The US Dollar continues to undergo a period of corrective selling pressures having lost 1.56% against the Yen and 1.51% against the Pound over the course of the past five days.

Against the Euro it is 0.6% lower and has only managed to eke out some gains against the commodity Dollars.

Investors have been surprised by the currency's performance since the Federal Reserve announced an interest rate rise in mid-March.

The reason for the underperformance is that investors are selling the Dollar as an expression of disappointment after the Fed suggested markets should only expect two further interest rate rises in 2017.

What the Dollar needed to hear was that the Fed was considering a third rate rise.

But are the Fed and the markets right in maintaining these expectations and is this therefore just a temporary set-back or a deeper more sustained contraction for the Dollar?

John Higgins, US Economist at Capital Economics, is of the opinion that the current pull-back is only temporary and that the Dollar will rise again.

Higgins thinks the weakness was initially due to Fed members not upgrading their forecasts for the Fed base lending rate as reflected on the Federal Reserve dot-plot.

“The median projections of FOMC participants for the federal funds rate at the end of 2017 and 2018 were left unchanged from their levels in December. This appears to have been the cause of the dollar’s retreat, as some had expected them to be raised,” notes Higgins in a briefing to clients dated March 20.

Higgins says markets have overly low expectations of the path of future rates:

“In our view policymakers will end up tightening by more than they and investors are envisaging, as inflation picks up steam," says Higgins.

The implied rates on the January 2018 and January 2019 federal funds futures contracts are around 1.30% and 1.75%, whereas Capital Economics have an end-2017 and end-2018 mid-point forecasts for the federal funds rate remaining at 1.625% and 2.625%.

Meanwhile, Capital Economics expect monetary policy in other developed economies to stay very loose which should benefit the Dollar against its major counterparts.

He is not the only one.

Knut Magnusson at DNB Markets also expects higher interest rates than that currently expected by the market.

“The market is pricing in around two hikes in the coming year. This is clearly lower than indicated by the dot-chart, and also less than what we forecast,” says Magnussen in a note to clients dated March 20.

Magnussen actually sees two more rapid rate rises happening this year, one in June and then a second in September, which is far quicker than anticipated by current market expectations, and if he is right it should propel the Dollar higher.

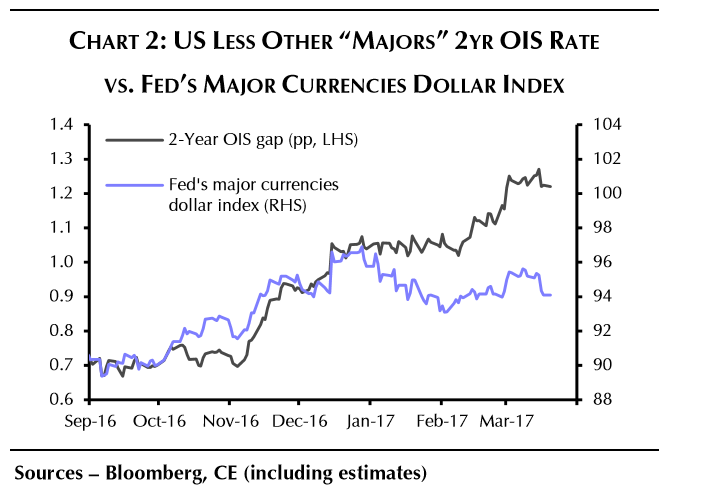

And, the Dollar now looks oversold.

Based purely on the difference between the Dollar Index and Overnight Index Swaps which track interest rate expectations the Dollar is now considerably undervalued as the chart below shows:

Higgins puts this divergence down to overblown concerns held by investors on Donald Trump’s protectionist trade agenda, something which Higgins expects to fade in coming months.

Higgins puts this divergence down to overblown concerns held by investors on Donald Trump’s protectionist trade agenda, something which Higgins expects to fade in coming months.

“Although the relationship shown in the Dollar Index to 2-year OIS Rate above has broken down this year, this has probably been due to the influence of temporary factors such as investors’ concerns about the Trump administration’s attitude towards protectionism. We expect the influence of these factors to fade in time, allowing the dollar to resume its rise,” says Higgins.

But, not all analysts are as optimistic concerning the Dollar's prospects.

Dollar's Slide is Going to Continue

Nordea Markets see storm clouds on the horizon for the US economy, and this week’s housing data may be key in relation to this view as “housing leads the economy,” as they say.

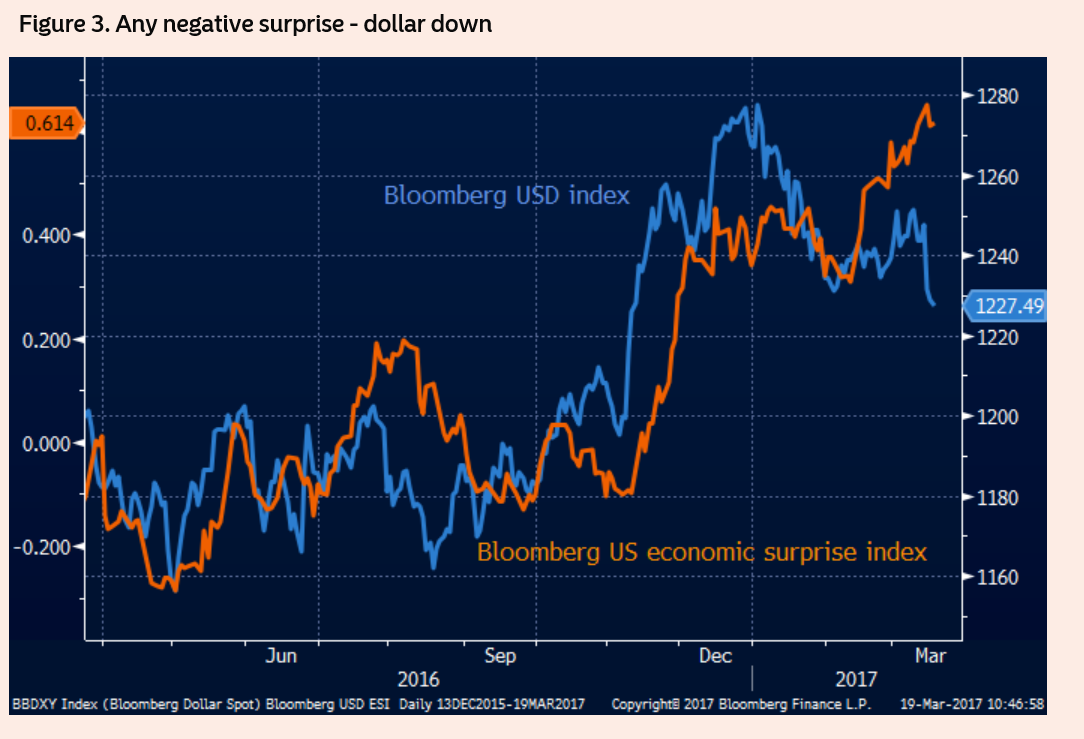

The Nordea analysts highlights the growing divergence between the economic surprise index in the US, which tracks the difference between over and undershoots in economic data and the USD Index.

The fact the Surprise Index has disengaged from the Dollar and moved higher is a sign in her view that the upside surprises are stretched and due a pull-back, indicating data in the US might start to deteriorate.

“We have passed peak activity, and even the first US regional manufacturing survey data has ticked lower last week. Keep watching those as the indication for the next ISM. As a reminder, any miss in data is bad for the USD,” says Augulyte.

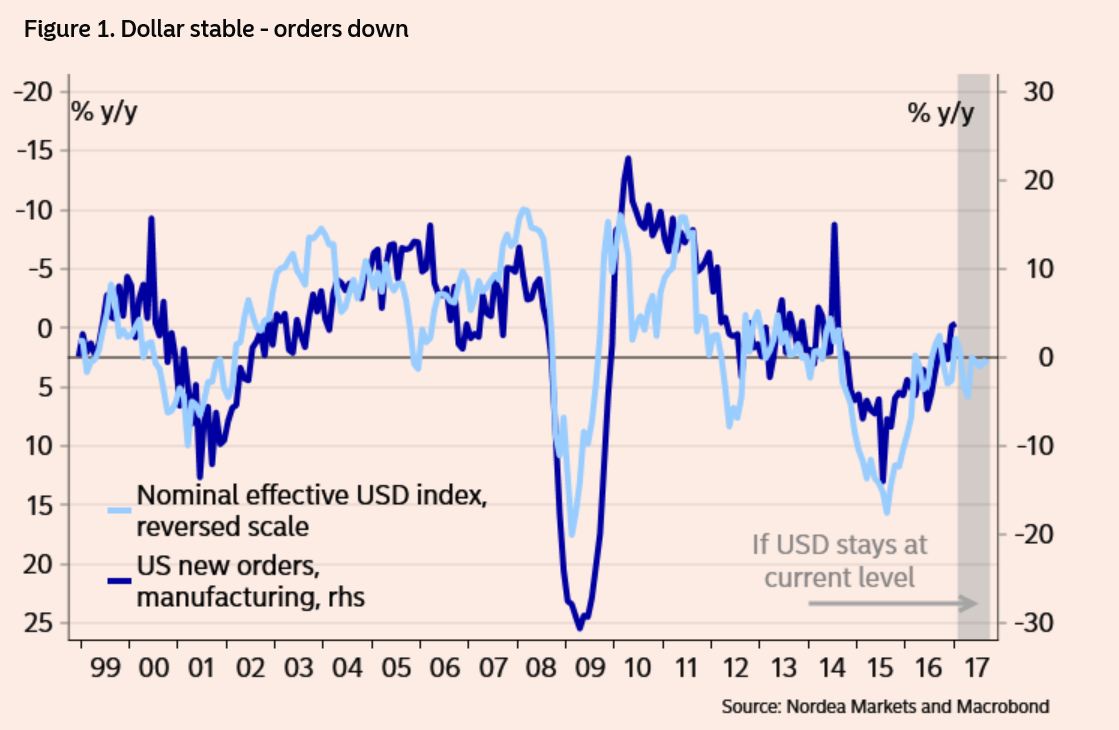

This reinforces her central hypothesis that the strong Dollar has now become detrimentally strong.

She notes, for example, how the current level is commensurate with a flat or declining growth in Manufacturing.

“Say, the USD stays at these levels – base effects are negative to industry at least until October. Also, should oil prices stay at these “comfortable” levels for the rest of 2017, we will probably see industrial contraction in the US by New Year!”

Nordea Markets are forecasting the Pound to rise back to 1.27 against the US Dollar on the back of this weakness.