The British Pound's rally could continue in the near-term as short-positioning is flushed out of the market and a November interest rate rise is fully priced argue analysts at Deutsche Bank.

Pound Sterling has made substantial gains this September as the Bank of England tells markets it believes an imminent rise in UK interest rates is appropriate.

The suggestion, made by the Bank at their September meeting and subsequently reinforced by Governor Mark Carney on two occasions, has seen a notable re-evaluation of the Pound in global foreign exchange markets as a result.

The Pound-to-Euro exchange rate rose stratospherically, from a pre-meeting open of 1.1114 to highs of 1.1395 24 hours later, and the Pound-to-Dollar exchange rate from 1.3211 to 1.3616.

Gains have since faded somewhat with traders booking profits at the start of the new week, and the question those watching the market is whether the gains are over.

Oliver Harvey, Macro Strategist at Deutsche Bank believes the Pound still has further to run, in the short-term at least.

For Harvey the gains appear to be a function of a technical squeeze on short positions held against the Pound.

'Short positions' are bets held by the trading community that a currency will fall further, and when they reach an extreme what often happen, the market reverses and goes in the opposite direction on any unexpected counter-trend news.

Think of a spring being stretched and then being let go.

In the case of the Pound, this happened when short-bets proliferated in the weeks leading up to the BoE meeting, only for the Pound to surge when the BoE delivered an unexpected message.

This inevitably led to some closing or 'covering' of shorts, which would have fuelled the uptrend.

The question now is whether the rally can last, or whether it is spent and it is time to 'fade' it.

Deutsche's Harvey says this pro-Pound move we are seeing still offers more upside for the Pound, at least in the near-term.

Deutsche Bank now expect an interest rate rise to be delivered in November; thanks to the Bank of England’s recent inferences.

However they do not see a November hike as wholly discounted by the market yet, and this, combined with more upside left in the short-squeeze, continues to make them bullish in the short-term.

The September meeting “was even more hawkish than we expected and we have subsequently changed our rate call for a hike in November. With this still less than 100% priced, and given the build up in short positioning over recent weeks, we wouldn’t fade the rally in GBP just yet," says Harvey.

Beyond the short-term, Harvey points to extended uncertainty that should cap Sterling's exuberance.

“Medium-term, the structural sterling outlook will depend on whether the recent improvement in the external balance is sustainable, whether UK growth can tolerate the Bank of England hiking and the timing of a Brexit deal."

Major question marks remain on each of these issues.

"But in the short-term at least, we think the move higher in GBP has further to run," says Harvey.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Brexit: Risk or Opportunity?

Some analysts have pointed out that the risk of a breakdown in Brexit negotiations is still a threat to Sterling and focus will soon shift away from the Bank of England and back to Brexit.

Harvey is nevertheless optimistic in the short-term:

"On Brexit, we don't think agreement on divorce is reached at the October EU Council meeting, but PM May's Florence speech next week is likely to strike a conciliatory tone and the UK government has been moving towards a more pragmatic position over the summer."

Contrasting with this view is that of Italian lender Intesa San Paolo, who see the currency weakening over the 1-3 month period before recovering more broadly into 2018.

The discrepancy in the two short-term outlooks comes from Intesa Sanpaolo highlighting the potential for Brexit negotiations to go wrong and negatively impact the Pound in the short-term.

"The contained retracement expected in the very near term mostly reflects uncertainty on the outcome of Brexit negotiations, which are proving difficult," said Intesa's Jamelah Asmara, who seems GBP/USD pulling back to 1.32.

The view is shared, although to a less degree, by MUFG's Lee Hardman, who sees GBP/USD falling to 1.33 in the near future.

Hardman also sees downside risks from Brexit uncertainty, although he also see weakness from the economy not performing as well as expected:

"A sharper slowdown in UK growth in the coming quarters and/or a breakdown in Brexit negotiations could yet outweigh the supportive impact for the pound from a higher BoE policy rate," says Hardman.

Overall MUFG is ultimately optimistic about the UK and the EU reaching a transitional agreement to prevent a negative cliff-edge Brexit.

"The BoE’s relatively optimistic outlook for the UK economy and monetary policy is based on the assumption that the UK government is likely to secure a transitional agreement with the EU to help smooth the Brexit adjustment for the UK economy in the coming years," adds Hardman.

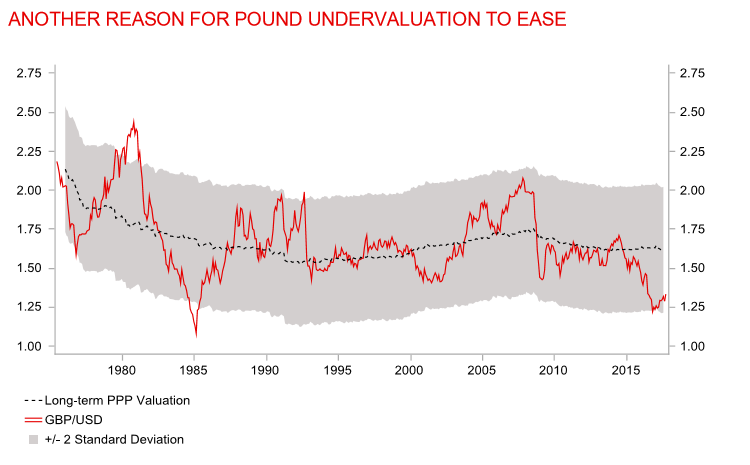

Sterling Undervalued

Another reason to expect the Pound to continue rising both in ths short and longer-term, is that historically it is at extremely devalued levels and therefore unlikely to make further significant loses.

MUFG show a chart of the trade weighted index (TWI) of the Pound, which is Sterling versus a basket of its most heavily traded counterparts.

The chart shows the long-term average of the TWI with an envelope around it at a distance of two standard deviations of the average and then on top of that GBP/USD superimposed.

GBP/USD has just bounced off the bottom of the envelope - an extremely undervalued level, and a level often respected in the past - which suggests the pair has reversed from major undervalued lows and is now set on a course of rising.

HSBC Scrap Forecast for Pound to Par Euro in Value

The Pound's recent rally against both the US Dollar and Euro has seen the analyst community adopt a more constructive tone with regards to the outlook.

Of note, HSBC Bank plc have briefed clients of an upward shift in forecast targets for Sterling that no longer anticipate GBP/EUR falling to 1.0.

The UK bank had been the most bearish on GBP/EUR in a regular poll of forecasters but by raising forecasts they move closer to consensus which more or less see GBP/EUR ending 2017 at 1.12.

“We were wrong. Contrary to our expectations, GBP has been exclusively driven by cyclical forces in 2017,” says David Bloom, Strategist with HSBC Bank plc based in London. “Combined with a more hawkish BoE, we revise our year-end 2017 forecast.”