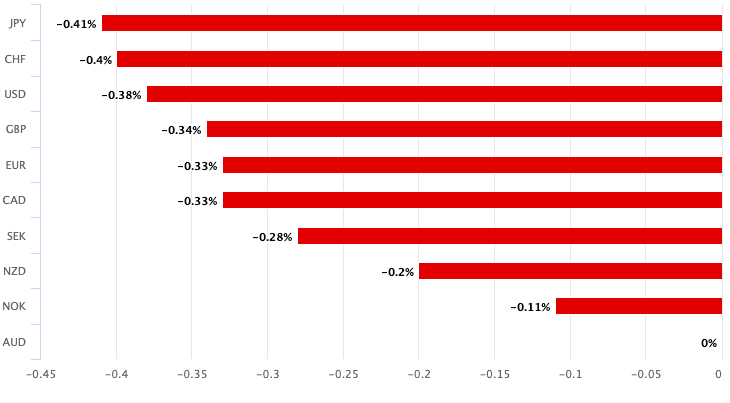

- AUD falls against all its major peers

- RBA likely to cut rates to 0.1% in Nov.

- Also signals potential move to 'pure' quantitative easing

Above: Governor Philip Lowe. Photo: O'Neill Photographics/Goldman Sachs. Source: RBA on Flickr, reproduced with permission from the RBA press office.

- GBP/AUD spot rate at time of publication: 1.8142

- Bank transfer rates (indicative guide): 1.7507-1.7634

- Transfer specialist rates (indicative guide): 1.7722-1.7979

- More information on specialist rates here

The Reserve Bank of Australia (RBA) has on Tuesday signalled it will offer the economy further support in coming weeks, a message that has triggered an across the board decline in the value of the Australian Dollar.

The RBA left interest rates unchanged at 0.25% and its quantitative easing programme unchanged at settings that will allow the Bank to target the three-year yield on Australian government bonds at 0.25%.

Yesterday we published a piece showing anlaysts were of the opinion that the Australian Dollar might rally in the event that the RBA keeps interest rates unchanged, however this expectation appears to be misguided given the currency market's reaction.

So what has transpired that has surprised markets and analysts alike?

It appears the communication offered by the RBA that caught investors' attention and meant the meeting did not pass by without incident for financial markets.

Economists have honed in on a change to the final paragraph of Governor Philip Lowe's statement. In September he said it "continues to consider how further monetary measures could support the recovery". In October the same paragraph now reads "the Board continues to consider how additional monetary easing could support jobs as the economy opens up further."

A shift to stating "additional monetary easing" is now coming is therefore an explicit one.

The rule of thumb in foreign exchange markets is that when a central bank signals interest rates are to fall in the future, or quantitative easing is to be increased, the currency it issues declines in value.

This is the knee-jerk reaction seen in the market following the RBA's October meeting.

The Pound-to-Australian Dollar exchange rate rose 0.34% to reach 1.8127, the Euro-to-Australian Dollar exchange rate rose 0.33% to quote at 1.6452 and the Australian Dollar-U.S. Dollar exchange rate fell 0.38% to quote at 0.7161.

In fact, the Australian Dollar is the worst performing major currency of the G10 pack:

Above: AUD performance on Oct. 06. If you would like to secure today's exchange rate for use at a date in the future, please learn more here.

"We take that as a clear indication the RBA will cut the cash rate to 0.1% when it next moves," says David Plank, Head of Australian Economics at ANZ Bank. "The addition to the final paragraph that the “The Board views addressing the high rate of unemployment as an important national priority” strongly suggests to us that the rate cut will come in November. It is a clear alignment with what is likely to be the theme of the Budget and why add it unless it is a reason to act."

An important question for markets is whether the RBA is also signalling it will shift its quantitative easing programme from a more 'spartan' one in which it does just enough to keep the payment costs of Australia's three-year government bonds anchored around 0.25%. There are suggestions that the RBA is signalling it will move away from this form of quantitative easing to a 'pure' form whereby it sets itself an absolute amount and targets bonds of varying maturities, similar to that pursued by the Reserve Bank of New Zealand and Bank of England.

This 'pure' form of quantitative easing is arguably more aggressive and therefore has greater implications for Australian financial assets, including the exchange rate.

Arguably, a more aggressive form of quantitative easing would weigh on the Australian Dollar going forward as the prospect of falling bond yields in Australia grows.

"The RBA is not ready to move to ‘pure’ quantitative easing just yet. But we have long thought that market dynamics will eventually force the RBA’s hand and require a move to ‘pure’ quantitative easing," says Plank.

Economists at St. George Bank in Sydney say that not only will the RBA cut interest rates in November, but they will also lower the target yield of the quantitative easing programme from 0.25% to 0.1%.

"The RBA’s reference to market pricing in today’s statement suggests a favouring of this approach," says Besa Deda, Chief Economist at St.George Bank. Lowe noted in his statement that "over the past couple of weeks, 3-year yields have fallen to around 18 basis points as markets price in some probability of further monetary policy easing".

However St. George Bank are also expecting to see a 'pure' quantitative easing programme introduced at some point in the future whereby more thank just three-year government bonds are targeted.

"We anticipate the RBA will engage in a large-scale asset program (LSAP) of buying government bonds beyond maturities of three years (i.e. four to ten years)," says Deda.

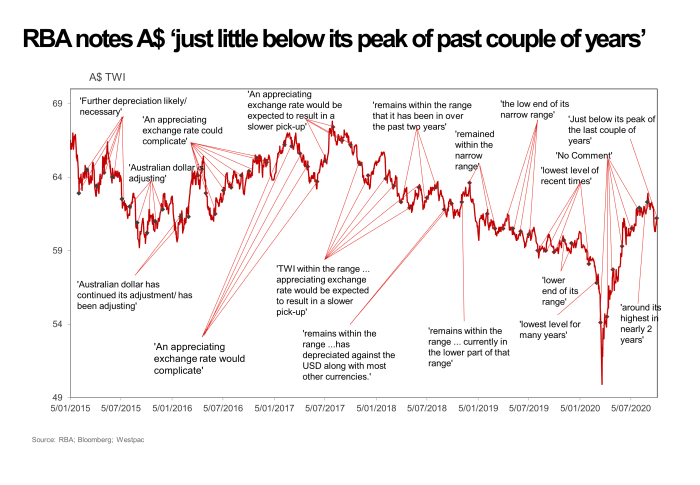

With regards to the value of the Australian Dollar, the RBA said "the Australian dollar remains just a little below its peak of the past couple of years" rather than the guidance offered in the Sep minutes that a "lower exchange rate would provide more assistance to the Australian economy in its recovery".

Investors were interested as to whether Lowe would echo the more targeted comments made about the currency by his deputy Guy Debelle in September.

Above image courtesy of Westpac

"We remain of the view that the Australian Dollar should remained capped by 0.7190/0.7210 near term... however, President Trump's health and the potential for US fiscal support remain significant drivers and positive news here could certainly lift the currency later," says Robert Rennie, a foreign exchange strategist at Westpac.