Image © Greg Brave, Adobe Stock

- GBP/AUD risen to major resistance level and stalled

- Will need to decisive break to forward uptrend

- GBP eyes inflation and retail sales data; Australian Dollar the RBA minutes

The Pound rose by just over 1.0% against the Aussie Dollar last week as Sterling gained on easing Brexit risks and the Aussie lost ground from continued China-US trade war tensions.

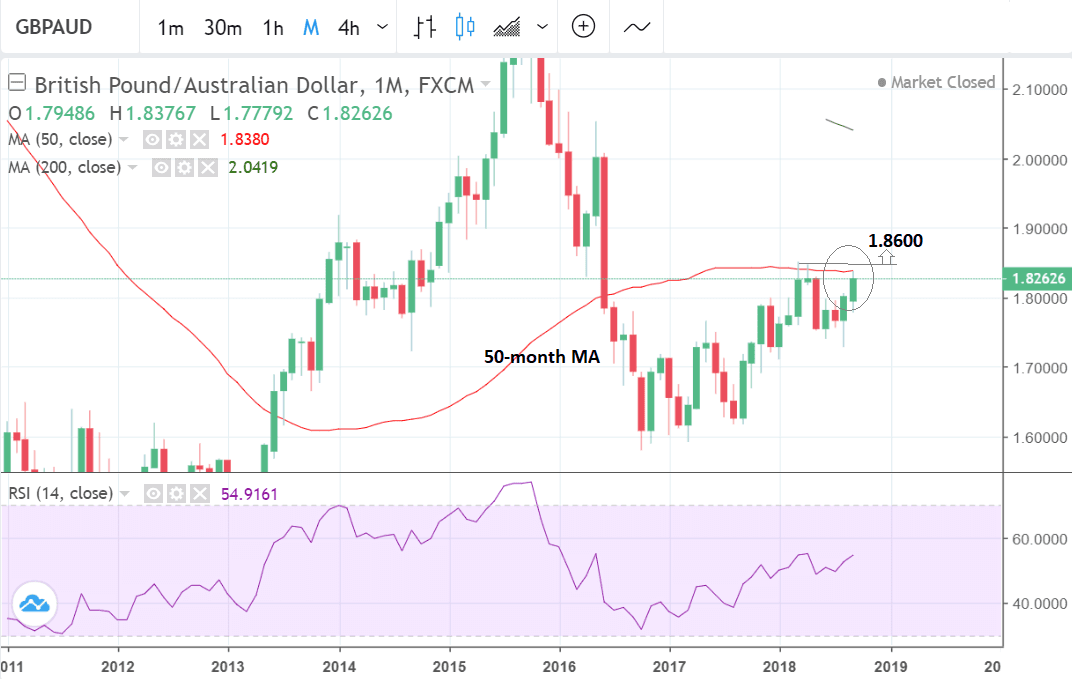

GBP/AUD peaked at a high of 1.8377 although it fell back to close the week substantially lower at 1.8263 amidst a broad-based relief rally in the Aussie.

Despite this, the short-term trend remains bullish after four up-weeks in a row but the uninterrupted series could end in the week ahead as the pair has now reached a major resistance level.

The level in question is the 50-month moving average (MA). The pair rose to retouch the 50-month MA at 1.8380 last week when it peaked only three points below at 1.8377. This strongly suggests the MA exerted a resistance effect on the exchange rate and was probably the cause of the up-move stalling.

Technical traders often target large MAs as places to fade the trend in anticipation of pull-backs in the trend and this actually often ends up causing them.

The 50-month is likely to present a major obstacle to bulls and prevent any easy gains in the near-term unless some spectacularly positive move propels the Pound higher (or the Aussie lower). One potential source could be improving Brexit negotiations even if it seems a little early to expect a complete deal yet.

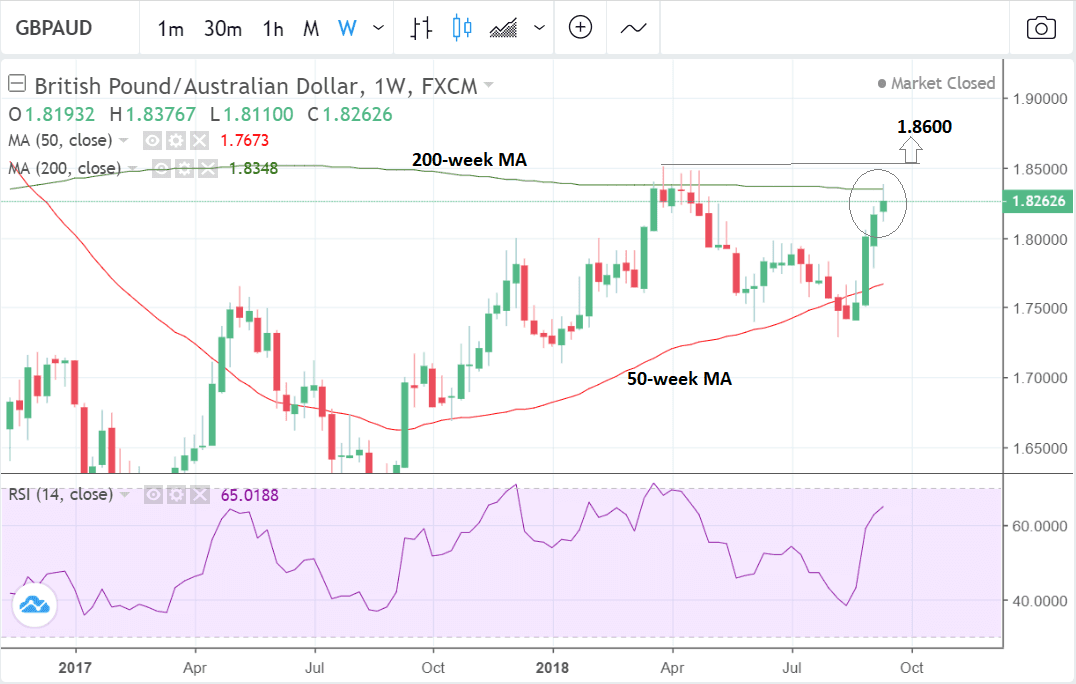

The weekly chart shows a similar picture although in place of the 50-month MA we have the 200-week MA which is obviously at a similar level given there are roughly 4 weeks to a month and the 200 week is 4 times longer than the 50 month.

Here too the exchange rate was repelled by the 200-week after rising up and touching it last week and here too the large MA is likely to present a tough obstacle to future gains.

The upshot of all this is that although the short-term uptrend remains intact and is therefore still biased to extending, the large MAs lie in the way and must first be broken through convincingly to confirm a continuation higher.

We estimate confirmation of such a breakthrough would at a minimum come from the exchange rate moving above the 1.8508 March highs. Such a move would then be expected to probably reach a target at 1.8600.

Yet even if GBP/AUD broke above that level there would still be a risk of a pull-back because the MA's in question are so large and therefore can exert a resistance effect in a wider circumference than, for example, a daily MA.

The RSI momentum indicator is at a middling level suggesting neither a positive nor negative bias to the outlook.

Advertisement

Lock in your Aussie Dollars: Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The Australian Dollar: What to Watch this Week

The Australian Dollar is currently being pushed lower by external factors but pulled higher by strong domestic data.

The external factors are deteriorating China-US trade relations - or rather the negative side effect of these on commodity prices which are Australia's life-blood.

"Although the Australian and New Zealand dollars hit fresh 2-year lows this week, both currencies rebounded on the back of stronger data. In Australia, business conditions improved and job growth strengthened and in New Zealand manufacturing activity accelerated for the first time in 4 months," says Kathy Lien, managing director and founding partner of BK Asset Management.

Turning to the week ahead, therefore, we have both the possibility of further declines due to worsening US-China news and more domestic data which could support.

It remains to be seen whether Trump will go through with slapping duties on a further $200bn of extra imports from China. Currently he is in negotiations with the Chinese again.

The public consultation ended over a week ago but resulted in no action. Next week could see something more decisive and if it is seen as negative for global growth and demand for commodities the Aussie may take another hit.

On the domestic from the main data release in the week ahead for AUD is probably the Reserve Bank of Australia (RBA) policy meeting minutes, released on Tuesday, at 2.30 B.S.T. The RBA's current monetary policy stance is neutral which means it is neither in favour of nor against raising interest rates.

If the minutes show a shift one way or another away from neutral, however, then that could impact the Aussie. If the shift is in favour of raising rates it will support the Aussie, if against, it will weigh.

The RBA are also expected to release their bulletin, on Thursday at 2.30, which should contain the most up-to-date description of their monetary policy stance, and provide further information on whether it remains neutral or not.

The Australian house price index is forecast to show a rather steep -7.0% fall in August when it is released at 2.30 on Tuesday. Such a fall is not a good sign for the economy and would probably weigh on AUD.

Finally, the Westpac Leading Index is scheduled for release on Thursday at 1.30 and RBA assistant governor Kent is to speak on Wednesday at 2.30.

The Pound: What to Watch this Week

Sterling has made a decisive recovery in September as the terms of reference of the Brexit debate have undergone a dramatic change.

Whereas previously they were somewhat polarised into the Chequers proposal on the one hand and a 'no-deal' pure Brexit on the other the gap now appears to have closed.

Now even 'die hard' Brexit purists appear to be advocating a deal based on the EU's deal with Canada - known as a 'Canada plus' deal - whilst Chequers, and even continued membership of EEA is being considered as the soft option avoiding the most economic disruption.

We heard from analysts at Nordea Markets in the week past that the Pound should actually rise under all Brexit scenarios, but expect a bloodbath if a 'no deal' arises.

The bottom line for the Pound is should the probability of a 'no-deal' continue to diminish the currency should see more gains.

"Brexit talks between the UK and the EU are expected to be stepped up in the coming days with the topic likely to dominate the informal summit of EU leaders in Austria on September 20. Sterling should therefore continue to see high volatility as it remains sensitive to Brexit headlines," says a note from forex broker XM.com.

On the hard data front, meanwhile, there are also some notable releases in the week ahead including inflation figures for August and retail sales.

Headline inflation is forecast to dip back to 2.4% in August (from 2.5%) on a year-ago comparison basis, while the core rate is predicted to fall to 1.8% from 1.9% previously (year-on-year).

Analysts are overall a bit downbeat about the prospects of economic data in the week ahead so surprises to the upside would be likely to drive the Pound higher, whilst those to the downside might weigh but to a certain extent will already be accounted for.

"Next week’s indicators may not be as positive and could fail to provide support for the pound in case the Brexit negotiations were to break down," says XM.com, "CPI figures will be watched on Wednesday for evidence that inflationary pressures in the UK continue to edge lower towards the Bank of England’s 2% target."

The other hard data release is retail sales on Thursday which is forecast to show a 0.2% month-on-month contraction in sales in August after a 0.7% bounce in July.

The overall assessment for UK data is that it remains 'sluggish' and more at risk of decline than growth.

Regardless of data no-one expects the Bank of England (BOE) to raise rates until Brexit is clarified.

Since interest rates are the main driver of foreign exchange - pushing the Pound up if they are hiked - the currency is ultimately at the mercy of Brexit negotiations rather than data, since everything hinges on the terms of divorce.

Put a different way, pure economic data is not the main consideration of when the BOE will next raise interest rates, and as such has less impact on the exchange rate. Indeed, this appears to have been the message from last week's September Bank of England policy decision.

"While inflation has started to come back down to earth and retail sales have firmed, economic growth in the U.K. has remained sluggish, with real GDP rising 1.5% annualised in Q2. Given slower economic growth and ongoing Brexit negotiations, we look for the Bank of England to remain on hold in coming quarters until these concerns subside," says a note from analysts at investment bank Wells Fargo.

Advertisement

Lock in your Aussie Dollars: Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here