"To improve labor supply, the Fed might try to put volatility in its service to engineer a correction in house prices and risk assets – equities, credit, and Bitcoin too," says Zoltan Pozsar of Credit Suisse.

File image of Chair Jerome Powell, image supplied by the Federal Reserve.

The Federal Reserve is caught in a bind: how does it bring inflation down while at the same time avoiding a jobs-killing recession?

According to a noted fixed income strategist the answer might lie with a major rethink by the Fed as to how it goes about its business: it should generate enough volatility to bring down asset prices, which might well encourage greater labour market participation.

Zoltan Pozsar, Global Head of Short-Term Interest Rate Strategy at Credit Suisse, says "historically, the Fed used rate hikes to engineer recessions that generated the slack needed to keep inflation in check".

But the Fed has been issued a new mandate on top of controlling inflation: that of keeping unemployment low.

How then does the Fed the Fed then keep inflation low and keep unemployment low at the same time?

"The Fed aiming to slow inflation via a recession is unimaginable. Hikes today then are meant to slow inflation without a recession which is not something that the Fed has ever managed to achieved before," says Pozsar.

Pozsar says the Fed must develop a new strategy for the unique set of circumstances it now faces.

One way to lower service sector inflation - that bit of inflation it can control (the Fed is impotent in controlling goods inflation other than by engineering a recession) - would be to boost labour supply.

By boosting labour supply you lower the upside pressure on wages, which is a deflationary force.

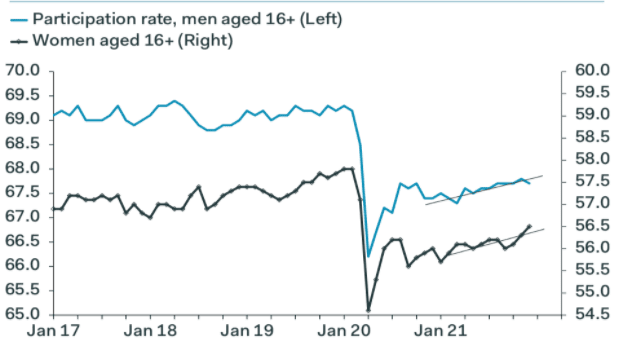

A major puzzle facing U.S. policy makers involves 'missing workers' - the labour force appears to be smaller now than it was pre pandemic, and this is putting upward pressures on wages. (There are approximately 5 million workers still missing from U.S. payrolls compared with the pre-pandemic peak).

Above: U.S. participation rate. Image courtesy of Pantheon Macroeconomics.

Pozsar suggests that in order to boost labour supply asset prices must come down and mortgage costs must go up: early retirement, a drain on the labour force, is typically only possible if pensions pots are strong and mortgage repayments are low.

Equity market inflation and cryptocurrency returns are meanwhile said to be keeping the younger segment of the wage force at home: the "bitcoin-rich" - as Pozsar calls them - are less inclined to work.

Pozsar says one thing the Fed could therefore do to increase labour market supply would be to boost the term structure of the rates market: the problem the U.S. economy faces is that near-term bond yields are higher while further out yields are relatively steady.

Term premia matters as it instructs mortgage rates and equity market valuations: as long as longer-term funding is relatively stable and affordable mortgage rates will remain relatively subdued.

Pozsar calls for a boost to market volatility in order to awaken the longer end of the curve: "volatility is the best policeman of risk appetite and risk assets."

"To improve labor supply, the Fed might try to put volatility in its service to engineer a correction in house prices and risk assets – equities, credit, and Bitcoin too," says Pozsar.

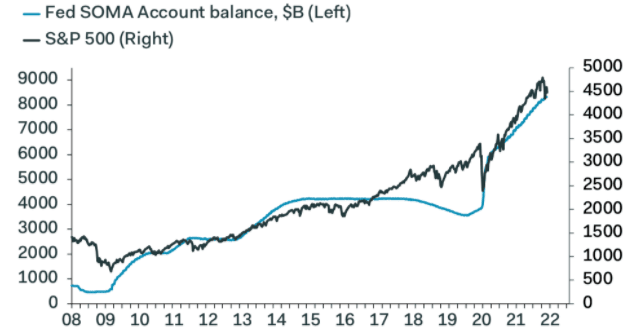

Above: "THE FED’S BALANCE SHEET IS SUPPORTING ASSET PRICES, FOR NOW" - Pantheon Macroeconomics.

The analyst says central bankers like Paul Volcker or Mario Draghi either sparked or tamed volatility: "Draghi tamed volatility with his bumblebee-themed speech, and Volcker sparked volatility by starting to target quantities instead of rates, and he didn’t talk too much about what he was doing – he kept the market guessing."

"Maybe the Fed should hike 50 bps in March, put an end to press conferences, and sell $50 billion of 10-year notes the next day... Maybe FOMC members talk too much. They don’t keep the market guessing. They suppress volatility," says Pozsar.

What is needed, he says, is a new "Volcker" moment.

But will raising mortgage rates and sending the stock market lower spark a recession?

"No, lower risk assets won’t kill growth. This is not a balance sheet recovery, and no, higher mortgage rates won’t kill growth either – wage growth at 5% can absorb higher monthly payments. The curve is flat and borderline inverted, and

delivering slope into it can come from higher term premia engineered by the Fed, not only rate cuts as the “policy-mistake-in-the-making” crowd would have it," says Pozsar.

He notes for decades central banks have been tasked with a redistribution from labour to capital.

"Maybe it’s time to go the other way next. What to curb? Wage growth? Or stock prices? What would Paul Volcker do?" asks Pozsar.