- EUR/USD risking slide back to 2021 lows near 1.1700

- Upside curbed as U.S. economy, Fed stance buoy USD

- Discouraging charts, Asian virus worries weigh on EUR

Image © Adobe Stock

- EUR/USD reference rates at publication:

- Spot: 1.1754

- Bank transfers (indicative guide): 1.1345-1.1427

- Money transfer specialist rates (indicative): 1.1650-1.1674

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Euro-to-Dollar rate entered the new week hobbled afresh and vulnerable anew to a retest of its nearby 2021 lows following signs of a renewed upturn in the U.S. economy that could have implications for Federal Reserve policy in the coming months, and as the coronavirus gathers renewed momentum in parts of Asia.

Euro-Dollar had previously been buoyed after the Fed suggested in July that a decision to taper the bank’s quantitative easing programme was likely a matter for the Autumn months, and later when data showed the Eurozone growing faster than the U.S. last quarter.

But after attempting a retest of 1.19 last Wednesday the Euro has suffered several setbacks, each of which lifted the Dollar across the board and helped push EUR/USD to 1.1760 by the opening of the new week, leaving it within arm’s reach of year-to-date lows around 1.1700.

“Although we expect the greenback to turn lower eventually, the currency may remain supported over the near-term in light of firm domestic data, uncertainty around the Fed’s taper timeline, and outbreaks of the infectious Delta variant in many parts of the world,” says Zach Pandl, co-head of global foreign exchange strategy at Goldman Sach, who forecasts a Euro-Dollar rate of 1.20 in three-months time.

Friday’s payrolls report showed the U.S. creating close to 1 million jobs for a second consecutive month and came hard on the heels of a new record high for the Institute for Supply Management services PMI, both of which hint of a renewed acceleration by the economy early in the third-quarter and could only embolden those Fed policymakers who already see economic conditions meriting tweaks to the bank’s policy settings.

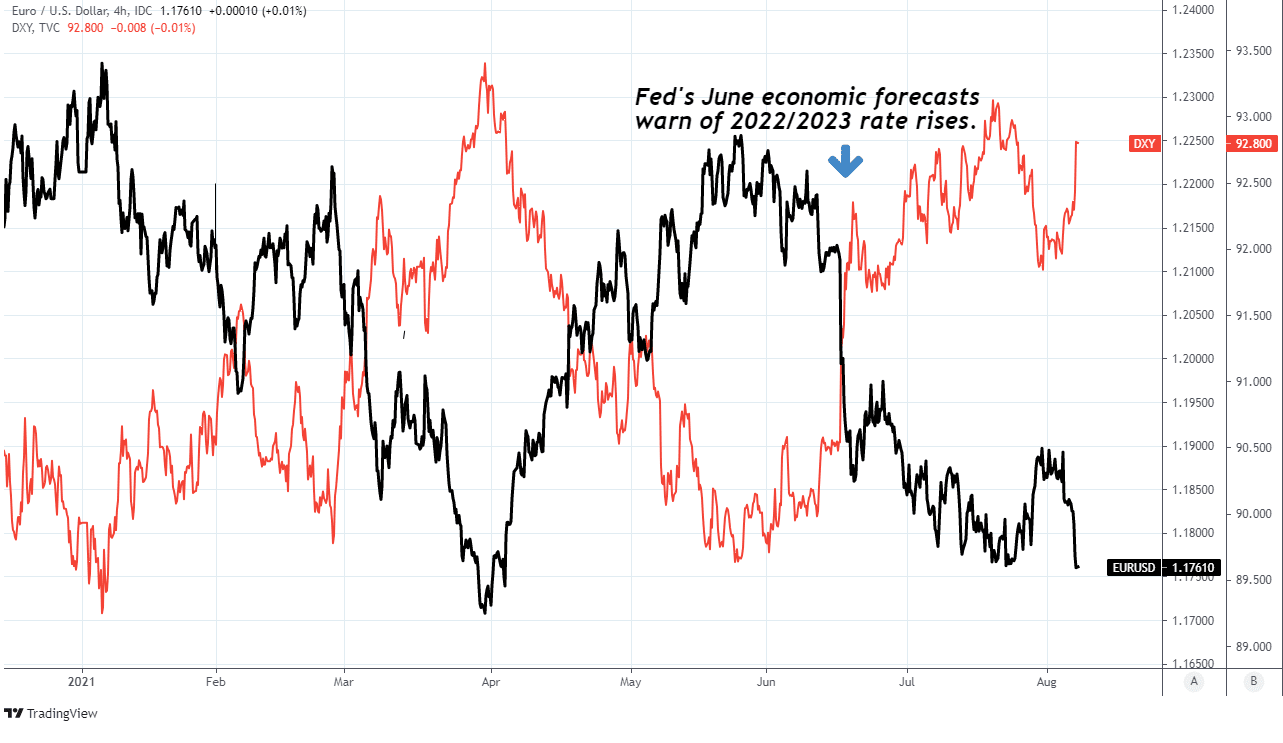

Above: Euro-Dollar rate shown at 4-hour intervals alongside U.S. Dollar Index.

The data could be a constraint on the Euro-Dollar rate for a while yet as it does little to discourage other Federal Open Market Committee members from joining Richard Clarida, vice chairman of the Fed, who said in a speech to the Peterson Institute for International Economics last Wednesday that if the economy conforms to the Fed’s June expectations then interest rates might need to rise from late 2022.

“Coming from him, as a dove, we believe the record has now been set straight for the Fed's default policies. Our interpretation of his comments is that the Fed plans to announce QE tapering in the September meeting-possibly flagging it in Jackson Hole, but with the details in the September meeting-and to start QE tapering in January next year, or at least in Q1,” says Athanasios Vamvakidis, head of FX strategy at BofA Global Research, who forecasts who forecasts a Euro-Dollar decline to 1.16 by the end of September and 1.15 by year-end.

“EURUSD is now consistent with real yield differentials. Fed and ECB policy changes this fall could determine what follows next,” Vamvakidis says.

Further strong job reports are exactly what the Fed’s Clarida and others had been waiting on before entertaining any winding down of the bank’s $120BN per month bond buying programme, although even before the data gave the bank a green light to begin packing away its crisis-fighting policy tools the Euro-Dollar rate had been struggling to sustain upward momentum whenever near the 1.19 handle.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

“The dollar appears to have re-aligned with the Fed’s hawkish pricing after having received some confirmation from the Fed Vice-Chairman Richard Clarida that the Bank is well on track to start normalising policy rates,” says Chris Turner, global head of markets and EMEA regional head of research at ING Group. “External factors should instead dictate the underlying narrative for FX.”

Turner and the ING team see many of the Fed’s pending policy changes as now already being reflected in the price of the Dollar, but cite a still-rampant coronavirus and its encroachment on Asian economies, all key trade partners of the Eurozone, as a possible weight on the single currency this week.

“The Nanjing COVID outbreak has spread to 16 provinces in China in the space of two weeks,” says Juan Chang, an economist at Barclays. “We note that the combined GDP of provinces with high risk regions (Jiangsu, Henan, and Yunnan) accounted for ~18% of China’s total GDP, versus ~10% in last winter’s outbreak (Dec 20-Feb 21) in northern China.”

The week ahead calendar is devoid of major data for the Eurozone but renewed restrictions on activity in China are a headwind for Europe’s export sector, while the Euro will also have to contend with a discouraging technical picture on the charts as well as the prospect of another strong set of U.S. inflation numbers this Wednesday.

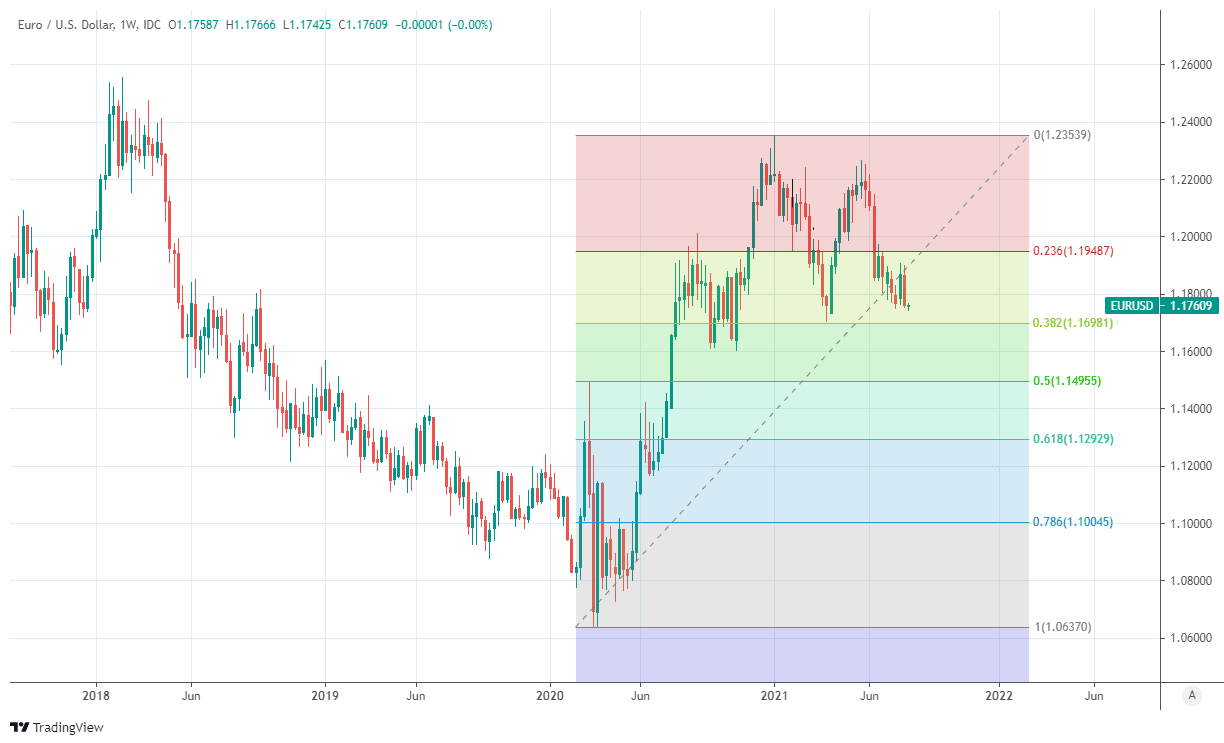

Above: Euro-Dollar rate shown at daily intervals with Fibonacci retracements of late May decline indicating possible areas of resistance.

“The market is clearly struggling to make any impression on resistance above 1.1900,” says Karen Jones, head of technical analysis for currencies, commodities and bonds at Commerzbank. “Below 1.1750 attention will revert to the September, November and March lows at 1.1704/1.1600.”

Euro-Dollar failed in repeated attempts since July’s Fed decision to recovery above 1.19 and would be sensitive this week to any further gains for U.S. inflation numbers when July’s data are released on Wednesday at 13:30, as they would merely reinforce market expectations for the Fed to announce an end of its quantitative easing programme.

“We have by the way been almost alone in calling for CLEAR upside to the actual core inflation prints since January, and we are firm that we haven’t seen the peak yet, even despite the rent of shelter tricks by the Biden administration. This means that tapering bets are still fully alive,” says Martin Enlund, chief FX strategist at Nordea Markets.

The main U.S. inflation rate has recently risen above 5% while the more refined measure of core inflation, which ignores movements in volatile energy prices and some other items that could distort underlying trends, has recently risen above 4%.

Still however, and with financial markets already close to pricing-in about as many interest rate rises as could come from the bank between now and then, it remains to be seen how much lower the divergence between the Fed and European Central Bank (ECB) will really be able to push EUR/USD.

“We think EURUSD has started to bottom out and like buying dips towards the lows near 1.1750,” says Mark McCormick, global head of FX strategy at TD Securities, who warned of a EUR/USD decline to 1.1750 ahead of Friday’s U.S. nonfarm payrolls report.