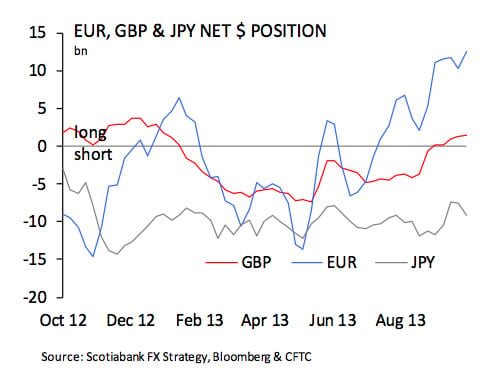

The CFTC continues catch up with unreleased reports due to the government shutdown in October; the overall message we get regarding sterling is that the situation remains mildly bullish and overextended in neither direction.

The CFTC data is widely used as an indicator as to how speculators are positioned on the currency markets. Thus, we can gauge which currencies are being tipped to rise and fall.

It also helps explain sudden moves both lower and higher when the market moves against overextended positions.

Data on speculative positioning for the weeks through October 15th and 22nd have now been released, showing that currency speculators continued to shed exposure to the USD

Net long British pound sterling (GBP) positioning rose modestly over the two weeks to 12k contracts (Oct. 15), then 14k contracts (Oct. 22).

What the below two graphs show is that GBP is maintaining an even keel without an overexposure either way; this is a good sign from a stability perspective.

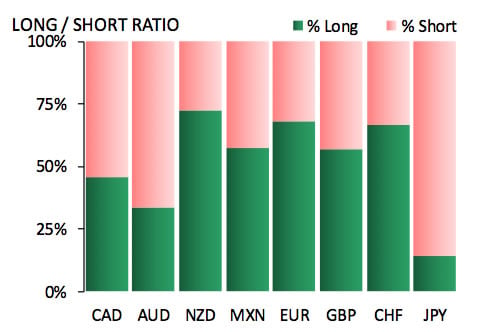

The below graphs come courtesy of Scotiabank and Bloomberg, click to enlarge.

Positioning of the majors

The large net long position in the EUR was trimmed slightly in the week through the 15th to 60k contracts (from 69k), but by the 22nd had expanded to 72k—the largest net long since May 2011.

"This reaffirms our suspicion that EUR positioning remained very one-sided through late October, a situation that has ultimately resulted in sharp long liquidation in recent days," says a note from TD Securities.

Elsewhere, JPY shorts re-emerged through the 15th and 22nd after notably shrinking earlier in the month.

As of the 22nd the net short position had expanded to 72k contracts—close to the extremes we’ve seen since the beginning of the year.

Among the commodity currencies, positioning changes were choppy, but the overall biases were unchanged.

Investors continued to prefer NZD exposure, adding to net long positions over the two weeks (12.7k on the 15th, and 13.1k on the 22nd). A

t the same time, investors remained overall more bearish on the AUD and the CAD, with AUD net shorts still quite notable at 32.2k as of the 15th and 22.1k on the 22nd.

CAD net shorts stood at 10.8k as of the 15th and 5.4k on the 22nd.

The almost neutral positioning in the CAD in the day ahead of the BoC’s dovish surprise highlights the fact that the market was caught off guard.