"It remains difficult to rationalise market pricing of a peak in Bank Rate ~5¾% next spring. With GDP still a fraction below pre-pandemic levels, it is hard to make a credible case for excessive demand," - Natwest Markets

Image © Adobe Images

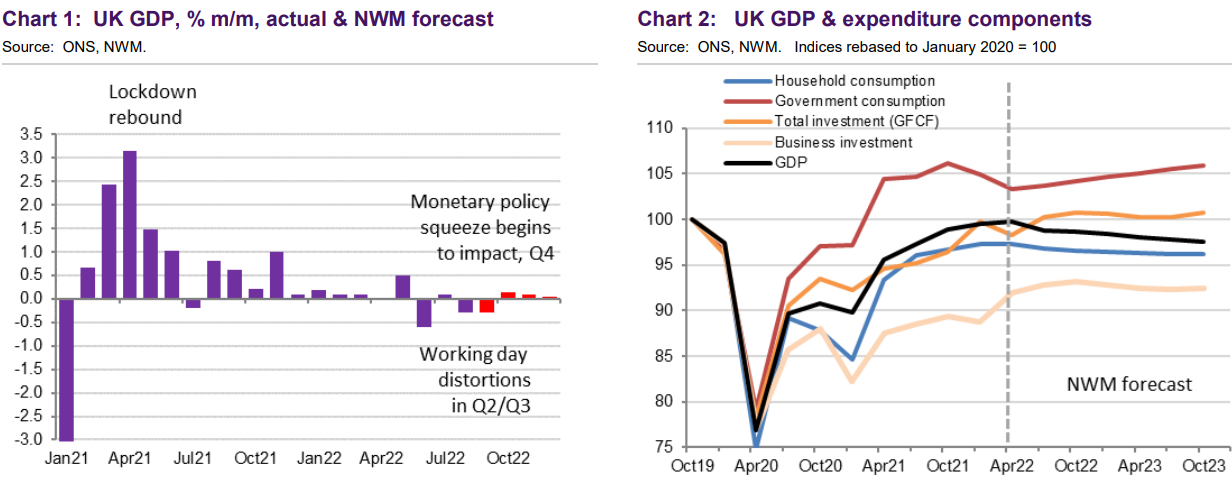

The UK economy shrank notably during August in an outcome that leaves GDP on course for a quarterly fall that would come sooner than many forecasters had anticipated and which could challenge the credibility of market-implied expectations for the Bank of England (BoE) Bank Rate.

UK economic output fell by 0.3% in August when the economist consensus had anticipated an unchanged or zero growth reading while placing the economy on course for a quarterly contraction that would come in contrast to the 0.2% third quarter expansion that was forecast by the BoE in August.

"To adopt the BoE Chief Economist’s preferred adjective, this was a ‘significant’ decline and undershoot vs expectations (consensus 0.0%, NWM +0.1%). Growth in the latest 3 months turned negative (-0.3% from +0.1%) for the first time since the Q1 2021 lockdown – which also feels significant," says Ross Walker, global head of economics and chief UK economist at Natwest Markets.

"We forecast negative quarterly GDP outturns from Q3 2022, persisting throughout 2023. What began as an energy-centred shock which would hit the bottom-third of households by income hardest is evolving into a more conventional monetary policy shock which will hit middle-income households hardest," Walker wrote in a Wednesday research briefing.

Wednesday's August GDP data was released soon after the Office for National Statistics figures revealing the first sign of a crack appearing in the UK labour market where new claims for unemployment-related welfare rose in September at their fastest pace since the early 2021 'lockdown' episode.

Source: Natwest Markets.

Source: Natwest Markets.

Together both sets of figures suggest the UK economy is already underperforming Bank of England forecasts that proved controversial with some economists and parts of the media back in August for what appeared at the time to be an overly pessimistic outlook.

August Monetary Policy Report projections suggested the economy would grow by 0.2% in the third quarter and by 2.3% for the year to the end of September, although August's data potentially places the third quarter outcome beyond reach and may mean that an underperformance of both forecasts is inevitable.

The BoE also forecast in August that the economy would contract by 2.1% for the year to September 2023 if it lifts Bank Rate in line with expectations implied by the Overnight Indexed Swap part of the derivative market, which had previously looked for Bank Rate to reach 3% over that period.

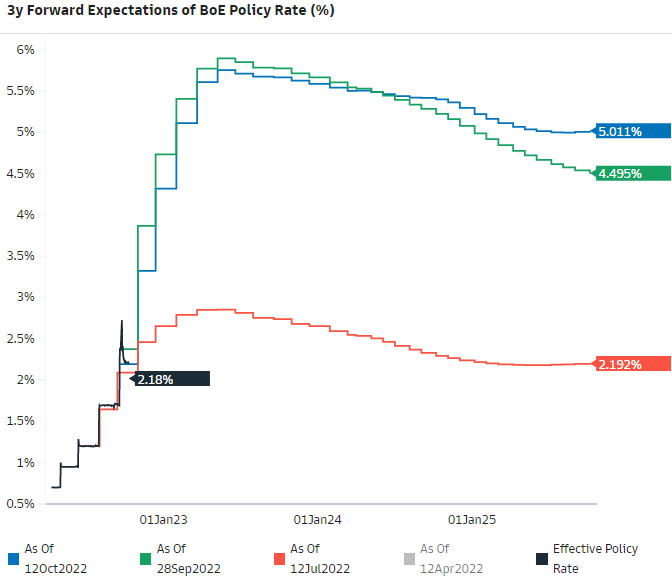

However, since the August report was released, those market-implied expectations for Bank Rate have surged further and now indicate that some investors see the benchmark for borrowing costs as likely to rise above 5% by the early months of the new year.

"In August, the UK economy was already on the verge of a recession with Bank Rate at 1.75% and with only a partial passthrough to mortgage borrowing costs. It remains difficult to rationalise market pricing of a peak in Bank Rate ~5¾% next spring," Walker said on Wednesday.

Source: Goldman Sachs Marquee.

Source: Goldman Sachs Marquee.

"With GDP still a fraction below pre-pandemic levels, it is hard to make a credible case for excessive demand. Is the UK supply-side so badly impaired that the 2% CPI target can only be reached/sustained via a protracted recession/stagnation in output?" he also wondered aloud.

The aggressive shift in market-implied expectations has taken place over a period in which the outlook for the already-underperforming economy has only become more uncertain, given financial market volatility following the late September budget and widespread suggestions that government policy proposals will not help the economy.

Government policy proposals included publicly-funded subsidies for household energy costs that have doubled twice over in the last year and tax cuts that have proven to be as economically contentious for economists and analysts as they have been ideologically contentious for some politicians.

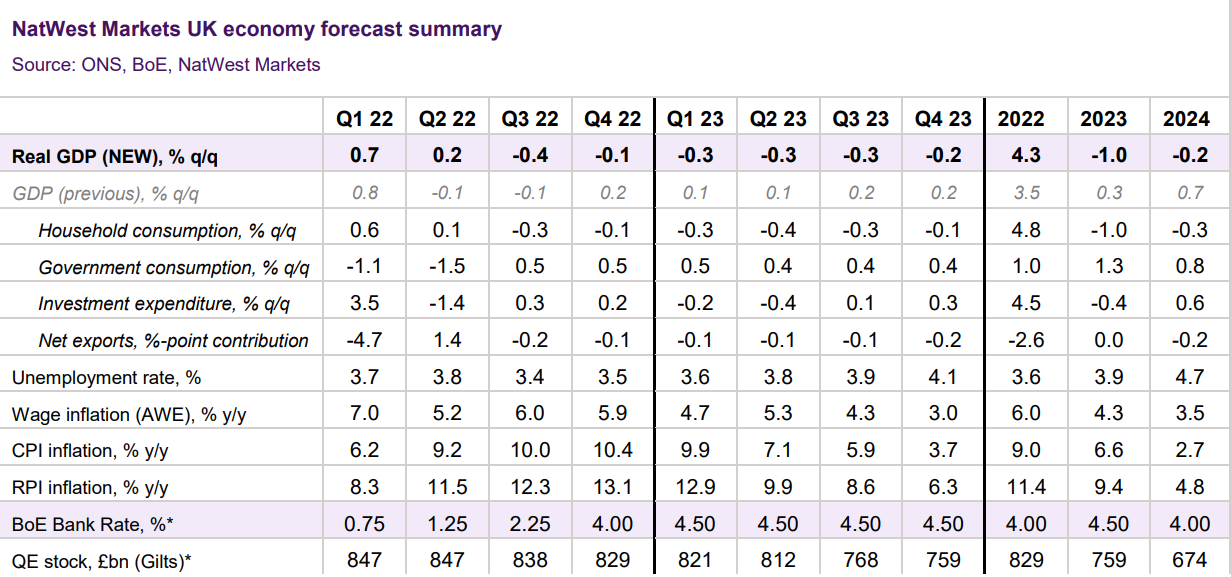

"The fiscal expansion from the misnomered ‘mini budget’ looks set to elicit a more ‘significant’ monetary policy tightening: we forecast Bank Rate to rise by 100bp in November (to 3.25%), +75bp in December (4.0%) and +50bp in February to a cyclical peak of 4.5%. This is some way below market pricing (~5.75% in May 2023) but would amount to a substantial (and probably excessive) monetary shock," Walker said.

"It is far from clear that this degree of policy tightening is required to return inflation to its 2% target," he concluded.

Source: Natwest Markets.

Source: Natwest Markets.