“By front-loading the increase in interest rates we are trying to avoid the need for even higher interest rates further down the road. As I’ve stressed a couple of times, frontloaded tightening cycles tend to be associated with softer landings and our objective is to get inflation back to target with a soft landing,” - Bank of Canada Governor Tiff Macklem

Image © Adobe Stock

The Canadian Dollar has been volatile with the Loonie whipsawing almost wildly since the Bank of Canada (BoC) shocked the market with its largest interest rate rise since 1998, throwing a curveball at investors and prompting a range of responses from analysts, a selection of which is included below.

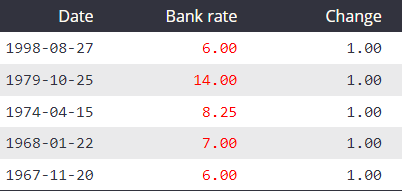

Canadian Dollar volatility had all but disappeared in the weeks after the BoC’s second 50 basis point increase in the cash rate back in June but it returned with a bang on Wednesday this week while persisting through Thursday after the bank lifted its cash rate by 100 basis points to 2.5%.

That was only the fifth time in all of Canada’s history that the cash rate has been raised by 1% in a singular sitting and, although the last occasion was back in 1998, the vast majority of these abnormally large steps were only seen during the bleak decade that spanned the years 1969 to 1979.

Source: Bank of Canada.

Wednesday’s move took the cash rate to its highest level since the collapse of Lehman Brothers and crescendo of the global financial crisis in late 2008 but could yet be followed by further steps of variable size during the months ahead, with much now to be determined by the Canadian economy.

“There are really three important reasons for this unusually large step today. First of all inflation is increasing, it’s broadening and it’s persisting. Second, the economy is overheated. What started as global inflation from higher energy, higher global goods prices is broadening here in Canada and it’s broadening because the economy is overheated,” BoC Governor Tiff Macklem said in Wednesday’s press conference.

Source: Bank of Canada.

“And the third reason, as I’ve already stressed, is our desire to front-load our interest rate response. By front-loading the increase in interest rates we are trying to avoid the need for even higher interest rates further down the road. As I’ve stressed a couple of times, frontloaded tightening cycles tend to be associated with softer landings and our objective is to get inflation back to target with a soft landing,” the governor also said.

In the same sitting the BoC cut its forecasts for Canadian economic growth in 2022, 2023 and 2024 to 3.5%, 1.75%, and 2.25% in reflection of downgrades from 4.5%, 3.25% and 2.5% respectively, while warning that inflation will be “substantially higher” than was previously thought likely.

The BoC’s inflation forecasts were unveiled in the July Monetary Policy Report and envisage a 2022 inflation rate of 7.2% that falls to 4.6% in 2023 and 2.3% in 2024, which would leave it sitting a tad above the bank’s 2% target level.

Above: Pound to Canadian Dollar rate shown at hourly intervals alongside USD/CAD. Click image for closer inspection.

Above: Pound to Canadian Dollar rate shown at hourly intervals alongside USD/CAD. Click image for closer inspection.

Underlying Wednesday’s decision and the three reasons given by Governor Macklem is a concern at the Bank of Canada about the risk of above-target levels of inflation becoming entrenched in the economy.

That would be mission failure for a central bank that is, like a large majority of others, charged with using its interest rate to manage or otherwise contain price growth within predefined parameters.

Wednesday’s policy step has been followed by volatile trading in Canadian Dollar exchange rates and prompted a wide array of responses from analysts and economists, some of which are set out in part below.

Greg Anderson, global head of FX strategy, BMO Capital Markets

“The BoC's dramatic 100bp rate hike hasn't buoyed CAD. Nor did high oil prices earlier this year. USDCAD is presently trading at its high since November 2020. This high in USDCAD is largely a reflection of USD strength

“As demonstrated yesterday, the Bank of Canada will continue to at least keep pace with the Fed. Yesterday's 100bp rate hike has brought the BoC's base rate to 2.50%. BMO's economics team now forecasts that the BoC will get its base rate to 3.50% by the end of this year. This would put the BoC at or near the forefront of G10 central banks on rate hikes.”

“We view Canada's combination of monetary, balance of payments, economic growth, and political fundamentals as the best in the G10. Canada's fundamentals seem equal or superior to the US's along all those lines. However, when the USD is surging, currency correlations rise dramatically, and CAD just becomes one element of the basket that the USD steamrolls, regardless of its fundamentals.”

Bipan Rai, North American head of FX strategy, CIBC Capital Markets

"Just an incredible move in USD/CAD so far today. Now this isn’t something you’d expect a day after the BoC hiked by 100bps, but it’s important to note that this isn’t a CAD-specific story...The break above 1.3177/80 feels legitimate and now opens the way for a test of the 1.3340/50 mark."

“I still like staying long USD/CAD, and I don’t see a reason to deviate yet. Not least as the macro picture in the US is in-line, or slightly worse, than it is in Canada. Remember that FX is a relative game, and that US CPI number this morning was incredibly ugly.”

“I can’t imagine a macro environment whereby the Fed doesn’t match that, or stay in the hiking game longer. That’s the important bit for USD/CAD and we still envisage the pair tracking slightly above 1.30 in the months to come.”

“Note the emphasis on ‘front-loading’, and that Macklem was clear that the terminal rate is ‘slightly’ above neutral.”

“Within the Monetary Policy Report, note the revisions lower to growth for 2023 and why. Indeed, the bank is stressing considerable headwinds to consumption/housing in the period ahead. In fact, this is already showing up due to higher prices/rates.”

“I know it’s tough, but look past the shock of today’s move. Today’s actions and communication from the Bank is really about a more truncated rate hike cycle than a higher terminal. To put it bluntly - it’s terminal faster, not terminal higher.”

Taylor Schleich, director, National Bank Financial (NBF) Economics and Strategy

“Macklem’s comments suggest the high watermark for the overnight rate might be in the low-to-mid 3% range. However, economic and inflation forecasts in the Bank’s MPR are not consistent with that, in our view. To us, nearly-2% real GDP growth in 2023 does little to reduce excess demand.”

“An inflation projection of 4.6% in 2023 (3.2% Q4/Q4) doesn’t suggest that the Bank will have room to stop hiking at a barely restrictive level.”

“From our perspective, we’re looking for a far more tepid inflation outlook next year and we’re also expecting slower growth than the Bank is projecting. Our economic/inflation outlook is far more consistent with the Bank tapping out in the low-to-mid 3% range than the outlook laid out in the MPR.”

Shaun Osborne, chief FX strategist, Scotiabank

“The sharp jump in domestic rates will doubtless prompt concerns that the Canadian economy, which is particularly highly geared to the housing sector, is poised to slow sharply now (accentuating domestic rumblings about a recession).”

“Tight labour markets, strong commodity prices and high domestic savings are counterpoints the Bank offered against the sharp slowdown scenario.”

“This augurs positively for the CAD in broader terms. On the other hand, front-loading rates now brings the potential peak in the rate cycle closer.”

“The bottom line for the CAD for us is that the BoC’s tightening should support the CAD broadly—particularly against the likes of the EUR, GBP and JPY where policy tightening will lag.”

“Against the USD, more CAD-favourable short-term yield spreads should reinforce the cap on USDCAD above 1.30 and potentially launch spot towards 1.28 in the next few weeks.”

Randall Bartlett, senior director of Canadian economics, Desjardins

“It’s not easy being a central banker these days, and they’re certainly not winning any popularity contests. Inflation is red hot and household inflation expectations keep moving higher, risking further accelerating wage gains and a vicious wage-price spiral.”

“With global factors like the war in Ukraine and supply chain disruptions still keeping prices elevated, the domestic economy is bearing the burden of lowering inflation through a chilling of domestic demand. Interest-sensitive sectors like housing are bearing the brunt of the adjustment, and consumption may be next.”

“In spite of signs that the economy is slowing quickly, the Bank of Canada is being very clear in its intention to continue raising rates. So expect further tightening, as policy seems to be on a pre-set course. This will cause economic activity to come down even more rapidly than we anticipated in our recent forecast, increasing the odds of a recession in 2023.”