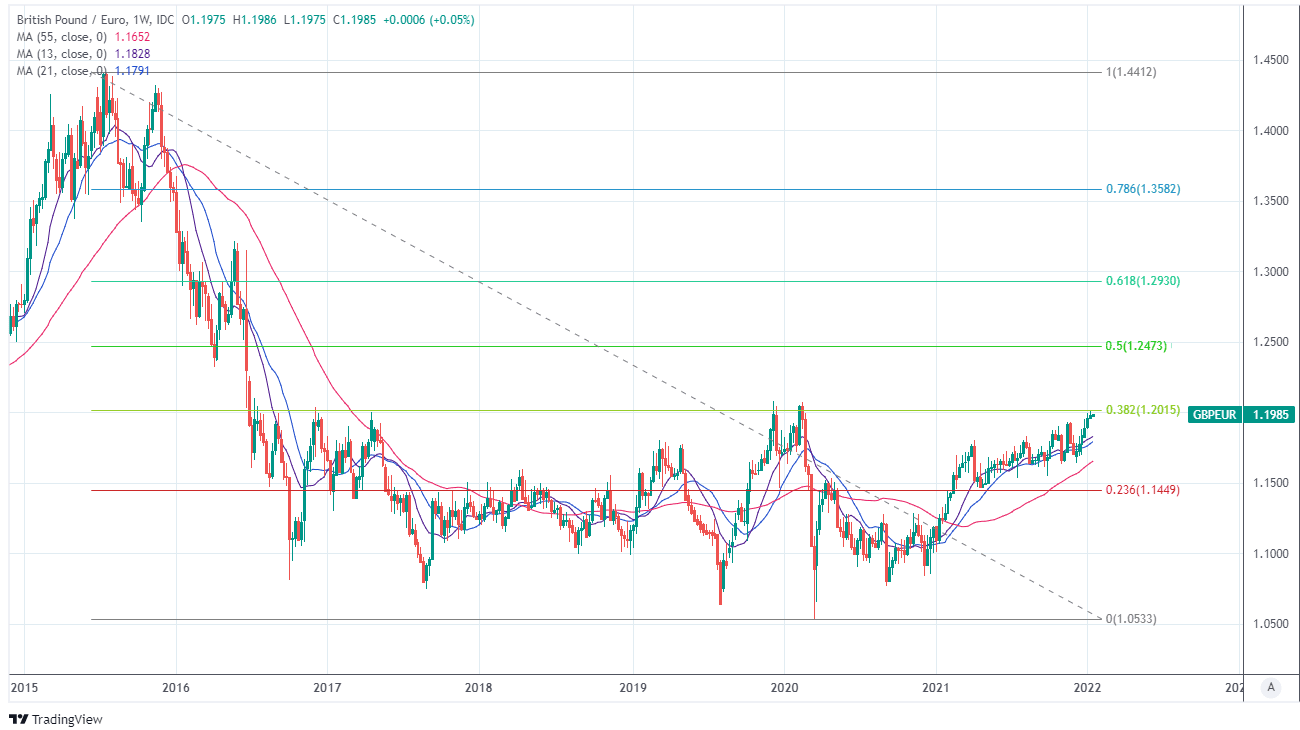

Above: GBP/EUR shown at weekly intervals with Fibonacci retracements of late 2015’s referendum-induced decline indicating possible areas of technical resistance to a further medium and long-term recovery by Sterling.

“We expect the drivers of inflation to ease over the course of this year. But we understand that rising prices are a concern for many people, and we take that concern very seriously. So let me reiterate that our commitment to price stability remains unwavering. We will take any measures necessary to ensure that we deliver on our inflation target of 2% over the medium term,” ECB President Christine Lagarde said on Friday.

The ECB has so far insisted there’s almost no chance of an interest rate rise in the Eurozone this year or next due to its expectation that recently elevated inflation pressures would subside of their own accord over the course of 2022, although with inflation reaching another record high in December, there’s a chance that it could begin to acknowledge during the months ahead an increased risk of it eventually needing to act.

To the extent that any such shift in the ECB’s rhetoric has a supportive impact on EUR/USD, it could also act as a headwind for Sterling, although the Eurozone economic calendar is devoid of major appointments this week and so the Pound to Euro rate may be likely to take its cues from Wednesday’s inflation figures and any relevant commentary from BoE Governor Bailey and colleagues in testimony about the latest financial stability report.

“CPI inflation in the advanced economies will fall sharply in 2022, in our view. But the high starting point means that the economic and policy implications of any drop will depend on the speed – and timing – of the decline,” says Ben May, director of global macro research at Oxford Economics.

“Our baseline view is that most economies will see around a 3ppt drop in the headline rate between December 2021 and December 2022, reflecting a combination of weaker energy and core inflation. With the exception of the US, we think lower energy and core inflation will limit the pressure on central banks to implement more than one or two rate hikes at most next year,” May and colleagues wrote in research briefing last week.