The short-term uptrend in GBP/CAD is likely to reach the December 1 highs eventually.

The Pound-to-Canadian Dollar exchange rate is in a strong, short-term, uptrend ever since it found support and rotated at the 200-day moving average (MA) on January 8.

Since then we have had ten up days in a row, which is quite a rare phenomenon, and there is now a fairly high chance this uptrend could slow down and we will start to get some down days.

"GBPCAD’s rally appears to be stalling above 1.7250 resistance. Momentum indicators are bullish however they are showing signs of exhaustion and DMI’s are converging in a manner that hints to a shift in the balance of risk," says Shaun Osborne, an analyst with Scotiabank.

Nevertheless, our studies are inclined to suggest that in the absence of any bearish signs, and considering financial markets have a propensity to extend to extremes more than other data sets, the short-term uptrend must be considered intact and expected to continue.

A rise, therefore, above the 1.7347 highs would confirm an extension to a target at December 1 highs of 1.7475.

At the December 1 highs, there is an increased chance the uptrend may stall and pull-back since there is likely to be an increase in selling at that level from traders anticipating a correction and betting as such.

This is therefore our key short-term target.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Data and Events for the Canadian Dollar

From a data perspective, the main release in the week ahead is Canadian inflation data (CPI) for December, out on Friday, which has the potential to impact on interest rate expectations, and from there the value of the Canadian Dollar (Loonie).

Higher inflation equals higher interest rates which equal a stronger Loonie as it attracts more foreign capital drawn by the promise of higher returns.

The results, however, are expected to be softer than the previous months because of the unexpectedly strong data released then.

"Canadian retail sales and consumer prices are due for release next week - softer numbers are expected after last month's strong gains," says BK Asset Management Managing Director Kathy Lien.

Offical market estimates expect headline CPI, which is out at 13.30 GMT to come out at 1.9% from 2.1% previously, whilst month-on-month they forecast it to fall -0.3% after it gained 0.3% in November.

Core CPI, which misses out volatile and seasonal items such as fuel and food, is forecast to come at 1.5% in December from 1.3% previously.

The other main release for the Canadian Dollar is Retail Sales for November, which is out on Thursday at 13.30.

Headline Retail Sales are forecast to rise 6.2% in November by data website tradingeconomics.com compared to a year ago, after rising 6.7% in October, but they are expected to rise at a slower 0.7% month-on-month compared to the 1.5% increase in October.

Data and Events for the Pound

The two big releases for the Pound next week are Employment data and fourth quarter GDP.

Employment data for November is out on Wednesday at 9.30 GMT and is forecast to show the unemployment rate staying fixed at 17-year lows of 4.3%.

Wages are also likely to be in focus as they influence inflation which in turn influences interest rates and Sterling.

Higher wages, equal higher inflation, equals higher interest rates, equals higher Pound.

Wages rose by 2.5% in the previous month of October compared to a year ago and are expected to rise the same in November.

Unfortunately for workers, this is a half a percent below inflation at 3.0%, which means they are essentially getting poorer.

This suggests consumption may fall as people tighten their belts which will reduce growth.

Evidence of wages rising in December, however, from a new survey conducted by IHS Markit suggests a possibility of an upside surprise in Wednesday's earnings data, although the official data will be for the month before the IHS Markit data.

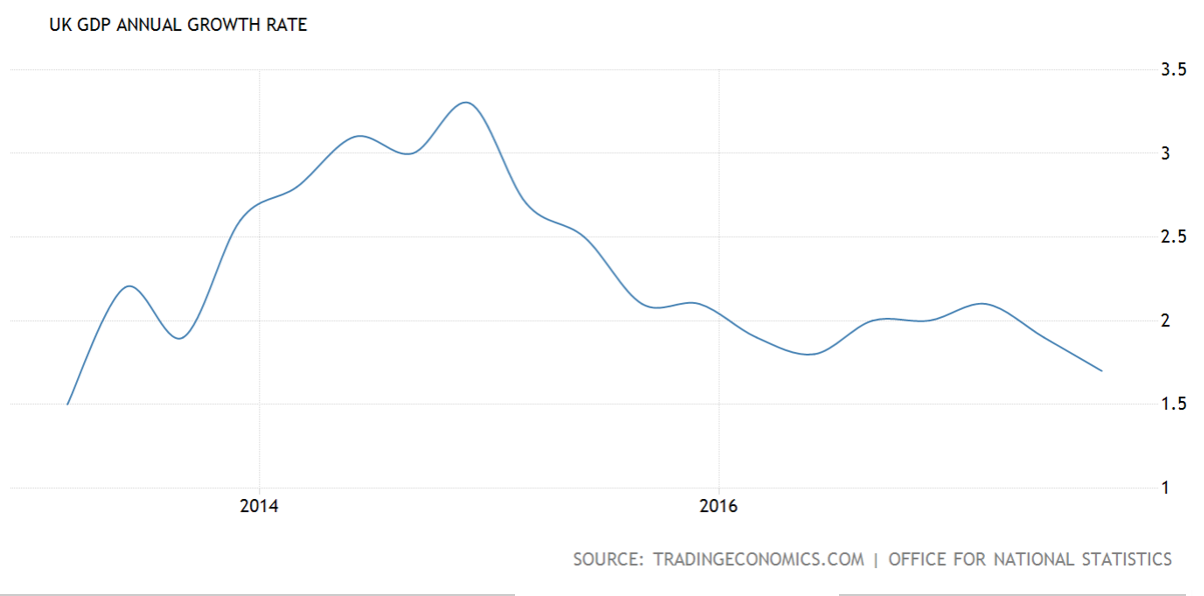

The other major release in the week ahead is Q4 GDP on Friday at 9.30.

Consensus estimates are for GDP to equal 1.4% in Q4 from 1.7% in Q3 reflecting the slowdown in the economy due to the corrosive effects of high inflation and businesses holding back from making investment decisions due to Brexit uncertainty.

A fall to the estimated 1.4% would mean the annual growth rate on a quarterly interval comparison basis will have fallen to lows not seen since 2009 - over eight years ago during the financial crisis.

(Image courtesy of tradingeconomics.com)

The quarterly rate, however, is forecast to remain at 0.4% like Q3, and the year-on-year data may reflect a more negative situation than the quarterly figures suggest.

The economy has shown and will continue to show resilience when GDP data is released, says IHS Markit Economist Bernard Aw.

"Preliminary estimates of UK GDP for the fourth quarter are eagerly awaited for confirmation that the economy continues to show resilience on the face of Brexit uncertainty," says Aw.

From a growth perspective, the outlook may be improving after recent conciliatory comments from French President Emmanuel Macron and other leading EU figures suggested the UK could have a bespoke trade deal after Brexit, and consequently a softer-landing for the UK economy.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.