- GBP/EUR testing support as political pressure cooker enters overdrive.

- Failure at 1.1149 opens door to 1.1037 ahead of likely fall toward parity.

- Gov adviser controversy irrelevant but school rowback a blow to GBP.

- Botched lockdown exit, Brexit, trade tensions et al thoroughly bearish.

Image © Adobe Images

- GBP/EUR spot at time of writing: 1.1161

- Bank transfer rates (indicative): 1.0867-1.0946

- FX specialist rates (indicative): 1.0991-1.1058 >> More information

The Pound-to-Euro rate steadied last week but the technical outlook remains bearish on the charts and the fundamental pressure cooker that otherwise stains Sterling's prospects has gone into overdrive and threatens to produce big trouble in Little Britain during the days and weeks ahead.

Pound Sterling was relatively unchanged against the Euro last week after earlier declines were arrested by an important technical level on the charts, the 38.2% Fibonacci retracement of the March-to-May rebound around 1.1149.

However, the British currency still underperformed a solid majority of its comparable rivals while the Pound-to-Euro rate was left sat atop of that support level at the weekend close after failing to pull away from it.

"EUR/GBP continues to probe the 38.2% retracement at .8988, it is struggling to regain psychological resistance at .9000 and may need some near term consolidation ahead of further gains," says Karen Jones, head of technical analysis for currencies, commodities and bonds at Commerzbank in a Friday morning note to clients. "We view the market as having recently based."

Jones is tipping the Pound for a fall 1.1037, which is equivalent to a EUR/GBP rate of 0.9060 and implies that Friday's support level near 1.1149 will soon give way. She and her technical colleague Axel Rudolph have a bearish short as well as medium-term outlook for the Pound-to-Euro rate and forecast that it will fall back to its financial crisis low of 1.02 over the coming three weeks or so.

Commerzbank's outlook for a Pound-to-Euro fall to 1.02 implies around -8.5% downside from Sunday's opening levels and a direction of travel made more likely by recent and ongoing political developments, although an important reality is that such rates would only be available at interbank level, with those quoted to retail and SME participants likely much lower. Specialist payments firms can help squash the spread between interbank and retail rates.

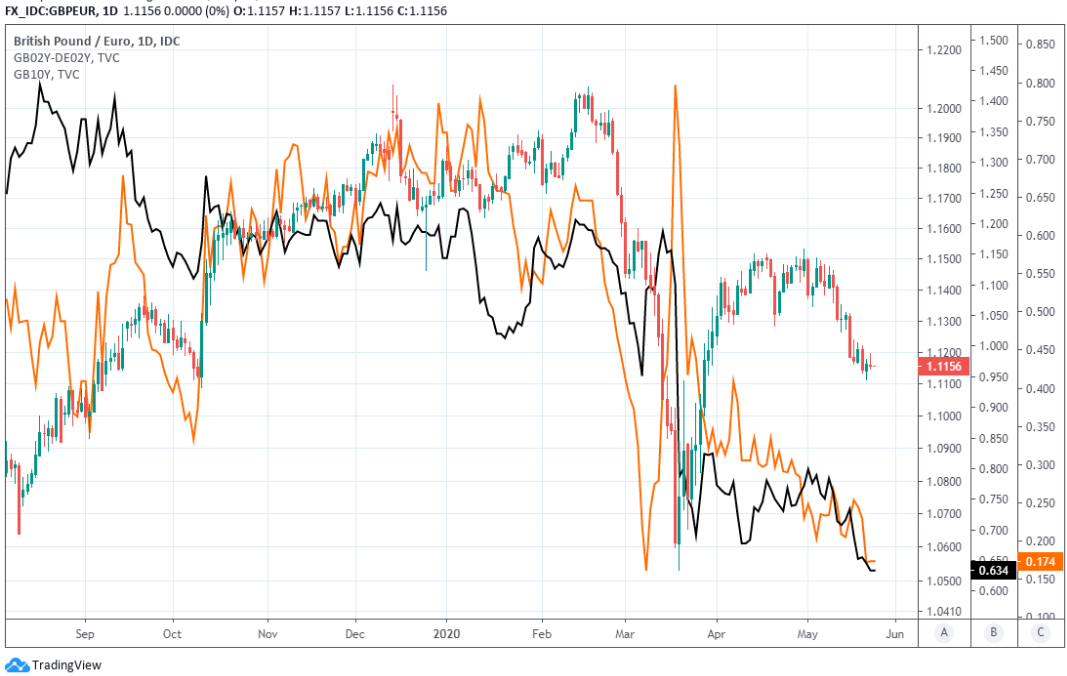

Above: Pound-to-Euro rate at daily intervals, testing 38.2% Fibonacci retracement of March-to-May rebound.

"Our quant models are overall bearish GBP on the crosses. While USD trends have started to moderate and slow down, GBP is sliding lower against all pairs in G10. GBP/NZD, GBP/SEK and GBP/NOK downtrends are robust, according to bearish Up/Down vol and Residual Skew for puts," says Vadim Iarolov, a quantitative strategist at BofA Global Research.

Each of those individual developments would have scope to weigh on Sterling even at the best of times but they're being combined together and imposed on the British currency at a point when its already testing a key technical support level on the charts that was already being tipped by analysts to give way over the coming days and weeks. Price action that takes place between 0700 and 0900 London time on Monday, which is a public holiday in the UK and U.S., will provide feedback on investors' reading of recent events and what lies ahead.

"The UK is being slower than many other countries in Europe to unwind its lockdown," says Jane Foley, a senior FX strategist at Rabobank. "This threatens to enlarge the toll on the economy which in turn places further pressure on policy makers, both fiscal and monetary. This week BoE Governor Bailey made clear that negative interest rates have not been ruled out...The combination of these factors leaves GBP very exposed."

European investors will return to their desks Monday to be greeted by much fanfare over whether one of the government's unelected advisers did or didn't flout the 'lockdown' rules. It's not the first controversy involving the government's unelected advisers although one does this time embroil somebody who's one of Downing Street's strategic masterminds on Brexit and in other areas.

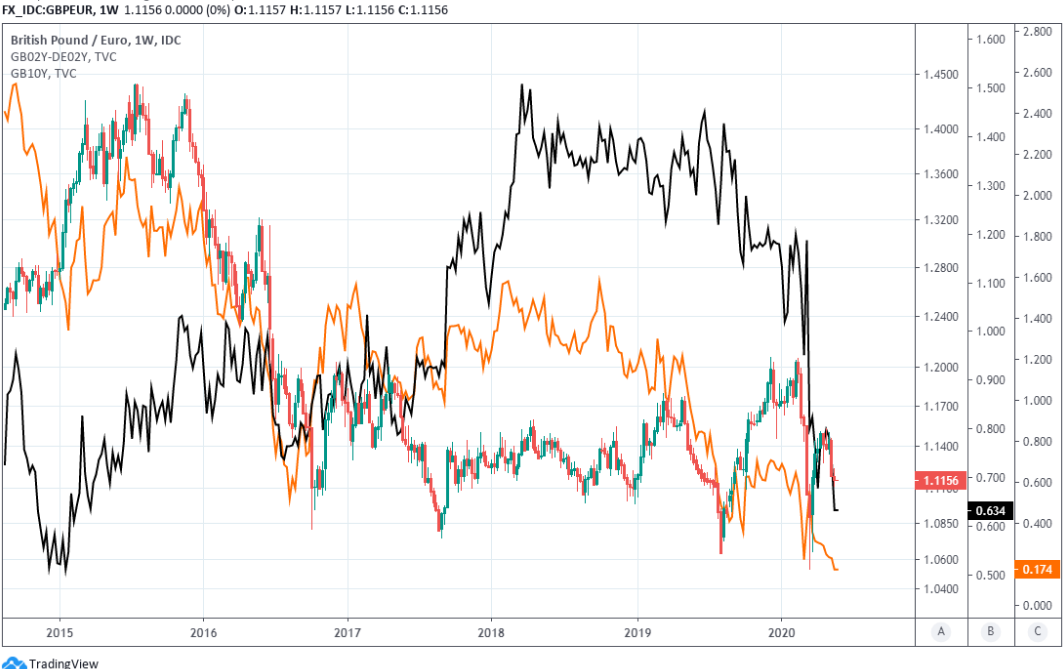

Above: Pound-to-Euro rate tests support as 10-year GB bond yield (orange) and GB-German yield spread (black).

The proverbial scalping of a government adviser does not change the electoral dynamics that ultimately govern the Prime Minister's approach toward Brexit so more important for Sterling is the latest in Britain's slowcoach exit from 'lockdown.' The government has encouraged a steady normalisation but while road traffic and usage of public parks is picking up, the public sector is in revolt and large parts of the private sector remain on furlough.

Last week saw the government water down its plan to have schools begin a staged reopening from June 01 after 13 opposition-party-dominated local councils refused to reopen their schools from next month. Government needs schools to reopen if it's to get the economy moving again but its plan did not quell widespread concerns over safety, which is now being exploited by a segment of the public sector that has long been partial to political activism, not to mention left-of-centre and largely-opposition policy.

The UK was no more than a fortnight behind France and other European countries to contract the virus and then go into 'lockdown' but finds itself at risk of falling behind in the reopening. That would truly render the UK the 'sick man of Europe,' if not the world, while arguing for a so-called U shaped GDP path for the economy rather than V-shaped recovery many initially hoped for.

A 'lockdown' that proves difficult and complex to exit would leave Pound Sterling sticking out like a sore thumb through the summer in a market where exchange rates often follow the differential between economist expectations for GDP growth on both sides of the currency equation. This would be as the Bank of England increasingly extolls the perceived merits of a negative interest rate policy, and while a 'no deal Brexit' bakes in the political pressure cooker.

"The next main hurdle for GBP should be the negative news-flow on the UK-EU trade negotiations and the likely no extension of the UK-EU transition period. As limited risk premium is priced into the GBP spot, speculative shorts not being material and the sterling implied volatility curve showing signs of complacency, the likely non-extension of the transition period and the associated negative news flow should weigh on GBP," says Francesco Pesole, a strategist at ING.

Above: GBP/EUR defies a fall in GB-DE yield differential (black) and 10-yr yield (orange) back to March lows.

The next and final round of Brexit negotiations to take place before July's deadline for extending the transition period is barely a week away so market attention could increasingly turn to the"limited progress" that's come from the talks so far. Trade discussion resume on June 01 ahead of the June 19-to19 European Council meeting that could yet see Prime Minister Boris Johnson walk away from the negotiating table, for a period at least.

The official deadline for agreeing preferential trade relations or defaulting to a relationship governed by World Trade Organization terms is December 31, although arguably the real one is July 01 because Prime Minister Boris Johnson has previously said "the Government will need to decide whether the UK’s attention should move away from negotiations and focus solely on continuing domestic preparations to exit the transition period in an orderly fashion," should sufficient progress remain absent.

Negotiator David Frost also said recently; "We very much need a change in EU approach for the next Round beginning on 1 June. In order to facilitate those discussions, we intend to make public all the UK draft legal texts during next week so that the EU's member states and interested observers can see our approach in detail." Economic sickness, negative interest rate concerns and the growing prospect of 'no deal' Brexit fears that rise as U.S.-China tensions ratchet higher is a recipe like no other for a thoroughly bearish outlook. Sterling might struggle to remain blind to the implications of this intoxicating mixture over the coming week. More so when remembering the Pound tends to diverge from the British-German bond yield differential, which fell back to March lows last week, during times of palpable Brexit risk and uncertainty.

That important bond yield differential is illustrated by the black line on the above charts and argues in favour of forecasts suggesting a fall back to financial crisis lows for the Pound-to-Euro rate. The gap between it and Sterling widened between 2018 and 2020, with the British currency trading substantially below the level implied by it for the length of time that UK trade prospects were in doubt.

Meanwhile, and over in Europe, focus will be on a European Commission proposal for a coronavirus recovery fund as well as the market response to counter-proposals from the 'frugal' Northern members, who took issue last week with the Franco-German gambit to have the commission raise €500bn from markets in the EU27's name to finance grants for financially vulnerable and virus-hit members. The so-called frugals released counter-proposals at the weekend which seek to have the commission make loans rather than grants, in addition to a two-year time limit to the programme's duration.