Image © Adobe Images

Australian dollar appreciation won't be arrested by a below-consensus inflation print.

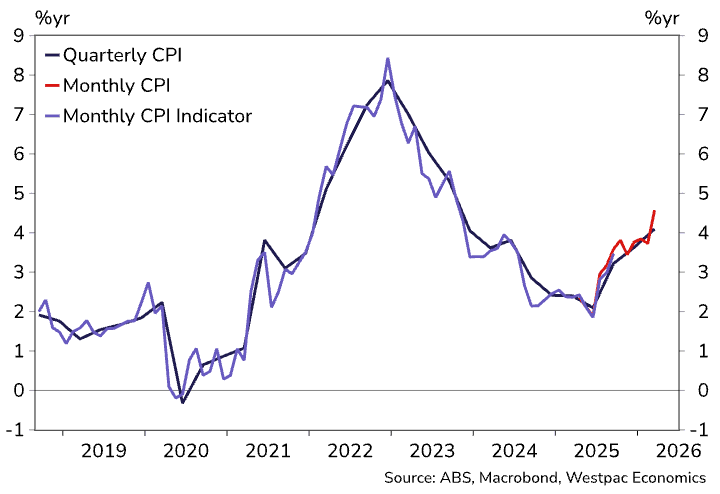

The Australian dollar is broadly softer on the day as Aussie inflation generally undershoots consensus expectations: it came in at 4.1% y/y said the ABS, whereas the market was expecting 4.2%.

Trimmed mean inflation - which is a measure of core inflation - rose 0.8% quarter-on-quarter in Q1, which is slightly less than the 0.9% the market was looking for.

So, from a purely short-term FX market take, these undershoots should weigh on the AUD: AUD/USD fell a quarter of a per cent to 0.7161, and EUR/AUD rose a similar margin to 1.6344.

The pound-Australian dollar pair rose to 1.8857 in midweek trade with a discernible lift following the data's release.

Despite the data undershooting, it sends a very strong message: Australia's inflation is running hot and the Reserve Bank of Australia (RBA) will likely respond with further rate rises.

"We continue to expect the RBA to increase interest rates by 25bp at its May meeting," says Madeline Dunk, an economist at ANZ, following today's release. "With annual growth in underlying inflation at 3.5% y/y and additional price pressures expected to come through due to higher fuel and other costs, the RBA is likely to remain cautious around the inflation outlook."

The prospect of higher interest rates in Australia should keep AUD well supported, meaning Wednesday's post-CPI currency weakness should wash out soon enough.

"The RBA has taken a hawkish stance in the face of the global energy shock," says David Forrester, FX Strategist at Crédit Agricole. "This hawkish stance has kept the AUD outperforming among the G10."

Image courtesy of Westpac.

Headline CPI gained a chunky 1.4% in the first quarter of the year, and its clear that the annual pace of headline inflation is accelerating again.

It was at a comfortable 2.1% y/y in mid-2025, rising to 3.6% by year-end and 4.1% today.

Trimmed mean, which is derived from domestic economic activity and isn't so dependent on imported factors, is where worries for the RBA lie, and why further rate rises become possible.

To be sure, Q1 trimmed mean was softer than the RBA's forecast of around 0.9% q/q from February. Momentum here is also contained: the three-month annualised rate of trimmed mean inflation is just above the RBA’s 2-3% target band at 3.2%.

"Looking ahead, the focus will be on the extent that higher fuel and other costs spillover to consumer prices more broadly," says Dunk. "While there were little signs of second order impacts flowing through to other parts of the basket, we expect that to start becoming more evident from April."

Dunk cites anecdotal evidence of rising business costs, particularly in areas like agriculture and construction, and the latest NAB business survey showed a sharp pickup in purchase costs.

ANZ are currently expecting headline inflation to peak around 5% y/y in Q2.

With data like that, it's hard to see the RBA sitting pat, and further rate rises will increase Australia's real yield advantage in the G10 and underpin ongoing Aussie dollar outperformance.

"Another hike could thereby provide further support for AUD FX, which has already performed well this spring," says a currency analyst response from Danske Bank.