- ZAR at risk of losses this week as Mboweni delivers 2020 budget.

- Market looks for tax rises, Gov expenditure cuts and Eskom plan.

- But Gov is apt to disappoint, placing Moody's rating in question.

- Market could price downgrade if no improvement on Oct budget.

- Citadel Wealth Management tips 2020 rating downgrade to 'junk'.

- RBC eyes ZAR losses post-budget as market prices downgrade.

Image © Government of South Africa, reproduced under CC licensing

- GBP/ZAR Spot Rate: 19.56, up +0.17% today

- Indicative bank rates for transfers: 18.89-19.03

- Indicative broker rates for transfers: 19.28-19.40 >> find out more about this rate.

The Rand is the emerging world’s worst performing currency of 2020 but the going could get tougher in the week ahead if South Africa’s 2020 budget is poorly received by the market on Wednesday.

South Africa's Rand has entered the week on the back foot amid panic in the markets over the spread of coronavirus outside of China after so-far small outbreaks were confirmed in South Korea, Japan and Italy among others, leaving the 2020 uptrend in the Pound-to-Rand rate intact while taking USD/ZAR comfortably above the 15 handle.

Coronavirus could remain a headwind to emerging market currencies for a while yet but domestic risks are also at play this week with Finance Minister Tito Mboweni set to deliver the 2020 budget in parliament Wednesday.

"To turn the tide here for markets, we need a turn in coronavirus news, one that has so far entirely failed to materialize and may be hard to achieve for a long time if the contagion spreads to countries less able to deal with the outbreak like the strange case of Iran. Until then, we will continue to watch for strain in credit markets from the the disruptions in supply chains and shutdown of activity. This is not a situation where traditional stimulus works very well," says John Hardy, head of FX strategy at Saxo Bank.

Moody’s, the last agency to still rate the government’s Rand-denominated bonds as ‘investment grade,’ will be looking for signs of improvement on the dire outlook given back in October and if it's not forthcoming markets might view the risk of a downgrade as having risen, leading to even more losses for the Rand.

Above: Pound-to-Rand rate shown at daily intervals.

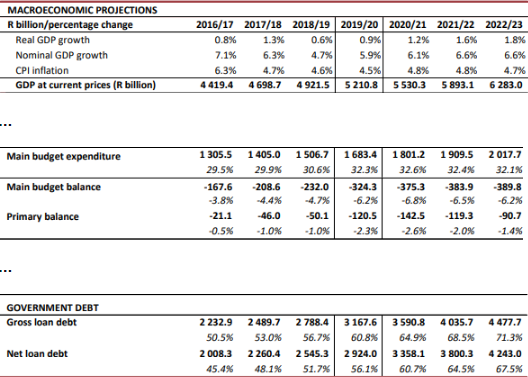

October’s medium-term budget statement left the Rand reeling when it revealed the government, which has a tendency toward optimistic forecasts, is expecting the “main budget” deficit to deteriorate from -4.7% in 2018 to -6.2% for last year before topping out at -6.8% of GDP in 2020.

That put the anticipated gross-debt-to-gdp ratio on a short but steep climb from 56.7% in 2018, to 71.3% by 2022/23. And Moody’s subsequent decision to cut the outlook on the rating from stable to negative was seen as a hint that a downgrade to ‘junk’ could be imminent, which wounded the Rand.

“We see scope for ZAR weakness on the back of the 2020 Budget, given our internal positioning monitor shows the market is only slightly long USD/ZAR and some market participants are expecting the downgrade to be delayed to late 2020,” says Daria Parkhomenko, a strategist at RBC Capital Markets.

Above: Selected excerpts from October MTBPS.

The Moody’s rating matters for the Rand because a downgrade to junk would force the sale of South African government bonds by fund managers who are only able to hold 'investment grade' debt, leading to potentially large capital outflows.

Active fund managers may already have sold their South African bonds in anticipation of a downgrade although managers of passive funds that mimic pre-determined benchmarks like the Citi World Government Bond Index, now called the FTSE World Government Bond Index, wouldn’t be able to sell until the country is actually excluded from those benchmarks by a downgrade.

“Everyone expects this Budget to be poor but they might manage to demonstrate the will to cut expenditure and show just enough fiscal consolidation and, in that case, Moody’s might delay any decision until November, after the next MTBPS,” says Mike Van der Westhuizen, a portfolio manager at Citadel Wealth Management.

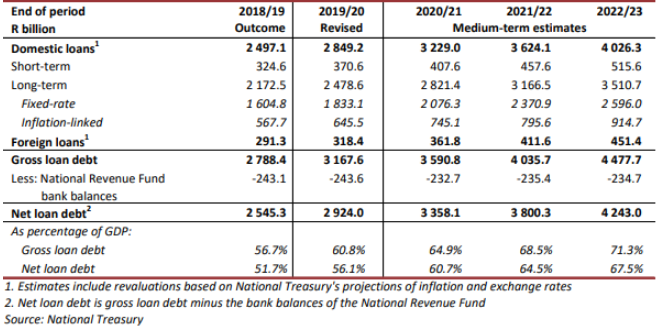

Above: October MTBPS table showing foreign position in capital structure.

Analysts and economists have said that if the government announces a 1% increase in the VAT tax rate Wednesday it would eliminate around 40% of the funding shortfall anticipated by the government for the next year threes, although Citadel’s Van der Westhuizen says that won’t be enough for Moody’s.

He says the government will need to take an axe to its spending commitments as well as raise taxes if it’s to stave off a downgrade when Moody’s next reviews the rating on March 27. And that markets should expect more financial support to be announced for the ailing electricity provider Eskom.

The prospect of a downgrade to ‘junk’ has been hanging above South Africa’s head for years, keeping the Rand close to record lows against the Dollar, as low levels of economic growth and mounting demands on the public purse have seen the government’s balance sheet continue to deteriorate.

“While many are trying to remain optimistic, a pragmatic and unemotional approach to the country and the fiscal state of the nation is essential at this juncture. We’ve been aware of these risks for the past few years and, in terms of portfolio positioning, have been underweight South African government bonds and overweight enhanced cash and the US dollar for a while. We will continue to search for the lowest risk route to get to the other side of the junk divide,” Van der Westhuizen says.

Above: USD/ZAR rate shown at daily intervals.

Citadel’s Van der Westhuizen says 2020 will be the year that Moody’s finally makes the call and downgrades the rating either in March or November, which could hurt the Rand at the time because foreign holdings of South African bonds are large. Treasury estimated in October that foreign holdings of government debt totalled R318.4 bn, which is more than 6% of GDP.

However, Van der Westhuizen says the market’s reaction to an eventual downgrade would be a flash-in-the-pan instead of the beginning of a short, medium or long-term trend.

In other words there could be a big crash and a bang in the South African bond and currency markets upon a downgrade, followed by stabilisation or possibly even a recovery rally in bonds and the Rand.

Bond investors have after all, been increasingly starved of yield ever since the financial crisis and more so in the negative-interest rate and negative-yield era of 2016 onward. Others have a similar view.

“We see scope for ZAR weakness on the back of the 2020 Budget,” says Daria Parkhomenko, a strategist at RBC Capital Markets. “If the 2020 Budget insufficiently addresses the deterioration in fiscal dynamics, a downgrade should be “priced in” by the time we get to Moody’s review on March 27, raising the hurdle for “negative” news on the decision day...our forecasts imply modest ZAR weakness vs USD on the back of a downgrade in March.”