Image © Adobe Images

J. Safra Sarasin says the Swiss National Bank (SNB) should lower its policy rate in March, independent of the signals that the European Central Bank (ECB) will send at its meeting this week.

The call from the Swiss private bank is made in the context of March 04's soft Swiss inflation print, below-potential growth forecasts, deteriorations in the labour market, and the real appreciation of the Swiss franc, which together justify a rate cut to support the economy.

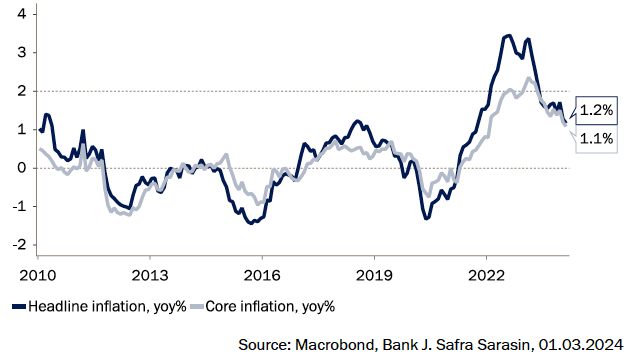

Swiss inflation fell in February to its lowest level in nearly two and half years, fuelling expectations that the SNB could cut interest rates later this month.

Consumer prices rose by 1.2% compared with a year earlier, a deceleration from the 1.3% rate in January, albeit slightly higher than the 1.1% forecast in a Reuters poll.

Above: Inflation fell further in February.

"Given the favourable inflation outlook, the strong Swiss franc, falling wage expectations and the current restrictive monetary stance of the SNB, we believe that a rate cut in March is justified," says Dr. Karsten Junius, Chief Economist at J. Safra Sarasin.

If the SNB does indeed cut interest rates in March, the Swiss franc would likely face further devaluation pressures, as it would front-run the ECB and other central banks by several months. The ECB, Bank of England, and Federal Reserve are all tipped to cut rates for the first time in June.

J. Safra Sarasin sees several reasons why the SNB should cut interest rates in March:

Below-Potential Growth: The Swiss economy's growth has been slightly below potential, which indicates that the output gap should be closed. However, while showing slight improvements, forward-looking indicators still point to moderate growth. This scenario suggests that an accommodative monetary policy could stimulate economic activity.

Deterioration in the Labour Market: The unemployment rate has increased from a very low level, with job losses concentrated in the manufacturing sector. This indicates stress in certain parts of the economy, which a rate cut could help mitigate by lowering borrowing costs and encouraging investment and consumption.

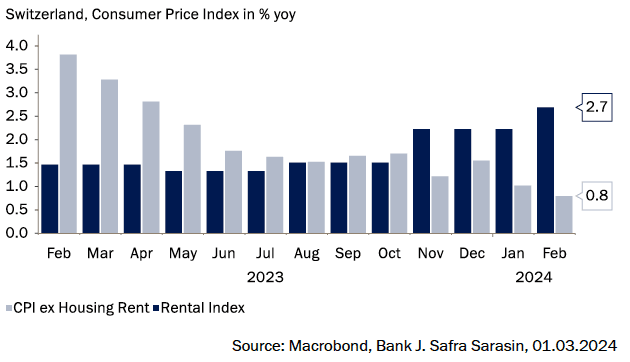

Above: When rents are stripped out, inflation is clearly trending lower.

Real Appreciation of the Swiss Franc: The Swiss franc remains highly valued in real terms, exerting pressure on the globally exposed manufacturing sector. Although the real appreciation is unlikely to continue, its past impact justifies a monetary response to support exports and manufacturing.

Falling Wage Expectations: Wage expectations are falling across all sectors and are in line with the inflation target. Lower wage pressures contribute to a favourable inflation outlook, providing the SNB with room to cut rates without stoking inflationary pressures.

Restrictive Monetary Stance: The current monetary policy stance of the SNB is deemed restrictive, especially considering the strong Swiss franc and falling wage expectations. A rate cut would be a move towards a more accommodative stance, supporting economic activity without jeopardising price stability.

Rents and Inflation: Although rents are expected to increase in May again due to a previous increase in the mortgage reference rate, the overall inflationary pressures are considered balanced, with consumer prices excluding rents increasing only slightly. This suggests that a rate cut would not lead to significant inflationary risks but would instead help address the temporary factors affecting inflation.