Image © Adobe Images

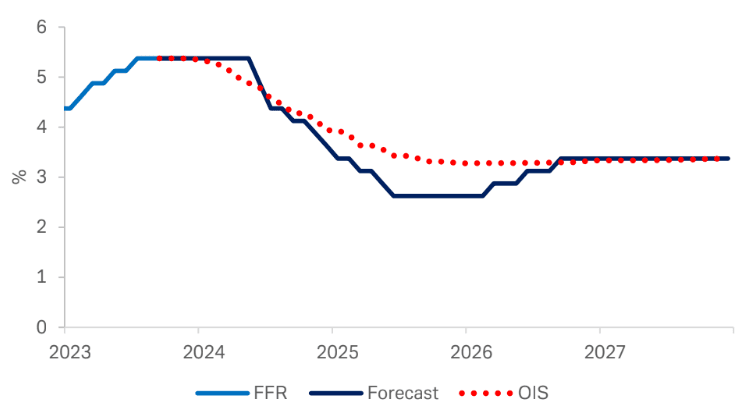

The Federal Reserve will wait until June before cutting interest rates, but from this point, the pace of rate cuts could surprise markets.

This is according to Deutsche Bank, where fixed-income strategists have updated clients with their latest views, acknowledging their projected pace of cuts is aggressive relative to market pricing.

"We expect a mild recession with inflation on track to 2% to lead the Fed to cut more aggressively next year than market pricing or Fed projections," says Matthew Raskin,

Strategist at Deutsche Bank.

Deutsche's U.S. economists predict a mild recession to form in the first half of 2024, bringing the U.S. unemployment rate above 4.5% around mid-year.

Above: "With that macro backdrop, we project more Fed rate cuts than market pricing" - Deutsche Bank.

Core inflation is expected to run at around 2.5% year-on-year by this point.

"Against that backdrop, we anticipate the Fed will begin to cut rates in June," says Raskin.

Deutsche Bank's baseline projection is for a chunky 175bp worth of cuts to be delivered by the end of 2024, followed by additional cuts in 2025, making for a peak-to-trough decline of 275bp.

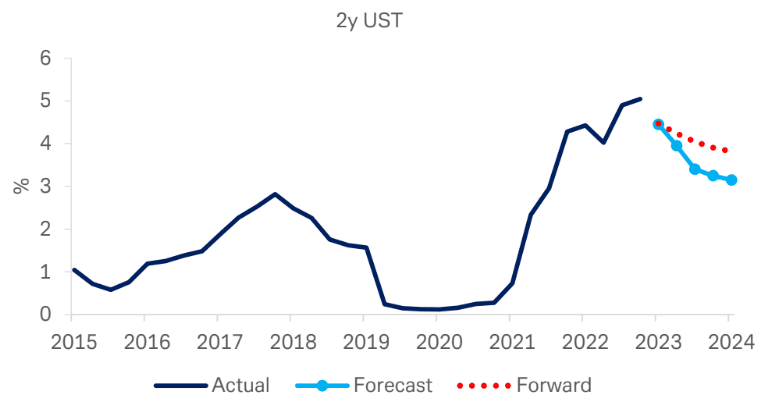

These expectations mean U.S. bond yields will fall further: Deutsche Bank's forecast puts the two-year U.S. Treasury yield at 3.4% by mid-2024 – as Fed cuts approach – moving down to 3.15% by year-end.

Above: Deutsche Bank is forecasting lower U.S. bond yields than the market.

The ten-year is forecasted to be at 4.1% by mid-year and stay around that level, close to its longer-run equilibrium value.

According to Raskin, the stars are aligning for a busy Q1 as the market moves towards Deutsche Bank's expectations:

"While it’s difficult to project the timing of these yield moves and markets over recent weeks have already been shifting in the direction of this outlook (which we first put out in early October), we have the most pronounced moves coming in Q1, in line with recession timing and the historical response of yields and the curve to recessions and Fed cutting cycles."