- BoE's Sept. update judged 'hawkish'

- Feb. rate hike now +80% likely

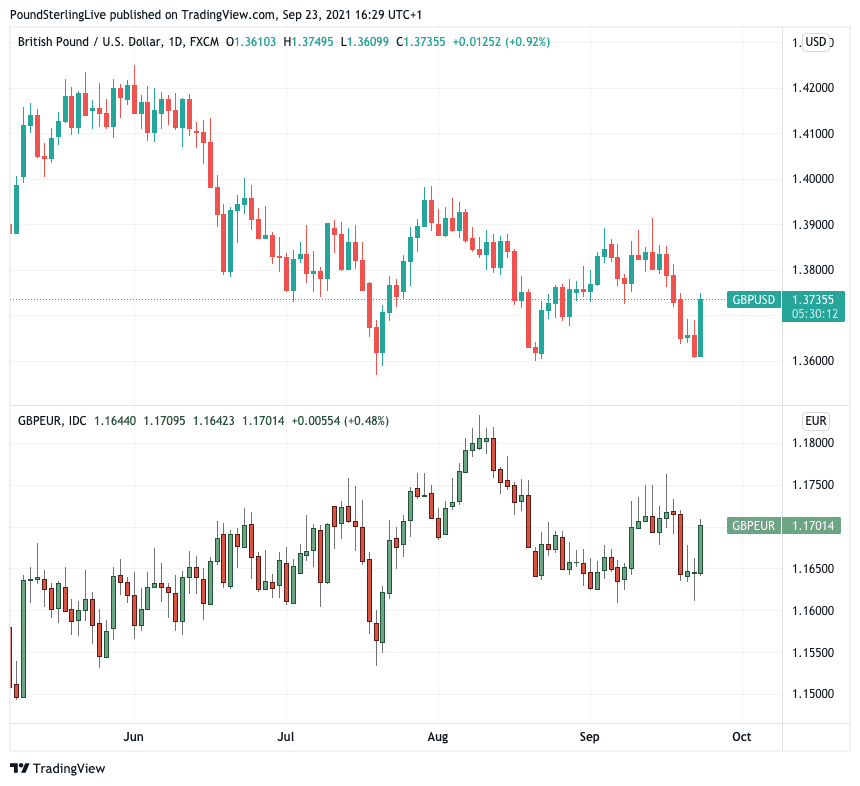

- GBP rallied in wake of update

- More gains possible say analysts

Image © Bank of England

- Market rates at publication:

GBP/EUR: 1.1687 | GBP/USD: 1.3718 - Bank transfer rates:

1.1460 | 1.3434 - Specialist transfer rates:

1.1630 | 1.3650 - Get a bank-beating exchange rate quote, here

- Set an exchange rate alert, here

The British Pound can extend its post-Bank of England rally according to analysts we follow, although 2021 highs remain some way off given its recent underperformance.

The Pound rallied against the Euro and Dollar after the Bank of England said UK inflation levels were at risk of staying at elevated levels for an uncomfortably extended period, while they consider headwinds to the economy as being temporary in nature.

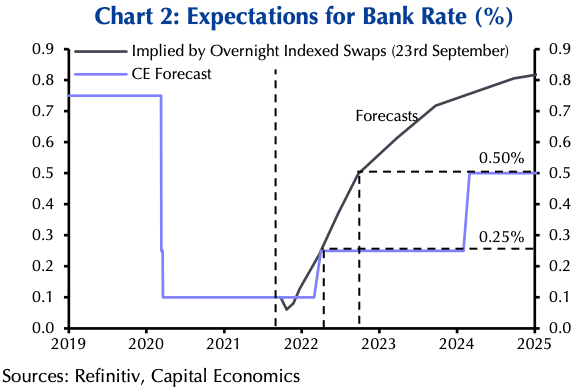

In all the Bank's September update surprised investors by being more 'hawkish' in tone than anticipated and money market pricing showed the probability of a 15 basis point hike in the Bank Rate happening in February 2022 had risen to 87%.

And a cumulative 40 basis points of hikes to 0.5% are now fully priced by September 2022.

"The details of the Bank of England policy decision were somewhat more hawkish than expected and suggest some room for near-term GBP outperformance," says Dominic Bunning, Head of European FX Research at HSBC.

The Pound-to-Euro exchange rate recovered losses sustained earlier in the week and briefly went back above 1.17 while the Pound-to-Dollar exchange rate advanced by a percent to leap the 1.37 round number.

"We now expect the Bank of England to initiate a rate hike cycle with an increase in May 2022, followed by November 2022. While the pound may be subject to some near-term uncertainties, we expect the U.K. currency to strengthen against the U.S dollar and the euro over the medium-term," says Nick Bennenbroek, International Economist at Wells Fargo Securities.

Above: GBP's post-BoE rebound in context: 2021 highs are still some way off.

"We had expected the Bank of England’s MPC to sound hawkish... and that’s what we got," says Daniel Vernazza, Chief International Economist at UniCredit Bank.

"If unemployment does not rise materially then the MPC will likely tee-up a small (15bp) rate hike as soon as February next year," he adds.

The Bank probably now has little choice to raise rates in early 2022 given the sheer weight of expectation held by the market for a February hike: disappointment could now in itself be destabilising.

Big investment bank names Citi and JP Morgan brought forward their expectations for a rate rise to early 2022 in the wake of the policy update, while Goldman Sachs did so just last week.

Consultancy Capital Economics - who have long expected a 2023 rate rise - have also folded.

"The Bank is moving closer to raising interest rates," says Ruth Gregory, Senior UK Economist at Capital Economics. "As such, we now think that rates could rise in early 2022, rather than in 2023 as we had previously thought."

Economists appear to have received the message that the Bank is concerned about price stability in the UK, i.e. an extended period of hot inflation above their mandated target of 2.0% cannot be tolerated.

"Given the gloomy tone of the recent news on economic activity, we had expected the MPC to place some weight on the downside risks to GDP growth," says Gregory.

"But while the Bank cut its Q3 GDP growth forecast by about 1%, it ultimately gave the downside risks to activity short shrift. Instead, the minutes noted the 'primacy of price stability' in the MPC’s remit and stated that 'that the inflation target applies at all times'," she adds.

Indeed, the Bank said the largest headwinds to growth were external in nature, resting in large with global supply chain constraints.

Critically therefore UK demand is not in question, as might have been the case following the 2008 financial crisis.

Therefore the risks to demand posed by a rate rise are not significant enough to overcome concerns over persistently high inflation.

"In our view, the key elements that support sterling strength are the vote on QE and the commentary around when rate hikes might start," says Bunning.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Sir Dave Ramsden joined Michael Saunders in voting to curtail gilt purchases at £840bn rather than letting it run to £875bn.

"In some respects, this is largely symbolic given it would only limit the BoE’s bond buying by a few months. But clearly it sends the signal that these two policy makers want to tighten policy settings right now," says Bunning.

Bunning says another interesting comment was the idea that tightening should occur via rate hikes even if this were to happen before asset purchases had finished.

"With QE set to run until the end of the year, this implies that is would be possible, albeit unlikely, that the Bank of England could hike rates later in 2021," says Bunning.

"Interest rate expectations have already moved forward in recent months, with hikes now implied for Q1 next year. This should support GBP for now, and any signs that these expectations might be pulled further forward would be even more bullish," he adds.

Hinesh Patel, portfolio manager at Quilter Investors says because inflation is largely being driven by external factors raising interest rates might have little impact on overall inflation levels.

But he makes an important point: the Bank of England does not exist in isolation and what the U.S. Federal Reserve and European Central Banks do matters.

"With the ECB and Federal Reserve both announcing that they intend to begin the tapering and unwind their financial support, there is a risk that not acting in the same timeline will force UK sterling down even further – exacerbating the inflationary shock further with even higher import prices," says Patel.

Indeed, the Bank cannot afford a significant devaluation of the Pound as it would only risk exacerbating externally driven inflation, therefore holding the line on a 2022 rate hike might be very necessary.

The UK is a net importer of goods and therefore a rising Pound pushes down the cost of imports and is therefore a deflationary force.

While the Bank does not officially target the Pound the MPC will be aware that now could be the worst possible moment to trigger a devaluation.