"The divergence between yield differentials and the currency pair offers a good risk reward to buy EUR-CHF" - HSBC.

Image © SNB

The Swiss Franc outperformed in the penultimate session of the week amid reports of hawkish comments from Swiss National Bank (SNB) Chairman Thomas Jordan but its latest gains are stoking an already high valuation and a potential vulnerability due to a moderation of inflation now underway in Switzerland.

Switzerland's Franc rose against almost all comparable counterparts on Thursday with the only exceptions being the South African Rand and Norwegian Krone as the market appeared to interpret reported remarks of Chairman Thomas Jordan as having hawkish implications for the Swiss National Bank interest rate outlook.

He reportedly told a conference that Switzerland's interest rate is "relatively low" and its inflation has been "more persistent" than expected but the Franc's subsequent rally will have further swollen an already wholesome valuation and there are also reasons to doubt whether the SNB's interest rate will really rise much further after all.

"The SNB is widely expected to raise the policy rate by 25bp to 1.75% on 22 June," says Chris Turner, global head of markets and regional head of research for UK & CEE at ING.

"Recent CPI releases have, though, shown core inflation dipping below 2.0% - a move that reduces the need for the SNB to drive the nominal Swiss franc stronger," he adds.

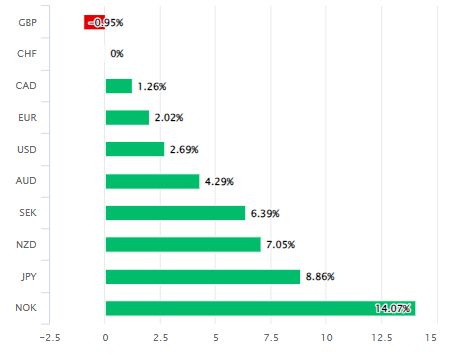

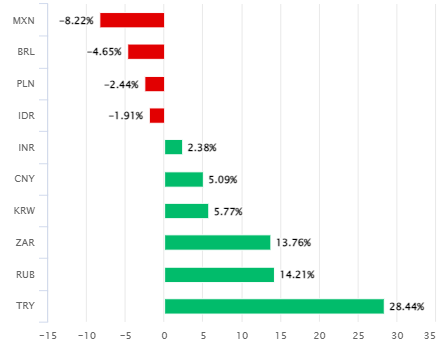

Above: Swiss Franc performance relative to G10 and G20 currencies in 2023. Source: Pound Sterling Live.

Switzerland's Franc has long followed an ascendant trajectory against many other currencies and often to the chagrin of the Swiss National Bank but policymakers have welcomed and even encouraged its appreciation ever since inflation surged above the price stability level following last year's invasion of Ukraine.

Market demand for the Franc has been supplemented by SNB sales of Dollars, Euros, Pounds, Canadian Dollars and other currencies from the reserve portfolio built up through efforts to hold down the Swiss exchange rates during the years after the European sovereign debt crisis.

The effect of this has lifted the SNB's trade-weighted measure of the overall Swiss Franc to new record highs in the last year while raising the real or inflation-adjusted measure of the trade-weighted currency to its strongest level since the onset of the pandemic.

Strong and broad appreciation has led import prices to cheapen and to, theoretically, more than offset recent increases in inflation but this has also left the Franc appearing to be 'overvalued' however it's measured, while the latest inflation developments are potentially an emerging vulnerability for the currency.

"We have long been of the view that the CHF was one of the more overvalued G10 currencies," says Dominic Bunning, European head of FX research at HSBC.

"We now believe the timing is right for these forces to create more negative momentum for the CHF," he told clients on Thursday while tipping EUR/CHF as a buy.

Above: Pound to Swiss Franc exchange rate shown at daily intervals alongside USD/CHF and EUR/CHF.

Bunning and the HSBC team say a less bleak outlook for the global economy, ebbing inflation in many parts of the world and larger increases for interest rates in lots of other countries are all reasons for why the Swiss Franc itself could be likely to deflate against counterpart currencies in the near future.

Deflation of the Franc might have become even more likely following the release of Swiss inflation figures on Monday this week, which confirmed the annual pace of price growth dipped from 2.6% to 2.2% in May while also suggesting the core inflation rate fell back below the 2% target last month.

This means financial markets are potentially being overly optimistic when expecting additional increases to lift the SNB's interest rate from 1.25% to 2% by year-end, and if that turns out to be the case then Swiss Franc exchange rates might be likely to adjust lower over the remainder of the year.

"The 2y swap rate differential between the EUR and CHF has widened out again in recent weeks. This can be supported by a still hawkish ECB through the summer, while the SNB is likely to be much closer to the end of its hiking cycle," Bunning says.

"The divergence between yield differentials and the currency pair offers a good risk reward to buy EUR-CHF," he adds.

Above: EUR/CHF shown at weekly intervals alongside spread or gap between 02-year German and Swiss government bond yields. Click for closer inspection.