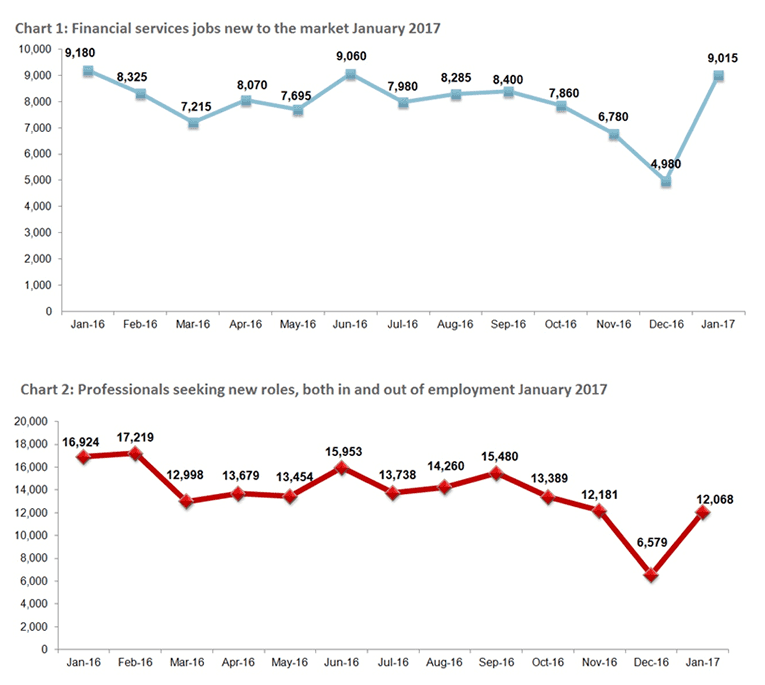

The UK’s financial services jobs market got off to a cautious start to 2017 as an 83% jump in the number of people seeking jobs deemed to be disappointing.

According to the Morgan McKinley London Employment Monitor for February 2017 there was an 81% increase in jobs available and an 83% increase in professionals seeking jobs.

“If the January jobs surge isn’t in the triple digits, something’s off”, said Hakan Enver, Operations Director, Morgan McKinley Financial Services. “Until the terms of Brexit are known and put in motion, the jobs market will remain cautious”.

Morgan McKinley are one of the leading financial services job brokers in the City of London and their monthly employment report is considered a good barometer of sentiment in the City.

And, contributing to the decrease is the trickling off of non-British EU nationals working in the City, who comprise up to 10% of its workforce.

This view echoes the findings of the CIPD and Adecco who reported a day earlier that EU nationals are no longer flocking to the UK following the Brexit vote.

The report shows companies are reporting labour and skills shortages in the food supply chain as well as in sectors such as manufacturing, healthcare and hospitality.

25% also had evidence that the EU nationals they employed were considering either leaving their organisation or the UK in 2017.

And it appears the same phenomenon is taking place in the financial services sector.

“Many of our non-British clients are choosing to return home, or seeking opportunities elsewhere in Europe”, says Enver. “People wanting to get ahead of the threat of having their right to work revoked is understandable, but is a huge loss for the City”.

Last week, the House of Commons voted against protecting the residency rights of EU citizens already residing in the United Kingdom.

Though the vote has no immediate legal effect, Morgan McKinley believes it leaves existing EU nationals in limbo, and acts as a deterrent to top talent from the continent who might otherwise have considered a career in London.

The government has said freedom of movement is a key negotiating tool for Brexit talks with the EU, leaving many to hold out hope that a mutually beneficial solution is forthcoming in the months ahead.

London Losing its Pull, But No Major Alternative

Chief executive of the British Bankers Association, Anthony Browne, characterised financial institutions as “quivering over the relocate button” ahead of Brexit negotiations.

According to a survey conducted by the market research company Ipsos MORI, 58% of business leaders from Britain’s largest firms reported Brexit having already had a negative impact on business.

In addition, a January EY survey reports that half of the financial services institutions that threatened to relocate staff have already done so.

Paris, Dublin and Frankfurt are among the top cities hoping to replace London as Europe’s financial capital.

However, Enver believes neither of these cities has the capacity to replace London.

“When you add up the half million people who work in the City of London and their spouses and children, you’re looking at over triple the population of Frankfurt, and over half the population of Paris”, says Enver. “It’s all well and good to put on a charm offensive, but without the infrastructure to absorb the City’s financial services industry in full, it’s wishful thinking”.

Morgan McKinley believes a more likely scenario is a decentralised approach in which institutions spread operations out across a handful of cities.

Most large institutions have drafted plans for relocating a percentage of their trading operations to other cities.

“Whether the relocation preparations are contingency plans or idle threats remains to be seen”, says Enver. “That said, it’s hard to imagine a scenario in which a hard Brexit doesn’t trigger some movement out of London".

But, it’s New York that London Should Really Worry About

While some banks are looking to increase their presence on the continent Morgan McKinley warn that it is New York that is most likely to threaten London’s dominance as the world’s financial centre.

In the early days of his presidency, Donald Trump signed an executive order calling for a review of the 2010 so-called Dodd-Frank financial services regulations.

And with the recent confirmation of former Goldman Sachs banker Steven Mnuchin as Treasury Secretary, pundits are suggesting big changes are in the air.

While it remains unclear what recommendations the review will result in, deregulation is expected.

The British financial services sector anticipates a loss in competitiveness if its own regulatory system does not mirror America’s.

The scramble to adapt will be complicated by the mix of EU regulations that continue to govern the British banking sector.

“If London doesn’t adapt to Dodd-Frank changes, then we should worry about losing jobs to New York much more than losing jobs to Frankfurt”, said Enver.

Simeon Djankov at the Peterson Institute for International Economics agrees that the real threat to London lies across the Atlantic.

"Politicians need to be more constructive in Brexit negotiations, because otherwise, the stats point to a loss, not just for the UK but for all of Europe," says Djankov.

Djankov says financial service companies move out of London, it is unlikely that many would relocate to another EU city.

“Europe does not have anything comparable to London to offer relocating companies. Financial centers outside of the European Union, would be more likely to attract the business because other EU financial centers rank so much lower,” says the economist.

“The pull away from London in several financial services sectors would be mostly towards the United States.”