The Canadian Dollar shot higher on news Canadian retail sales comfortably beat expectations.

Canadian Retail Trade data showed retail sales rose by 2.2% compared to the month before and easily beat expectations of 1.1%.

Core retail sales, which do not include volatile food and fuel components, rose by 1.7%, also overshooting forecasts of 1.1%.

Both rose from the -0.4% and -0.5% recorded in December respectively.

The Canadian Dollar soared on the release of the data, rising to 1.3283 Canadian Dollar to US at the time of writing from 1.3318 previously as traders bet that the Bank of Canada might have to adopt a more constructive view of the economy going forward.

The Pound to Canadian Dollar exchange rate fell to 1.6544 from a pre-release level of 1.6578.

The US Dollar to Canadian Dollar exchange rate fell to a daily low at 1.3263 from a high of 1.3365 ahead of the release.

The rise in spending is expected to contribute to a bumper first quarter for the Canadian economy, with GDP rising by an extraordinary 3.0% according to some forecasts.

“Given what we already know about other sectors in January (manufacturing/wholesale trade), we’re likely headed for 0.4%-0.5% gain in monthly GDP, setting us up for a 3%-plus Q1,” says Nick Exarhos at CIBC Economics.

The rebound in retail sales was based on a combination of stronger ocil prices pushing up the price of petrol and an increase in core sales due to the unduly weak December data notes an analysis released by TD Securities.

Stronger Canadian Dollar

Following the release the Canadian Dollar continued its young uptrend versus the Dollar, which began after last week’s disappointing meeting of the US Federal Reserve.

The improving economic data in Canada could be due to the influence of the strengthening economy of the US, its largest neighbour.

Historically this has tended to rub off considerably on Canada.

This is the thinking behind those who forecast a stronger Canadian Dollar in 2017, such as Marshall Gittler at FXPrimus who gave his main reason the cross-border influence from greater US growth.

Offset against this is recent weakness in the price of oil which remains highly correlated to the Canadian Dollar, especially with regards to the USD/CAD exchange rate.

Oil Glut to Weigh on the Canadian Dollar

The fall in oil prices has been late in coming argues Aurelija Augulyte at Nordea Markets who has noted a massive overhang for some time.

“Yes, the Markets finally realise the downside risks to oil. And while I did mention the huge supply overhang many times, I think the trigger for continued downside will be a slowdown in global demand. See oil in the context of e.g. industrial metal prices – very much similar dynamics lately,” says Agulyte in a note to clients.

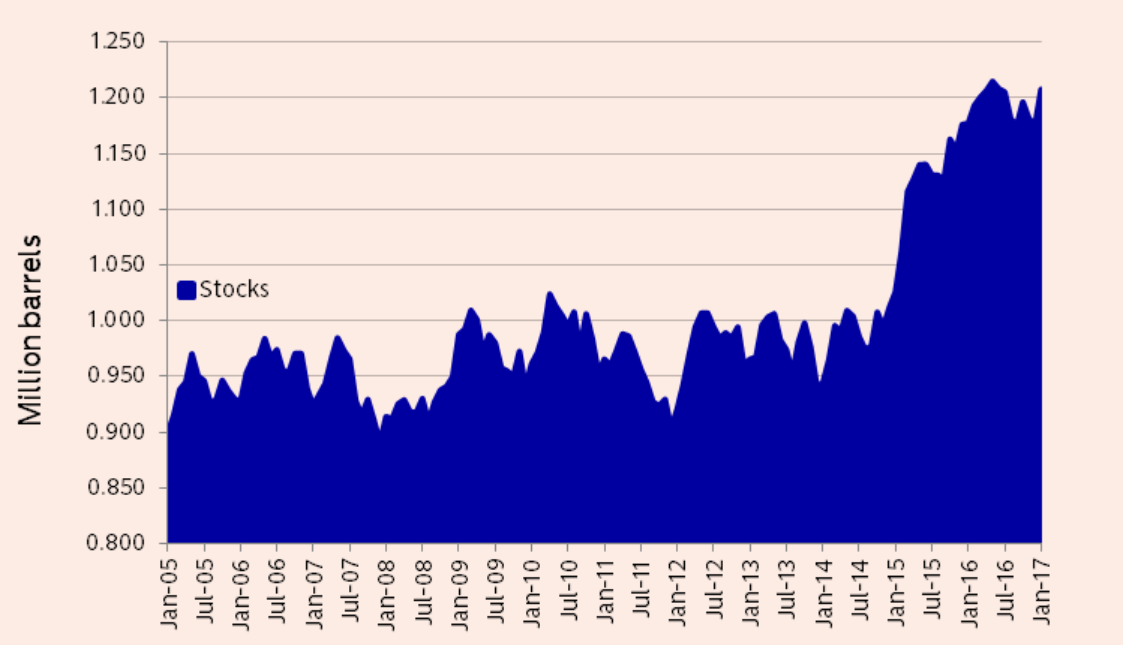

In a seperate note, her colleague Thina Margrethe Saltvedt also notes the massive overhang in oil stocks:

Saltvedt argues that the current fall in demand for oil which is responsible for the increase in inventory is only a temporary seasonal factor due to refineries closing for maintenance in the early spring and therefore demand for cured falling.

The large increase in production in non-OPEC countries such as Canada and the US has also contributed to the overhang.

Another is as a result of the sharp increase in OPEC production which occurred just before the decision to cap supply came into force.

OPEC needs to be vigilant in complying to its commitments to cut production to keep prices stable.

“OPEC maintained a historically high compliance rate in February at 98% – down from 135% according to the IEA. The sharp fall in oil prices by more than 8% over the last two weeks shows the pressure on OPEC to maintain compliance going forward. Global inventories need to come down to normal levels to support oil prices at USD 55/barrel and higher,” said Saltvedt.

The analyst sees “Major Headwinds Ahead” for Oil and a material chance of a fall back to the 45-50 Dollars per barrel range seen before the OPEC agreement.

At that level Shale oil would once again become too expensive to pump.

Yet any hope from OPEC that this will lead to closures of Shale wells may be misplaced as this time round Shale operators have hedged against a fall in oil prices using futures contracts which lock in a selling price above the breakeven rate.

Saltvedt also notes how banks are now also extending credit lines to Shale producers for the first time, for investment in exploration and R&D, showing greater longevity for the sector.

Despite these headwinds she notes a strong possibility of a rebound in oil prices at the end of Spring when seasonal factors dampening prices now fade, and the pre- OPEC deal glut disperses.