- EUR/USD looks to 2021 highs

- Short-term gains driven by real money demand

- But valuation models leave EUR/USD looking stretched

Image © European Central Bank.

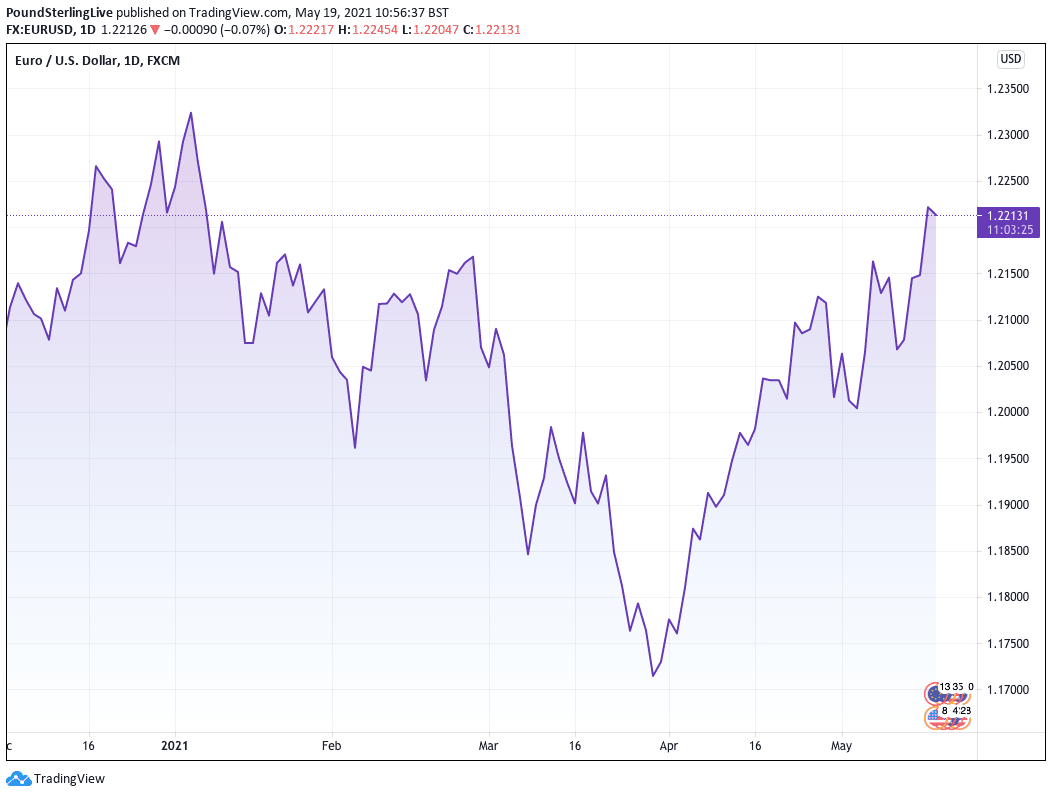

The Euro has risen back above the 1.22 mark against the Dollar amidst an ongoing short-term rebound leaving the prospect of fresh 2021 highs tantalisingly close for those bulls betting on further appreciation.

However, we hear from one foreign exchange strategist that while the rally in the Euro does not come as a surprise - and can continue for a little while yet - ultimately the foundations are poor and early June could represent a high-water mark for the exchange rate..

"We remain sceptical that the recent EUR/USD rally can be sustained in the near-term," says Valentin Marinov, Head of G10 FX Strategy at Crédit Agricole.

The call comes in the face of an appreciating single currency that has seen the Euro-to-Dollar exchange rate (EUR/USD) rise back above 1.22 this week as a trend of appreciating value extends from the March 30 lows at 1.1715.

The EUR/USD is now on course to deliver fresh 2021 highs based on existing momentum and Marinov says the appreciation does make some sense given external 'real money' investors are buying the currency to fund investments within the Eurozone.

According to Crédit Agricole's FX positioning gauge, the Euro was bought for most of the past week with real money investors driving most of the latest development.

"This makes sense, especially when considering that equity-related inflows may be among the main drivers of currency strength. Speculative-oriented investors such as hedge funds, however, have been fading currency upside," says Marinov.

"Those flows were sufficient for preventing the single currency from entering strongly overbought territory. From that angle, further short-term upside cannot be ruled out, at least as long as EUR-denominated risk assets continue to perform," he adds.

But Crédit Agricole's proprietary 'Fast FX Fair Value Model' finds the U.S. Dollar remains undervalued against the Euro, Yen and Canadian Dollar and that recent extensions higher only leave the EUR/USD looking ever more overvalued.

"Indeed, EUR/USD’s short-term fair value has been lowered from 1.1955 to 1.1915 as short-term rates shifted modestly further in favour of the USD over the EUR and peripheral EGB spreads over bunds continued to rise," says Marinov.

Analysts find that the rise in the EUR/USD exchange rate of late pushes it yet further into overvalued territory.

Image courtesy of Credit Agricole.

Beyond the fair-value modelling the fundamental arguments against the Euro's appreciation appear to stack up with the European Central Bank (ECB) who will be required to give a major policy steer mid-year.

"We think that, come June 10, the recent tightening of the Eurozone financial conditions could tilt the balance of risks

towards a delay of the PEPP taper beyond Q3, especially as the Governing Council tries to avoid further EGB yield spikes during the relatively illiquid summer period," says Marinov.

Such a move could constitute a dovish surprise in his opinion and lead to European sovereign bond yields surrendering most of their gains since March.

Given the yield paid on sovereign bonds relative to those in other countries is a major driver of currency valuations, such a move could have implications for the Euro exchange rate complex.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

At the same time improving U.S. growth and inflation data could push U.S. sovereign yields closer to their March high says Marinov.

As a result, Crédit Agricole think that the long-term Eurozone-U.S. yield spread will turn more negative again and weigh on EUR/USD.

Elsewhere, Crédit Agricole note recent talk about U.S. imports of Eurozone exports boosting EUR/USD is not borne out of tangible evidence.

"The lack of corporate hedging flows further suggests that the EUR’s recent rally is almost entirely driven by inflows in the Eurozone stock markets. In turn, this could make the currency vulnerable to any potential deterioration of risk sentiment on the back of higher UST yields," says Marinov.