Written by Charalampos Pissouros, Senior Investment Analyst at XM.com. An original version of this article can be found here.

The yen is extending its recovery today after Japanese media carried a report expressing confidence that the end of the Bank of Japan’s negative interest rate policy is approaching.

Raising interest rates at a time when other central banks are expected to start cutting rates could narrow the gap between Japanese government bond (JGB) yields and yields elsewhere, thereby allowing the yen to stage a solid comeback against most of its major peers.

What may have also helped the Japanese currency is separate news that Japan’s top business lobby, Keidanren, is planning to hold discussions on the negative impact of the yen’s slide on the economy at its December meeting.

In the past, the lobby has favoured a weaker yen as it makes exports more competitive overseas, and thus, the shift to discuss negative implications highlights the severity of the impact of the currency’s latest fall on the economy.

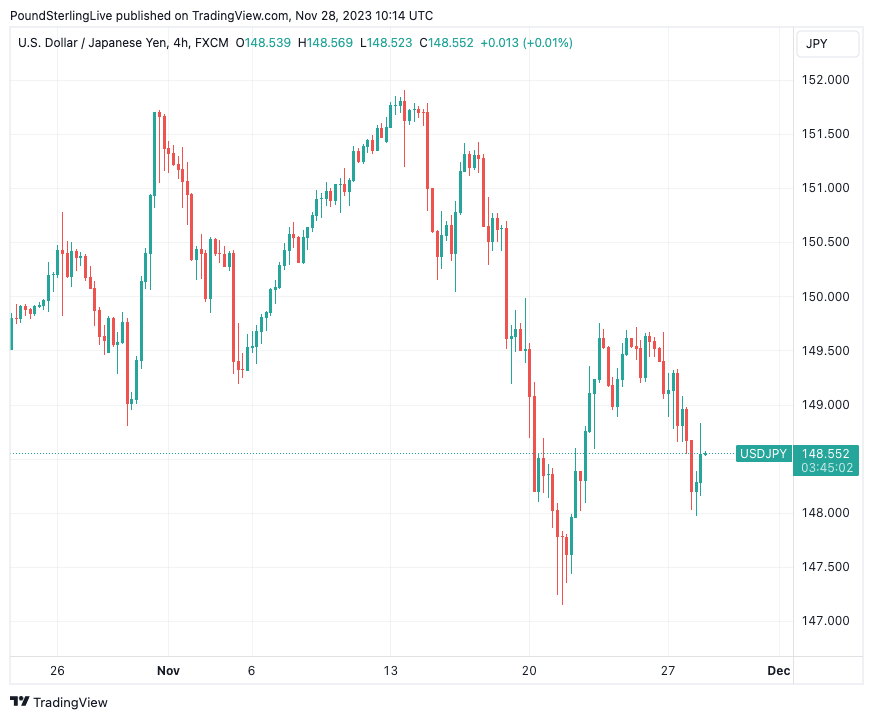

Above: Dollar-Yen shown at four-hour intervals. Track JPY with your own custom rate alerts. Set Up Here.

The US dollar continued trading on the back foot against its major peers on Thursday, losing the most ground against the yen, the aussie, and the kiwi, in that order.

It seems that expectations of several cuts by the Fed next year continue to weigh on the greenback, with the weaker-than-expected new home sales data yesterday corroborating investors’ view.

According to Fed funds futures, market participants are pencilling in around 90bps worth of rate cuts for next year, assigning a 50% chance for the first 25bps reduction to be delivered in May and fully pricing it for June.

Traders are now likely awaiting the core PCE index on Thursday, the Fed’s favourite inflation metric, where a further slowdown could increase the probability of a May cut and perhaps push the dollar even lower.

However, investors will have the opportunity to listen to several Fed officials before the numbers are out, with Chicago President Goolsbee and Board Governors Waller and Bowman stepping onto the rostrum today.

It will be interesting to see whether they will push back against rate cut expectations but also whether the market will pay attention to such comments.

Recent market moves suggest that investors prefer to focus more on data rather than Fed rhetoric, and thus, even if policymakers decide to pour cold water on rate cut expectations, any rebound in the dollar due to their remarks could remain limited and short-lived.

The aussie was the second winner in line yesterday, as the divergence in policy expectations between the RBA and the Fed is adding fuel to its engines.

Today, RBA governor Bullock said that they have to be a “little bit careful” with using interest rates to tame inflation without lifting unemployment, but she added that demand is being propped up by immigration, which has contributed to second round effects of cost rises, and that service inflation is sticky.

This allowed investors to continue pricing in around a 60% probability for another quarter-point hike by May.

The kiwi was also among yesterday’s top gainers, despite bets of around 40bps worth of rate cuts by the RBNZ next year.

The Bank meets tonight, during the Asian session Wednesday, and expectations are for no action. Ergo, the focus is likely to turn to the accompanying statement and the updated macroeconomic projections, on signs about the future path of interest rates.

Although recent data out of New Zealand came in on the soft side, inflation remains well above the RBNZ’s 1-3% target range, with inflation expectations suggesting that inflation is not likely to return within that range in the coming year. What’s more, New Zealand’s governing coalition is likely to be led by the National Party, which promised tax cuts, an inflationary policy, and suggested the adoption of a stricter inflation target by the RBNZ.

This means that if the Bank switches to a 2% objective like other major central banks, policy may need to stay restrictive for longer than previously estimated to achieve that target.

Therefore, officials are unlikely to affirm market expectations of rate reductions. They will probably continue to predict that interest rates will finish 2024 at the current 5.5% level, which could prove positive for the kiwi.