- GBP contained in 1.74-to-1.76 range through BoC decision.

- But could see 1.80+ in weeks ahead on BoE, UK outlook.

- Bond yields, risk appetite & BoC policy guidance in focus.

Image © Pound Sterling Live

- GBP/CAD spot rate at time of writing: 1.7534

- Bank transfer rate (indicative guide): 1.6920-1.7043

- FX specialist providers (indicative guide): 1.7271-1.7411

- More information on FX specialist rates here

The Pound-to-Canadian Dollar rate has edged above the middle of its likely short-term range ahead of Wednesday's Bank of Canada (BoC) policy decision but would still have significant upside ahead of it if Natwest Markets is right to remain bullish on an outperforming Pound Sterling for the weeks ahead.

The Pound-to-Canadian Dollar rate has recovered above the 1.75 handle thus far in the new week after coming undone alongside the U.S. bond market last week, amid a rally in oil prices that enabled the Loonie to resist the overtures of a resurgent U.S. Dollar that had been charged up by surging yields.

Oil prices have rallied after the Organization for Petroleum Exporting Countries (OPEC) extended some production curbs and production facilities in Saudi Arabia were attacked by militants, although the Pound remains the outperformer among major currencies for the year-to-date.

"The Chancellor will be throwing petrol on a growth inferno in Q2/Q3/Q4 as the UK economy is unlocked," says Paul Robson, head of G10 FX strategy EMEA at Natwest Markets. "So despite how far the currency has come, we think this is a time to be adding to long Sterling positions rather than reducing them. Our conviction levels have risen this week. We stay long Sterling versus both the EUR and CHF, and see GBP/USD trading up to 1.45 in coming weeks."

Last week's budget was more expansionary than economists anticipated and has cemented the UK's position among forecasters as a 2021 favourite for outperformance, an outlook which also explains the relatively more 'hawkish' policy stance of the Bank of England (BoE), which has noted upside risks to its inflation target for the years ahead lately and neglected to push back against speculation suggesting Bank Rate could rise as soon as next year.

"If I had to summarise the diagnosis, it’s positive but with large doses of cautionary realism," Governor Andrew Bailey told the Resolution Foundation on Monday during a speech in which he noted that the coronavirus has disrupted both supply and demand sides of the economy. "It is important to emphasise the role of the forward guidance that the MPC has adopted, and the announcements made a month ago on so-called toolbox issues."

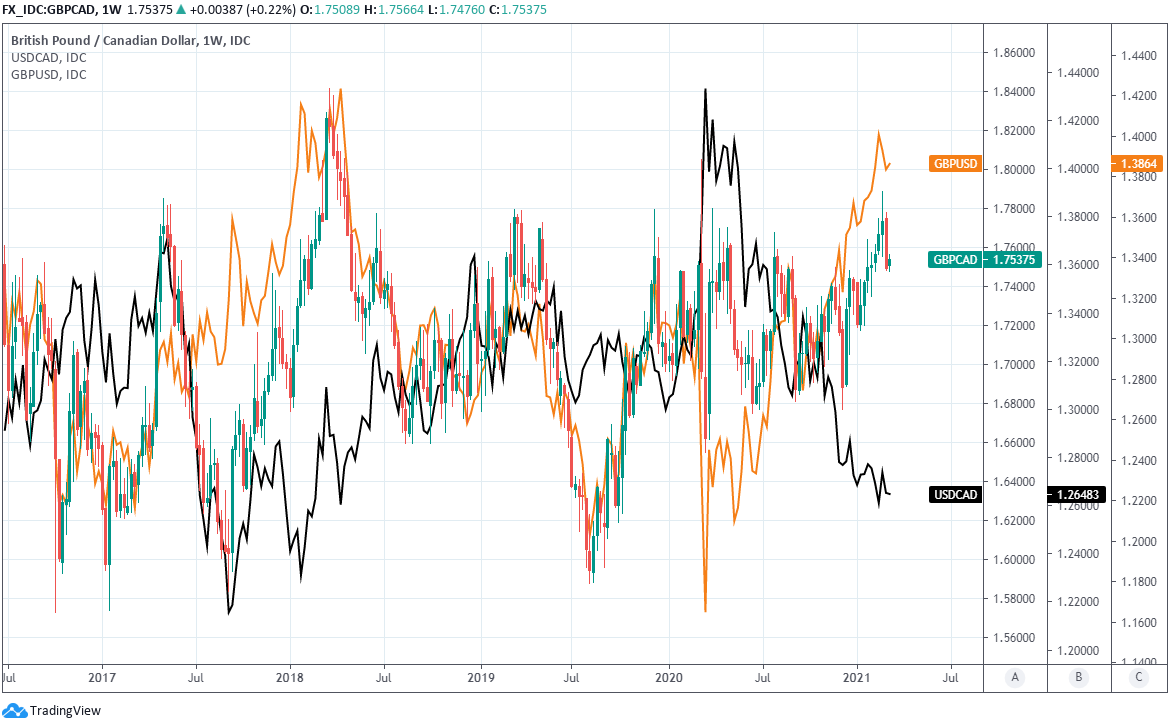

Above: Pound-to-Canadian Dollar rate shown at daily intervals GBP/USD (yellow) and USD/CAD (black).

Others including the BoC, Federal Reserve (Fed) and European Central Bank (ECB) have expressed concerns about risks to their economic recoveries as well as concerns that they could ultimately end up undershooting their inflation targets due to economic weakness. Meanwhile, the BoE's guidance is that “If the outlook for inflation weakens the Committee stands ready to take whatever additional action is necessary to achieve its remit."

This makes for a divergent policy outlook that is supportive of Sterling and explains why despite recent Canadian Dollar strength and some potentially supportive rhetoric ahead from the BoC being ahead this week. But Natwest's outlook for a GBP/USD rally to 1.45 over the coming weeks has bullish implications because even if USD/CAD falls to 1.25 in the interim, GBP/CAD would still be found trading north of 1.80 during the weeks ahead.

USD/CAD would need to fall all the way to 1.22 in order to prevent GBP/CAD rising in any market where GBP/USD is trading at 1.45. GBP/CAD is effectively an amalgamation of USD/CAD and GBP/USD so always closely reflects relative price action between the two.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

"A positive-sounding statement and better jobs data (recall the Jan number was skewed by huge part-time job losses) would be CAD-supportive," says Shaun Osborne, chief FX strategist at Scotiabank. "Our week-ahead model suggests modest downside potential for USDCAD within a wide 1.2550/1.2790 range."

In the meantime, GBP/CAD would remain above 1.74 amid any short-term Canadian Dollar strength and may even see 1.76 in response to weakness if Scotiabank is right to anticipate a range of 1.2550-to-1.2790 for USD/CAD this week. But where within that range the Loonie trades is hinged on Wednesday's Bank of Canada policy decision. The 15:00 decision is expected to see the cash rate unchanged at 0.25%, leaving the market focused on what the BoC says about its quantitative easing (QE) program.

"At its April announcement, we look for the Bank to cut its bond purchase program by $1 bn per week. Its March statement doesn’t have to give a warning about that post-April adjustment, but we can’t rule that out," says Avery Shenfeld, chief economist at CIBC Capital Markets. "Despite these coming shifts in tone, the Bank of Canada can’t afford to get too hawkish, too soon, in a short March statement that doesn’t have a fully-fledged forecast. It has to weigh its words given that bond yields have backed up a fair bit, and the market is already pricing-in outright rate hikes a bit earlier than what we’re actually likely to see."

Above: Pound-to-Canadian Dollar rate shown at weekly intervals GBP/USD (yellow) and USD/CAD (black).

The BoC said in January it'll buy bonds at this pace "until the recovery is well underway," although its gigantic footprint in the market means it'll have to cut back purchases sooner or later, or risk running out of bonds to buy, and the bank now faces having to do this amid a global surge in yields. That makes the communication of this week's decision a careful balancing act.

"We expect its share of ownership would reach 50% in the fourth quarter," says Andrew Kelvin, chief Canada strategist at TD Securities. "The BoC's best course of action is to say as little as possible. They will need to acknowledge the improving outlook, and they have no incentive to endorse recent shifts in BoC expectations. Best to emphasize uncertainty and leave all options on the table for April. The BoC matters much less for USDCAD than for CAD crosses."

The rally in yields has rocked stock and currency markets of late and results in part from investors' expectations of a global economic recovery and fears that it, combined with unprecedented levels of government fiscal support for households, will see inflation making a comeback further down the line. Quite how the BoC navigates these conditions will be an important influence on the Canadian Dollar this week with any discussion about "tapering" likely to fuel its recovery against the U.S. Dollar. That would be a short-term risk for GBP/CAD.

"The next move by the BoC will be to taper its bond purchases. At next week’s meeting, however, in the middle of a fierce bond sell-off, Governor Tiff Macklem will likely have no interest in endorsing any tapering expectations," says Francesco Pesole, a strategist at ING. "We expect the BoC message to be broadly in line with the recent Fed’s rhetoric: stressing that monetary stimulus is here to stay. This means that the market (and FX) impact should be limited, unless Macklem opts for a more alarmed rhetoric."