The Euro to Dollar exchange rate continues to exhibit signs of strength that can see it extend its short-term rally, according to Fawad Razaqzada, an analyst at City Index.

Last week saw the EUR/USD eke out another weekly gain following a large rally the week before, thereby maintaining its recent bullish bias.

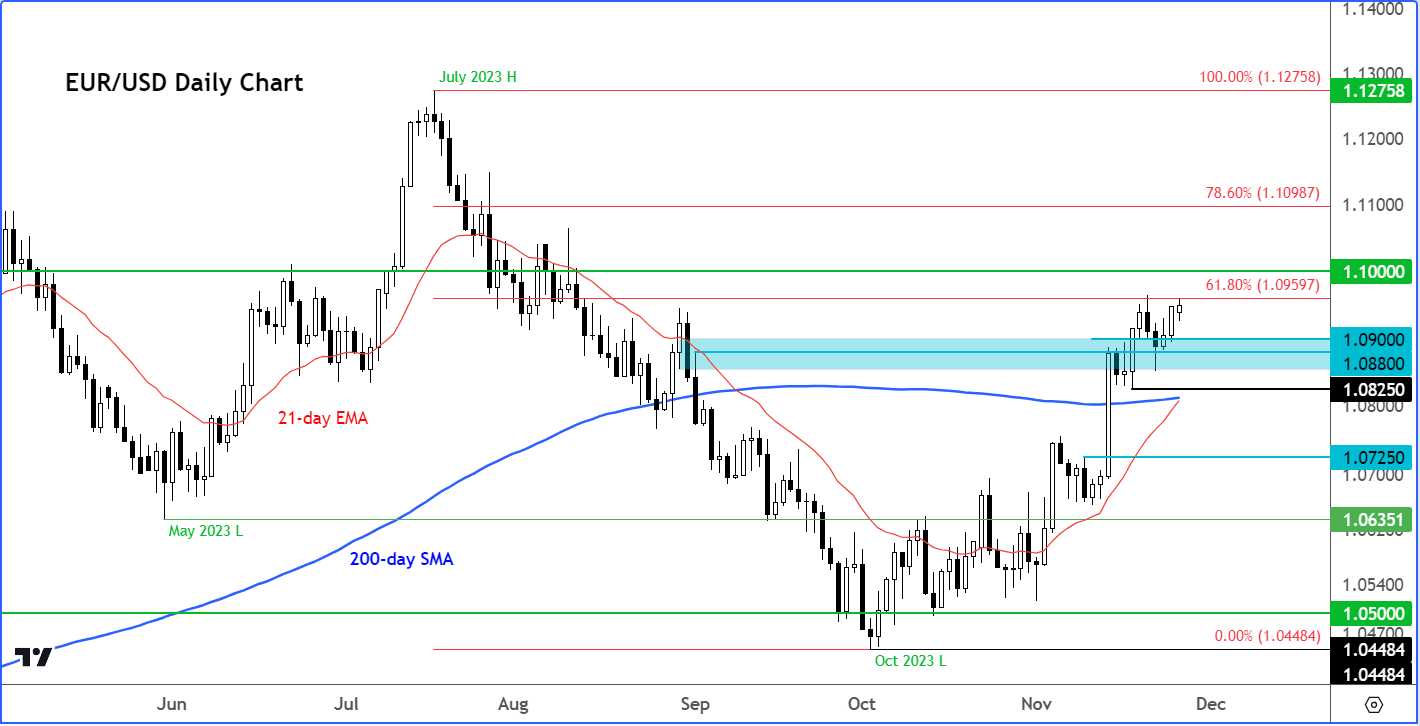

It has now managed to hold above the 200-day average for 9 sessions and counting, which is a sign of strength. So, the path of least resistance remains to the upside.

The EUR/USD held support around an area where it had struggled previously, namely around 1.0880 to 1.0900. The Bulls will need to continue defending this zone to keep the bullish momentum alive.

The line in the sand is at 1.0825, which was the most recent low. If the EUR/USD falls below this level, I would anticipate a correction towards the base of the previous breakout around 1.0725.

However, this isn't my primary expectation.

Considering the recent bullish momentum, it seems more probable that the EUR/USD will move towards and possibly above the 1.10 level rather than dropping below 1.0825.

Image courtesy of City Index.

The EUR/USD’s upward drift continues as it edges ever closer to the 1.10 handle, now less than 50 pips shy of that psychological barrier.

It has been a good month for the EUR/USD, rising nearly 450 pips (4.25%) from the lowest to the highest point of the month so far.

As we enter the final week of November, can we extend those gains to 500 pips, and potentially set the stage for further follow-up gains in December?

Track EURUSD with your own custom rate alerts. Set Up Here.

The US dollar has been weakening across the board as the market becomes increasingly convinced that the next move from the US central bank will be to cut interest rates, possibly as early as the second quarter.

In fact, the odds of a cut in May are nearing 50% probability, as per the CME Group’s FedWatch tool.

The dollar edged lower last week following a big drop the week before, when softer-than-expected CPI and PPI figures poured cold water on recent hawkish Fed comments, keeping yields under pressure.

On Monday, new home sales data came in below expectations. With global stock markets also being excited by the possibility of central banks adopting a more dovish stance moving forward, with signs of global inflationary pressures slowly moving to normal levels around the world, this is also helping to keep the dollar under pressure, boosting the appetite for foreign currencies.

Meanwhile, European data has started to show some signs of stabilisation. Last week for example saw the PMI data surprised to the upside, if still in the contraction territory, while German Ifo business climate rose for the second consecutive month.

Investors will be looking ahead to a key week for data, with inflation figures from both the eurozone and the US, as well as GDP and a few other US macro pointers, all to come.

ECB president Christine Lagarde on Friday said that the fight against inflation is still not over, even though no more rate hikes are expected.

U.S. Data to Watch

The preliminary estimate for the US GDP in the third quarter is slated for release on Wednesday.

Should there be a notable revision from the initial 4.9% annualized growth reported last month, it may well influence the EUR/USD’s trajectory. The previous estimate surpassed expectations, resulting in a positive response in the US dollar.

The question now is whether a similar reaction will occur this time, or if the markets are more attuned to forward-looking data, considering the GDP is a couple of months old.

On Thursday, the core PCE price index is set to be unveiled. Given that the US headline CPI fell below expectations, traders are keen to see if this weakening inflationary trend persists in the upcoming PCE figures.

This is pivotal for maintaining the belief that the Fed might lower interest rates in the first half of the coming year. The core PCE is typically the Fed's preferred inflation metric due to its lower volatility compared to traditional CPI measures.

Therefore, a stronger reading could dampen risk appetite, strengthen the US dollar, and prompt traders to reassess their expectations of an earlier-than-expected rate cut in 2024.

A +0.2% reading or lower would likely align with the current market narrative of peaking interest rates and a potential rate cut in the first half of 2024, potentially weakening the US dollar and supporting the EUR/USD.

Eurozone Data to Watch

On Wednesday, we will have the most recent inflation data from Germany, followed by the Eurozone flash CPI estimate a day later. In September, the latter moderated to a 4.2% annual rate from the previous month's 4.5%, following an even more pronounced decline in the month preceding.

Let's see whether the trend of disinflationary pressures persisted in October. If so, this could positively impact European stock markets, consequently offering indirect support to the risk-sensitive euro.

Therefore, the EUR/USD may, actually, find support if Eurozone inflation weakens further. This is paradoxical since such a scenario is usually deemed to have the opposite impact. But as it is likely to enhance the appetite for European stocks, it may indirectly offer support for the risk-sensitive euro. Consequently, the possibility of a move towards or above the 1.10 handle on the EUR/USD remains viable, even if we see a weaker Eurozone inflation print.