"We will cross the neutral rate (regardless of where anyone currently sees it) like a runaway train. We need to get monetary policy into the restrictive environment, at least for a certain period," Peter Kazimir, Governor of Narodna Banka Slovenska.

Image © European Union - European Parliament, Reproduced Under CC Licensing.

The Euro remained one of the better performing major currencies this week even after October's European Central Bank (ECB) decision prompted the market to perhaps mistakenly adjust its expectations for interest rates lower.

Europe's single currency rebounded on Friday from widespread losses sustained in the wake of Thursday's ECB policy decision, which saw all of its interest rates raised for a third time running but left the market less certain of what can be expected from the bank in the months ahead.

The ECB said "substantial progress" had been made in withdrawing the monetary support provided to Europe's economies in recent years but that further increases in interest rates are likely to be needed, which markets took to mean the ECB's interest rate cycle may be nearing its end.

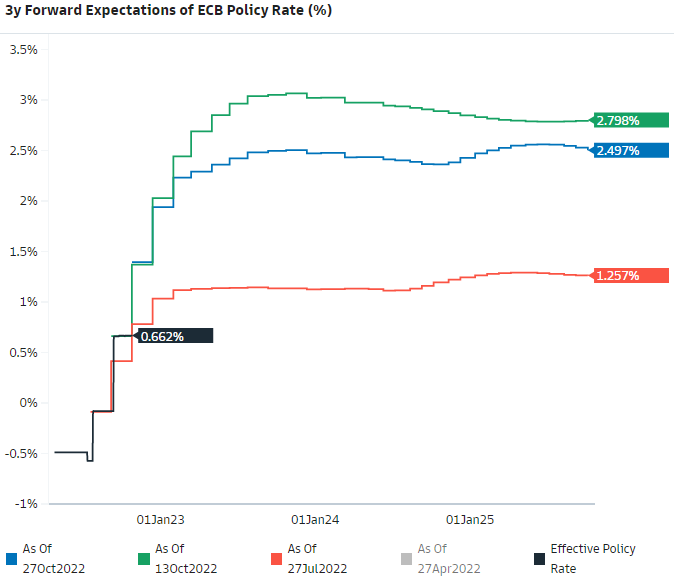

This interpretation was evidenced by a retreat of expectations implied by the Overnight Indexed Swap market where rates shifted to suggest that some investors now anticipated that the ECB's once-negative deposit rate will top out around 2.55% next year, down from 2.8% prior to Thursday's decision.

However, some Governing Council members have since argued that the market was mistaken in its interpretation of Thursday's statement.

Above: Market-implied expectation for ECB deposit rate before Thursday's decision and at other earlier intervals. Source: Goldman Sachs Marquee. Click image for closer inspection.

Above: Market-implied expectation for ECB deposit rate before Thursday's decision and at other earlier intervals. Source: Goldman Sachs Marquee. Click image for closer inspection.

"There is a risk that inflation in Eurozone will remain higher for longer, and we stay above the target despite the expected drop in inflation over the next two years. This is not acceptable, and we need to act. Consistently," says Peter Kazimir, Governor of Slovakia's central bank, on Friday.

"We will cross the neutral rate (regardless of where anyone currently sees it) like a runaway train. We need to get monetary policy into the restrictive environment, at least for a certain period," he later added in conclusion of an op-ed published by the Narodna Banka Slovenska.

Kazimir's comments suggest that the ECB's statements highlighted earlier were in fact a reference to the "neutral rate" of interest as well as an indication that the ECB intends to lift interest rates above there and to a restrictive level as part of its effort to return inflation to the 2% target.

That would be just one interpretation, however, and there are now 20 national central banks represented on the ECB's Governing Council so little could be said for certain until after the next meeting in December.

With that, below is a selection of remarks setting out how analysts and economists have interpreted Thursday's update and what they think it could mean for the Euro in the weeks and months ahead.

Sven Jari Stehn, chief Europe economist, Goldman Sachs

"Taken together, today’s communication suggests that the Governing Council is preparing the ground for a slowdown in the pace of hiking as the deposit rate is now approaching levels that might be regarded as neutral, the growth outlook has continued to weaken and other central banks are slowing the pace of hiking."

"Today’s meeting therefore reinforces our view that the Governing Council will step down to 50bp at the December meeting. But we maintain our forecast that the Governing Council will take the deposit rate into restrictive territory of 2.75% in March in light of ongoing inflation pressures."

"President Lagarde indicated that the Governing Council will publish the principles for the unwind of the APP portfolio at the December meeting. We stick to our forecast that ECB officials will decide in Q1 to start passive PSPP run-off at the beginning of Q2, although an announcement is possible as soon as December."

Silvia Ardagna, chief Europe economist, Barclays

"The meeting was dovish relative to expectations and past meetings, but more tightening is coming and is likely to dampen demand, despite this no longer being an explicit ECB goal."

"Although the statement highlighted room remaining to reach the terminal rate, the removal of "several meetings" from the monetary policy statement and a full data-dependent, meeting-by-meeting approach open up the door to a possible pause in hiking rates sooner than we currently forecast if economic activity is in line with our projections."

"But, equally likely, we think the ECB could quickly turn more hawkish again on grounds of very elevated inflation, particularly if labour market strength remains and wages accelerate notably. We think the debate between the hawks and doves of the Governing Council will gain steam again and uncertainty around rate decisions to be taken at each meeting will likely increase."

Chris Turner, regional head of research for UK & CEE, ING Group

"Certainly, interest rate markets took note of the reference to 'substantial progress being made in withdrawing monetary accommodation' and took 30bp off the pricing of the terminal ECB rate, which is now priced at 2.50%. We still think that it is too high."

The repricing of the ECB cycle saw euro two-year swap rates fall and the spread to two-year dollar rates (normally a key driver of EUR/USD) widen back out to 200bp in favour of the dollar. That is the widest since mid-August.

"We had said going into the meeting that interest rate differentials had not been playing a big role in EUR/USD pricing, although that could reverse into December as speculation of an ECB pivot grows."

"EUR/USD might bounce around a little as ECB hawks brief the media that the central bank's statement was not quite as dovish as the market interpreted."

"But we think the dollar should stay supported into next week's FOMC meeting and would favour EUR/USD edging down today to the 0.9910/20 area – marking the top of a bear trend channel which was recently broken."

Claudio Wewel, FX strategist, J. Safra Sarasin

"Acknowledging that the global macro backdrop remains a challenge for the euro, we see scope for some near-term upside for EUR-USD."

"Given that euro area inflationary pressures are broadening and remain elevated, the ECB will continue to tighten monetary conditions, which should lessen the US dollar’s current yield advantage and act as support for the euro, going forward."

"Moreover, energy shortages may represent less of a headwind for the euro area economy than previously assumed, given that national gas storages are filled close to capacity and the prospect of a relatively mild winter."

"We think that an extended EUR-USD recovery is unlikely, given that the dollar’s uncertainty premium should persist as long as the war in Ukraine drags on."

Ulrich Leuchtmann, head of FX research, Commerzbank

"ECB President Christine Lagarde sounded a little more dovish yesterday than we might have expected. Nonetheless, the question of what central banks will do in case of higher or lower inflation levels is easier to answer than at the start of the inflation shock."

"We still do not know whether the rates of inflation will continue to rise in the different currency areas or whether they will fall again. All projections on the question (regardless of whether they are produced by central banks or others) were so incorrect in the past that market participants are better off not believing anything any longer."

"Only one thing has changed: it is no longer the central bank communication that attracts attention but the data on inflation developments."

Piet Haines Christiansen, chief strategist for ECB and fixed income, Danske Bank

"With the ECB still firmly in tightening mode, the recession risks for the euro area economy are increasing."

"Markets are pricing the ECB deposit rate to peak at 2.58%, slightly above our 2.5% call."

"The market is likely to maintain a negative view about EUR/USD spot. This stagflation theme and that higher European interest rates remain negative for the currency are well in line with our long-held USD-positive view and we have repeatedly seen such market reaction."

"We continue to forecast EUR/USD spot in the low 0.90’s and view today as confirming and likely supporting that view."

Radhika Rao, senior economist, DBS Group Research

"There will likely be a few divisions in the December rate review."

"We don’t expect the rate action to have material impact on the EUR/USD price action. What might matter more is a dovish pivot by the US FOMC, if any, which might be a bigger driver for growth and rate differentials."

Mazen Issa, senior FX strategist, TD Securities

"Overall, Lagarde seems to have indicated a pivot without explicitly saying as much (perhaps less obvious than the dovish BOC hike). That said, the non-committal nature over the future path of policy and its pace leaves us with the impression that it is reasonable to expect a downshift by the ECB."

"The implications of this are notable, because it effectively implies that the interest rate differential with the US will remain wide. While spreads are not a major driver at the moment, FX factors are notoriously time varying so one would expect it to resume significance at some point in the future."

"While we are sympathetic to the recent move lower in the USD, we are more skeptical that this is the inflection point for the broad USD."

"For now, we are still cautious on EURUSD as the global growth impulse continues to downshift. A move below 0.99 should be seen as a confirmation of a return to the downtrend channel, while a push to 1.02 will likely cap upside."

Lee Hardman, currency analyst, MUFG

"We continue to expect the deposit rate to peak below current market expectations of around 2.75%."

"The main immediate takeaway for financial markets is that the ECB has become the latest G10 central bank to disappoint expectations for a more hawkish policy update."

"It follows dovish surprises from the RBA and BoC when they delivered smaller rate hikes, and together will further encourage near-term speculation that the Fed will follow suite and slow the pace of hikes at the end of this year as well."

"Building expectations that broader dovish policy shift from G10 central banks is already underway is providing some much needed relief for risk assets. In the FX market, it has contributed to the USD correcting sharply lower."

"Next week’s FOMC meeting on 2nd November could prove even more pivotal for near-term USD direction."

"Overall, recent developments including the plunge in the price of natural gas in Europe and broad-based USD sell-off have made it less likely that EUR/USD fall as low as our year-end target of 0.9300."